The practical answer

- Short answer

- Benchmarks for SAP partner revenue composition. Diagnose your valuation based on License, Services, and AMS mix. Move from 4x to 12x EBITDA.

- Best fit

- Industry: Enterprise Software / IT Services. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 55% Target Gross Margin for optimized Application Management Services (AMS) vs. 35% for standard projects.

The 'Project Revenue' Trap

You are running on a treadmill that is speeding up, but your valuation is standing still. As an SAP partner, you likely celebrate the "Big Bang" implementation wins. A $2M S/4HANA migration? Champagne. A $500k advisory project? High fives.

But to a Private Equity buyer, that revenue is terrifying. Every January 1st, it resets straight back to zero.

We call this the Project Revenue Hamster Wheel. Most stalled SAP partners ($10M–$20M revenue) have a revenue mix that looks like this: 85% Professional Services (Projects), 10% Low-Margin Resell (License), and 5% Ad-Hoc Support (AMS).

Here is the brutal truth: Project revenue trades at 4x-6x EBITDA. It is viewed as high-risk, labor-dependent, and non-compounding. If you want the premium 10x-14x multiples seen in the 2025 IT Services Valuation Trends, you must engineer a mix that proves durability, not just delivery.

The 7-to-1 Lie

SAP often touts that for every $1 of software sold, partners generate $7 in services. While directionally true, chasing that $7 in pure billable hours is a race to the bottom. The "Unicorn Partners"—those exiting for $50M+—don't just service the software; they productize the service. They shift the mix from "hours sold" to "outcomes owned."

To a buyer, project revenue is one-time work. AMS revenue proves durability, and IP revenue proves leverage. Choose the mix that supports the multiple you want.

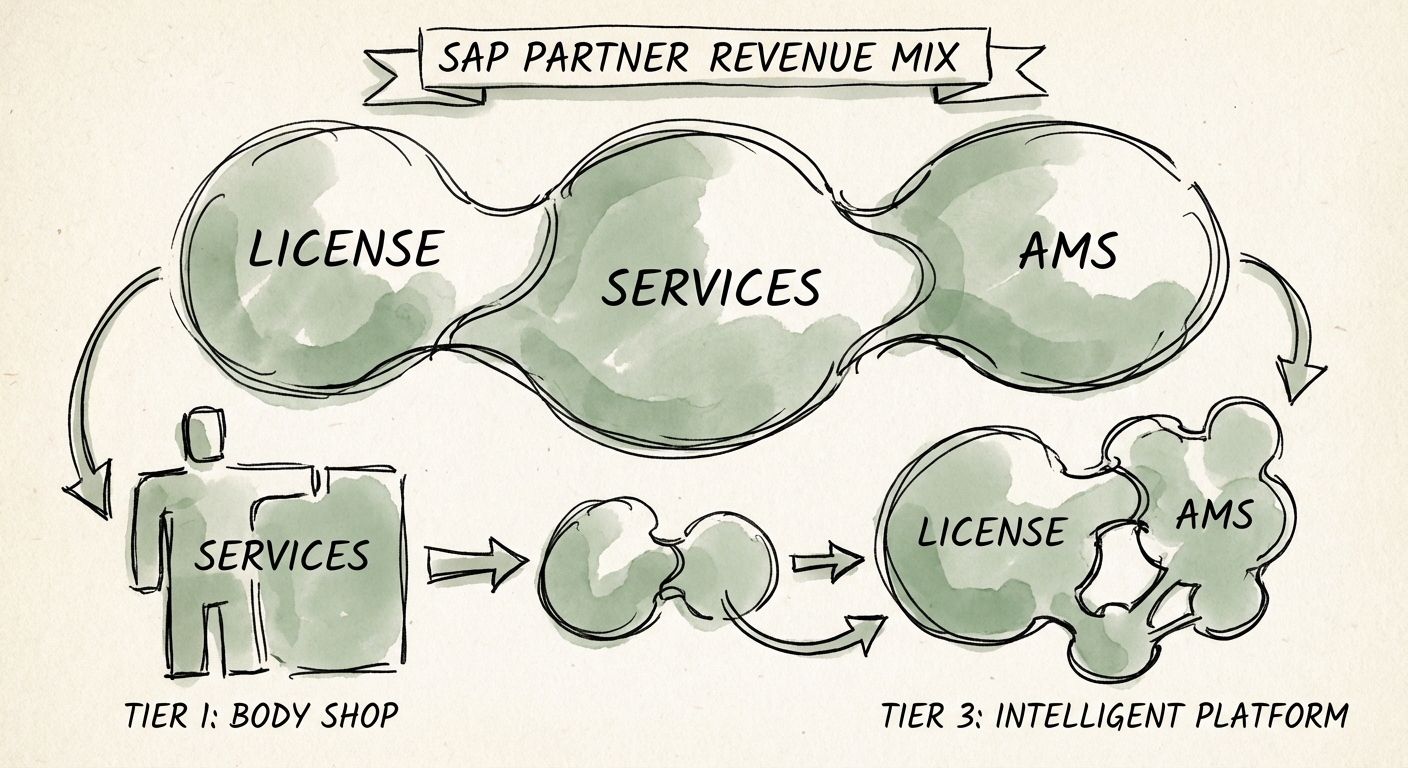

The Revenue Mix Diagnostic

Where does your firm fall? We analyze SAP partners across three distinct tiers of revenue composition. Find your profile below to understand your implied valuation cap.

Tier 1: The Body Shop (Valuation: 4x–6x EBITDA)

- Revenue Mix: 90% Projects / 10% AMS / 0% IP.

- Gross Margins: 30-35% (Blended).

- The Reality: You are essentially a high-end staffing agency. You have high concentration risk (one paused project kills the quarter) and zero leverage. Your "License" revenue is just reselling SAP paper for a slim margin, adding topline bloat but no bottom-line equity value.

Tier 2: The Managed Service Challenger (Valuation: 7x–9x EBITDA)

- Revenue Mix: 60% Projects / 35% AMS / 5% IP.

- Gross Margins: 40-45% (Blended).

- The Reality: You have stabilized the ship. Your AMS contracts are multi-year (3+ years), covering your OpEx. You are no longer desperate for every RFP. PE firms see you as a "platform" capable of add-on acquisitions.

Tier 3: The Intelligent Platform (Valuation: 10x–14x EBITDA)

- Revenue Mix: 40% Projects / 40% AMS / 20% Proprietary IP.

- Gross Margins: 50%+ (Blended).

- The Reality: You don't just implement SAP; you have a proprietary accelerator (IP) that speeds it up, and you retain the customer on high-margin, automated AMS. That 20% IP revenue drops 80% margin to the bottom line, expanding your EBITDA aggressively. This is the "Gold Standard" mix.

Fixing the Mix: From Reseller to Owner

Moving from Tier 1 to Tier 3 isn't about selling more; it's about selling differently. Here is your 12-month remediation plan.

1. Stop Treating AMS as the "Cleanup Crew"

In most firms, AMS is where junior consultants go to die. Flip this. AMS should be your Net Revenue Retention (NRR) engine. Structure AMS contracts not as "blocks of hours" but as "managed outcomes" (e.g., specific uptime or process efficiency SLAs). This allows you to decouple revenue from hours using offshore leverage or automation, driving margins from 30% to 55%.

2. Productize Your "Gap" Code

Every SAP partner has that one custom report, interface, or Fiori app they build for every client. Stop giving it away as billable hours. Package it. Name it. License it. Even if it only adds $500k in ARR, that $500k is worth $6M in Enterprise Value at exit (12x multiple). This is your bridge to the "Proprietary IP" bucket.

3. The "Land and Embed" Strategy

Don't just "Land and Expand." Use the S/4HANA migration deadline (2027/2030) as a trigger to lock in 3-year AMS agreements during the implementation sale. Discount the implementation fees (Projects) in exchange for long-term, high-margin committed revenue (AMS). You trade low-quality revenue today for high-quality valuation tomorrow.

For a deeper dive on structuring these deals, review our guide on Structuring Earnouts That Actually Pay Out, because if you don't fix this mix, your earnout will be tied to impossible growth targets.