The practical answer

- Short answer

- For HubSpot Partners, revenue mix dictates valuation. Why an 80% project mix caps you at 4x EBITDA, and how to pivot to Managed RevOps for a 10x exit.

- Best fit

- Industry: Professional Services. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 12x EBITDA multiple for HubSpot partners with >60% recurring revenue (vs. 4x for project shops).

The 'Project Trap' in the HubSpot Ecosystem

Most HubSpot Solutions Partners begin life as implementation shops. You sell the software, you configure the portals, you train the team, and you hand over the keys. It is honest work, and in the early days of the ecosystem (2015–2020), it was lucrative work. The demand for “lift and shift” migrations from Salesforce or spreadsheets was insatiable.

But in 2026, the “Project Shop” model is a valuation killer. If 80% of your revenue comes from one-time implementations, you do not own a business; you own a very expensive job. You are on a permanent hamster wheel of customer acquisition, needing to replace every dollar of revenue you earn each quarter.

The Valuation Gap: 4x vs. 12x

Private Equity buyers and strategic acquirers (like Elite partners rolling up smaller shops) view project revenue as low-quality revenue. It resets to zero every January 1st.

- Project-Heavy Firms (80% Implementation): Trade at 4x–6x EBITDA. Buyers treat you like a staffing agency. They are buying your labor, not your IP.

- Recurring-Heavy Firms (60%+ Managed Services): Trade at 10x–12x EBITDA. Buyers view you as a platform. They are buying your predictable cash flow and customer retention.

The math is brutal. Two agencies with the exact same $10M revenue and $2M EBITDA can have a $12M difference in exit value simply based on how that revenue is composed.

If 80% of your revenue resets to zero every January 1st, you don't own a business. You own a high-stress job that you can't quit.

The 2025 Program Changes: A Warning Shot

HubSpot’s 2025 Solutions Partner Program updates were not subtle. By rebranding “Sold Points” to “Sourced Points” and removing Partner-Assisted deals from minimum requirements, HubSpot sent a clear message: Passive service delivery is no longer enough.

Furthermore, the introduction of the usage and retention signals signals that HubSpot is now grading partners on retention and adoption, not just the initial sale. If you implement a portal and the client churns or fails to use the tools six months later, your partner score degrades. This structural change penalizes the “burn and churn” implementation model and rewards the “land and expand” managed services model.

The Golden Ratio: 40/60

So, what is the target revenue mix? Based on data from top-quartile Elite partners and PE-backed consolidators, the ideal “Exit Ready” mix is:

- 40% Implementation (New Business): This is your customer acquisition engine. You break even or make a modest 30% margin here to acquire the logo.

- 60% Managed Services (Recurring): This is your profit engine. You target 60%+ gross margins through productized RevOps retainers, not hourly support.

If your managed services revenue is below 30%, you are dangerously exposed to pipeline volatility. If it is above 80%, your new logo velocity is likely too slow to offset natural churn. The 40/60 split balances growth with predictability.

Pivoting to Managed RevOps: The ‘Productization’ Imperative

The mistake most founders make when shifting to recurring revenue is selling “buckets of hours.” This is a race to the bottom. Clients will inevitably scrutinize timesheets and ask, “What did we get for our $5,000 this month?”

To command a premium valuation, you must shift from “Support Retainers” to “Managed RevOps.”

Service Packaging Benchmarks

Successful managed services are sold as outcomes, not hours. They solve specific, recurring problems:

- Data Hygiene & Governance: “We ensure your database never exceeds 5% bounce rate and deal stages are accurate.”

- Pipeline Architecture: “We run your monthly pipeline council and optimize lead scoring quarterly.”

- Integration Monitoring: “We monitor the API sync between HubSpot and NetSuite, resolving errors within 4 hours.”

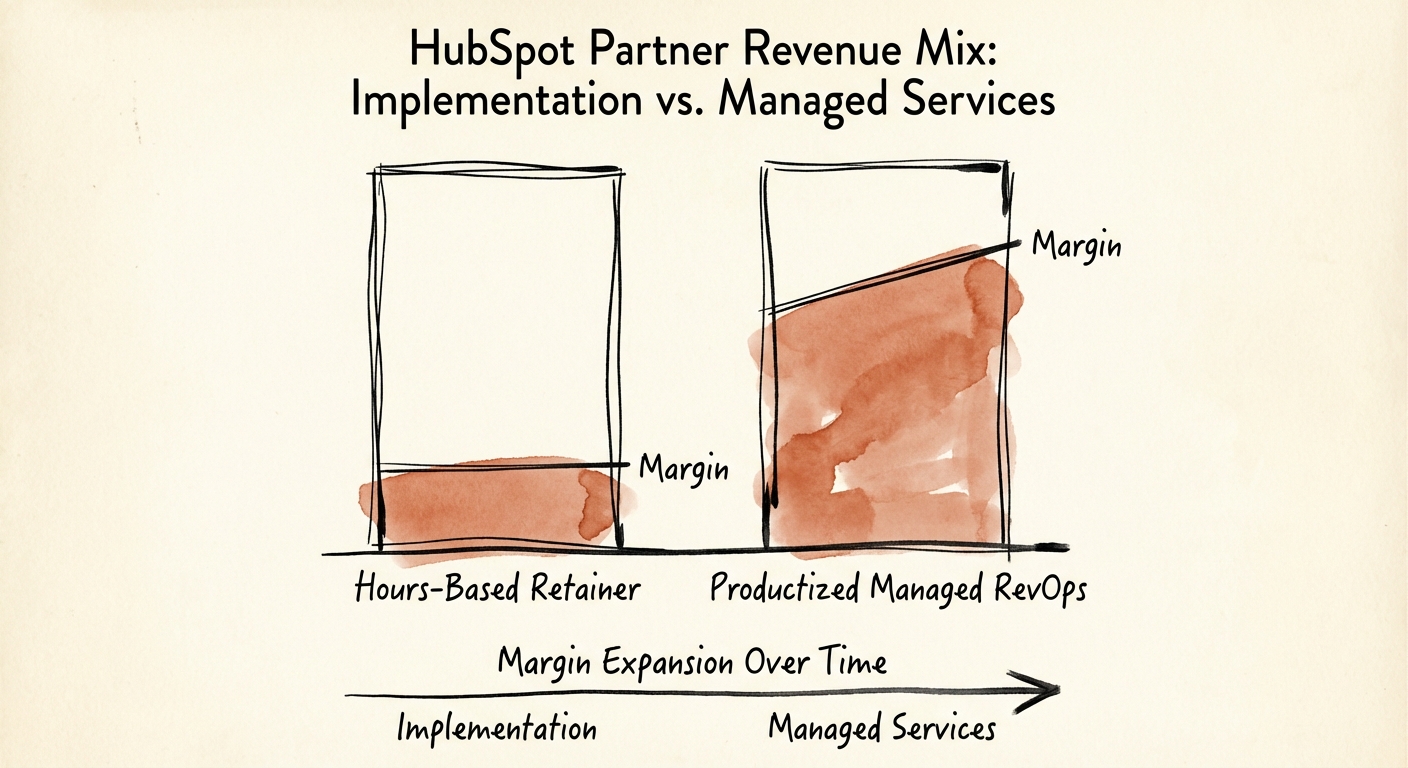

By packaging these as fixed-fee subscriptions (e.g., $3k, $5k, $8k/month), you decouple revenue from time. A “Data Hygiene” package might take your team 10 hours in month one, but only 2 hours in month six via automation. Your margin expands over time, whereas an hourly retainer’s margin is capped. This Margin Expansion story is what gets you the 12x multiple.