The practical answer

- Short answer

- Are you a Splunk partner relying on licensing resale? Learn why resale-heavy firms trade at a 50% discount and how to pivot to high-margin managed services.

- Best fit

- Industry: Cybersecurity & Observability. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 4x-6x Typical EBITDA multiple for Splunk partners focused on resale (VAR model).

The Cisco Effect: The End of the Boutique Reseller

For the last decade, many Splunk partners built comfortable businesses on the back of the "Reseller's Annuity." You sold the license, you collected the renewal margin (often boosted by rebates to 15-20%), and you delivered just enough professional services to keep the deployment sticky. In the era of standalone Splunk, this was a viable lifestyle business. In the era of Cisco, it is a valuation death trap.

Following Cisco's $28B acquisition, the channel dynamics have fundamentally shifted. Cisco's distribution network is optimized for massive scale, favoring broadline distributors and global systems integrators (GSIs) over boutique resellers. For a specialized Splunk partner, competing on licensing margin is now a race to the bottom against giants like CDW and Insight. If your P&L is 80% licensing revenue and 20% services, private equity buyers view you not as a technology consultancy, but as a sub-scale distributor with no competitive moat.

The data is brutal: Pure-play Value Added Resellers (VARs) are currently trading at 4x-6x EBITDA, while partners with a "Managed Motion" (MSSP/MSP) focusing on Security and Observability are commanding 10x-14x EBITDA. If you are still prioritizing license resale over managed services IP, you are actively suppressing your company's enterprise value by half.

If your revenue mix is 80% licensing, you aren't a consultancy—you're a bank financing your customer's software purchase. PE firms don't pay premiums for banks.

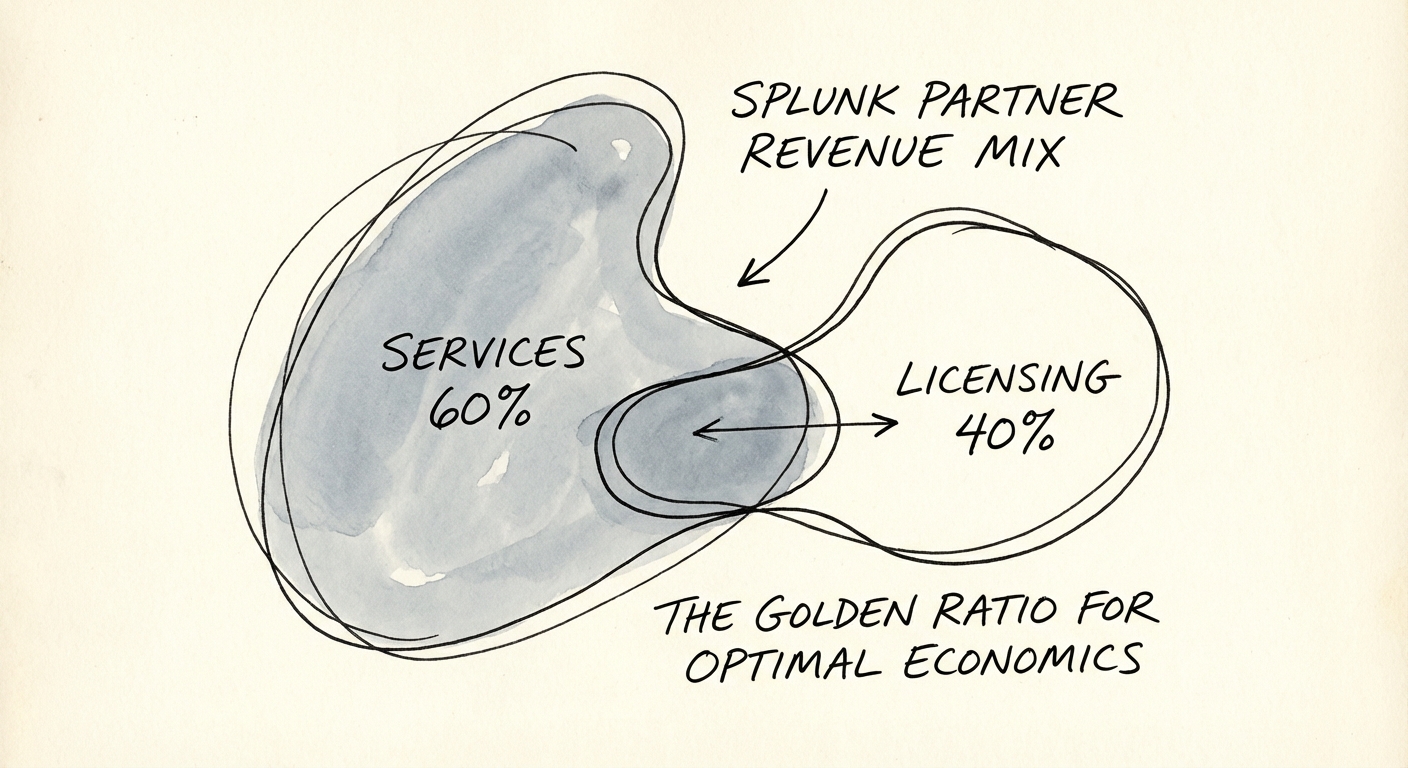

The Golden Ratio: 40/60 Licensing vs. Services

To unlock a premium multiple, you must invert the typical reseller model. The highest-valued Splunk partners in 2026 adhere to a strict revenue composition benchmark: maximum 40% resale, minimum 60% services.

The Margin Reality

The valuation gap is driven by gross margin quality. Resale revenue, even with "Elite" tier rebates, rarely exceeds 15% gross margin after accounting for sales commissions and cost of capital. In contrast, well-run Managed Splunk services—specifically in Security Operations (SecOps) and Observability—should operate at 50-65% gross margins.

Consider two firms with $20M in top-line revenue:

- Firm A (The Trap): $16M Resale (15% GM) + $4M Services (40% GM). Total Gross Profit = $4M. Valuation ~ $4M-$6M (1x Gross Profit).

- Firm B (The Target): $8M Resale (15% GM) + $12M Services (60% GM). Total Gross Profit = $8.4M. Valuation ~ $25M+ (3x Gross Profit / High EBITDA multiple).

Firm B is worth 4x-5x more than Firm A, despite having the same top-line revenue. Why? Because Firm B owns the customer outcome, whereas Firm A merely processes the transaction.

The Pivot: From "Admin" to "Observability"

Escaping the reseller trap requires moving up the value chain. Low-value services like "Splunk Administration" or "Upgrade Support" are being commoditized by Splunk Cloud and AI automation. The premium valuation lies in the "Manage" motion—specifically acting as a specialized Managed Security Service Provider (MSSP).

Strategic partners are wrapping Splunk licenses into their own IP-led offerings. Instead of selling a license and billing hours, they sell "Security Outcomes as a Service" or "Full-Stack Observability." This shifts the revenue recognition from one-time transactional resale (low multiple) to recurring managed services (high multiple). The most successful partners are leveraging the Splunk Partnerverse "Manage" motion to hold the entitlement themselves, effectively turning low-margin resale into a component of a high-margin managed service bundle.

Actionable Advice: Audit your last 12 months of revenue. If pass-through licensing exceeds 50% of your total bookings, institute a "Service Attach" mandate. For every $1 of licensing sold, target $1.50 of managed services. If you cannot attach services, do not chase the low-margin license deal—it is empty calories that bloat your revenue figure while starving your valuation.