The practical answer

- Short answer

- Zendesk's AI Resolution Platform gutted the value of setup work. Partners earning recurring tuning revenue trade near 12x; setup shops stall near 5x. Here's the math.

- Best fit

- Industry: Customer Experience (CX). Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 12x EBITDA multiple for partners with >40% Optimization revenue.

The $50K setup fee is now a $50 wizard

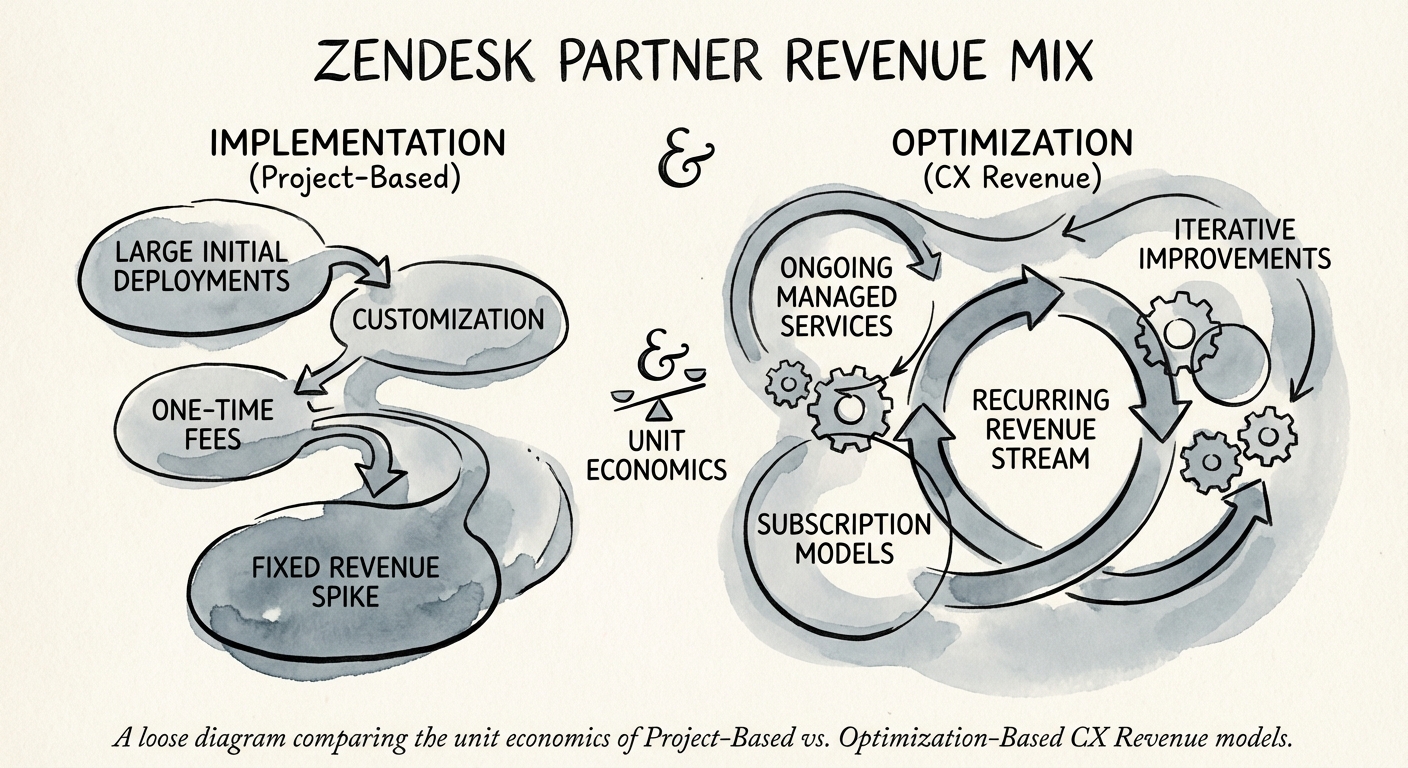

Picture the engagement that built half the Zendesk partner channel: a six-week deployment, a statement of work full of triggers, macros, business rules, and routing logic, an invoice somewhere north of $50,000, and a 90-day block of support hours that quietly expired before anyone used them. Clean project. Good margin. Onto the next one.

That motion is being automated out from under you. Zendesk's own roadmap has reframed the product from a ticketing tool into a Resolution Platform — AI agents that resolve conversations end to end, with onboarding flows that stand up the basic trigger-and-macro scaffolding without a human services hour attached. The configuration work you used to charge for is collapsing into a setup wizard. The judgment work — deciding which intents to automate, where the AI is confidently wrong, when a human handoff protects CSAT — is not.

Here is the uncomfortable part for anyone thinking about an exit. The complexity moved, and so did the money. An acquirer running technology due diligence on a CX services firm is not counting how many Zendesk instances you've stood up. They are counting how much of your revenue survives January 1st. A practice that lives on project work resets to a blank pipeline every year and gets read as a staffing arm with a good logo. A practice that gets paid every month to keep an AI resolution engine performing gets read as a platform. Those two stories carry roughly 2x the multiple difference — and most Zendesk partners are still telling the first one.

Nobody pays a premium for the firm that built the macros. They pay for the firm that can walk into a QBR and prove resolution rate climbed from 22% to 41% — and that it would slide back the day you left.

Run the two firms side by side

Take two Zendesk Premier partners, both at $10M in revenue, both profitable, both with a wall of logos. On paper they look like comps. They are not.

Firm A — the deployment shop. $8M of that is project work, $2M is leftover support hours. Project gross margin sits around 45% once you account for the senior solution architects who can't be fully utilized between SOWs. Because roughly 80% of revenue has to be re-won every year, the sales engine never stops paying for itself — acquisition cost is structurally high. A buyer looks at this and sees risk that walks out the door with each completed project. The kind of multiples First Page Sage and Clearly Acquired publish for project-based professional services firms land this in the 4x-6x EBITDA range. Call it $5M-$7M.

Firm B — the optimization partner. Same $10M, but flipped: $4M project, $6M recurring optimization retainers. Retainer gross margin runs closer to 65% because the work is tooled and templated, not bespoke. Acquisition cost is low because growth comes from expansion inside existing accounts, not net-new logos. A buyer sees revenue that compounds and a reason it stays. That story trades at 10x-12x — $12M-$15M for the identical top line.

The hinge is a specific number. Across CX services, the valuation re-rate doesn't happen gradually as recurring revenue creeps up — it lurches once optimization revenue crosses about 40% of total. Below the line you're a project firm with some retainers. Above it you're a platform with some project overflow. Same dollars, different asset class. And the comparison isn't unique to Zendesk; it mirrors the well-documented gap between how the market prices a managed-service book versus a consultancy. Predictability is the thing being bought.

What a Zendesk optimization retainer actually contains

You don't get to the 40% line by relabeling "blocks of admin hours" as a retainer — that's the same commodity work in a nicer wrapper, and it loses to offshore on price every time. You get there by attaching your fee to the one number Zendesk has taught your clients to care about: automated resolution rate, the share of conversations the AI closes without a human touching them.

A retainer worth $10K-$20K a month, in Zendesk terms specifically, looks like this:

- Monthly intent triage. Pull the conversations the AI agent failed to resolve or escalated, cluster the top unmatched intents, and train them. The backlog of "queries the bot fumbled" regenerates every month — which is exactly why this is a subscription and not a project.

- Handoff and friction audits. Find where the AI hands off too early, too late, or into the wrong queue, and where human agents stall inside a workflow. Fix it with logic, a custom app, or an integration. This is the work the setup wizard can't do because it requires reading your client's conversation data.

- A cost-avoidance QBR, not a usage report. Don't show them tickets handled. Show them: resolution rate moved from, say, 24% to 38%, which deferred roughly two support hires this quarter. Frame the meeting around headcount they didn't have to add. That's the slide that renews the contract.

This shift changes who you hire. Fewer configurators, more analysts who can read CX conversation logs and reason about deflection. Expect billable utilization to drop into the 65-70% band — optimization work simply isn't billed like a project — but watch revenue per head climb anyway as your IP and tooling do the leverage. That tradeoff is consistent with what shows up in 2025 utilization benchmarks by role: the highest-value services teams are rarely the most utilized ones.

If you're eyeing a sale inside 24 months, the single highest-leverage move is converting your existing implementation logos into optimization subscribers — you've already paid the acquisition cost. You don't need all of them. Converting even one in five can drag your revenue mix across the 40% line and re-rate the whole business. The thing not to do is take the firm to market while every dollar of revenue still ends the day a project does.