The practical answer

- Short answer

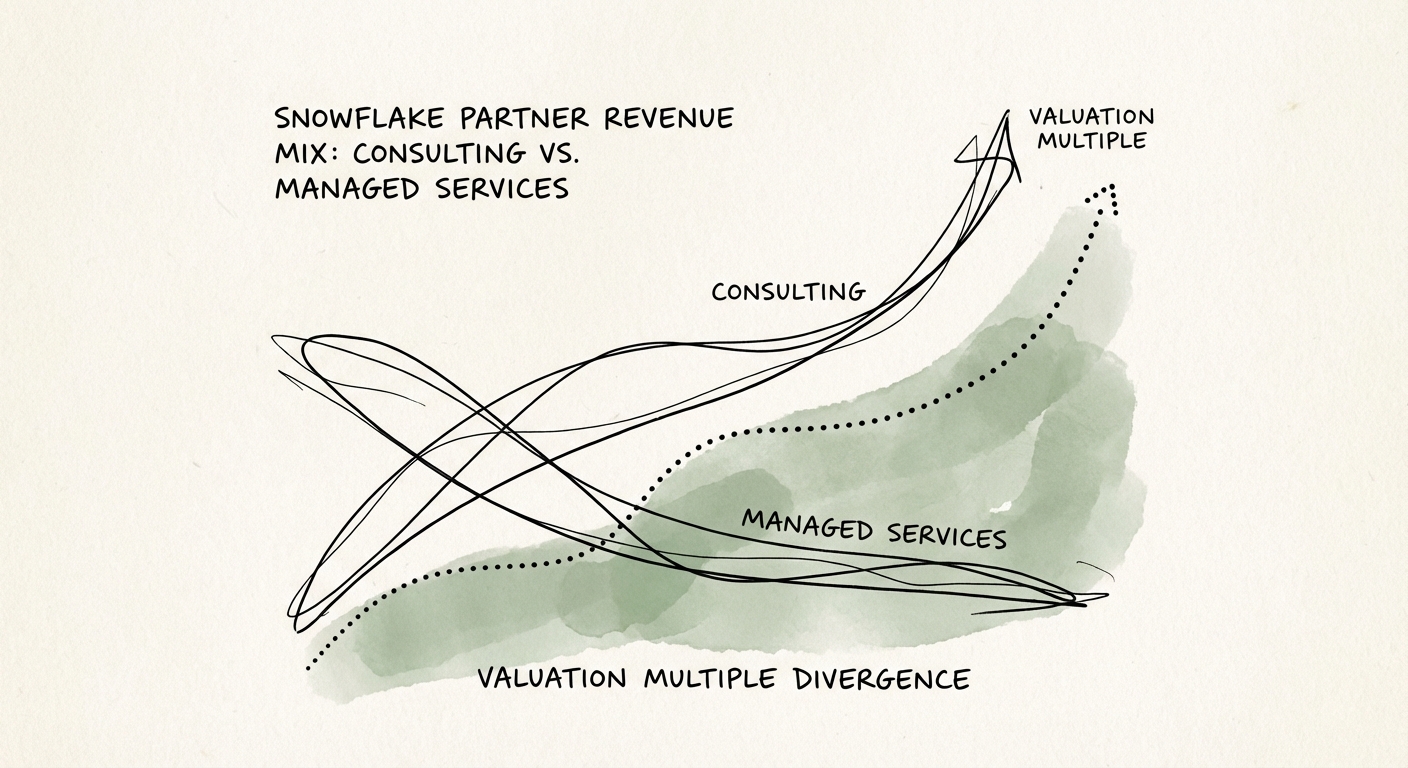

- A $15M Snowflake partner with 40% managed services outvalues a $20M migration shop. Here is the revenue-mix math buyers run, and how to move your line.

- Best fit

- Industry: Data & Analytics Services. Function: Executive Leadership

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 12x EBITDA Multiple for Partners with >40% Managed Services Revenue

The Teradata migrations ran out before the partners did

Picture two Snowflake partners in a data room next to each other. The first did $20M last year, almost entirely Teradata and Netezza migrations billed by the hour. The second did $15M, and 40% of it is recurring: monthly consumption monitoring, warehouse right-sizing, a few Native Apps living inside client accounts. The founder of the bigger shop expects the bigger number. He gets the bigger surprise instead. The $15M partner clears a 12x EBITDA multiple. He stalls at 6x. Same Snowflake badge, same general capability, half the value per dollar of revenue.

This is not a quirk of one deal. It is the dominant fault line running through the Snowflake ecosystem heading into 2026, and it traces directly to a calendar problem. For five years the work was migration: find a legacy warehouse, write a lift-and-shift Statement of Work, bill the hours, move on. That demand was real and it was lucrative. It was also finite. Most of the large legacy estates that wanted to move have moved, and the ones that have not are stuck for reasons no SOW fixes. The phrase "get me to the cloud" has stopped generating inbound. ISG's segmentation of the partner ecosystem (ISG Provider Lens: Snowflake Ecosystem Partners 2025) tracks exactly this: the market is reclassifying partners by what they do after go-live, not how many bodies they put on the implementation.

The buyers noticed before the founders did. A migration-heavy book of business is, in valuation terms, a sequence of one-time events. Every January, a partner running 90% project revenue starts again from roughly zero pipeline. That is not a business with continuity; it is a business with a good reputation and an empty calendar. The continuity premium goes to the partner whose revenue shows up next month whether or not the phone rings, and on Snowflake that continuity has a specific shape: recurring Data Cloud solutions bolted to consumption the client cannot turn off without turning off their analytics.

When a buyer sees Snowflake credit consumption on your dashboard but Time-and-Materials on your invoices, they price you as a staffing agency that got lucky on one platform.

Why hitting 85% utilization is the wrong scoreboard

The consulting founder's instinct, when growth stalls, is to push utilization. Get the billable team to 80%, then 85%. It feels like rigor. It is the trap. In a pure services model your revenue ceiling is your headcount times your bill rate times the hours you can extract before people quit, and that last variable is where the math breaks. A healthy practice runs around 72% billable; as our utilization benchmarks show, drive past 85% and you are not buying growth, you are pre-funding your next round of attrition. Below 65% and the margin is already gone. The window is narrow and a buyer knows it, which is why they discount the whole model: your growth is linear, capped, and tied to your ability to keep hiring senior data engineers in a market that is short on them.

The managed services line decouples revenue from headcount, and on Snowflake it does so in a way that is unusually defensible. A partner selling FinOps-as-a-service is not billing for the migration; they are billing a monthly fee to watch consumption, resize warehouses before the bill spikes, and keep the client off the consumption cliff that turns a celebrated migration into a budget crisis six months later. That contract renews because the alternative is the client watching their own credit burn, which they will not do well. TSIA's managed services work (The State of Managed Services 2025) puts renewal rates on managed contracts meaningfully above project extensions, and renewal rate is the single number that converts a multiple from 6 to 12.

The cleanest way to see the gap is the Rule of 40 (revenue growth plus EBITDA margin). Migration-heavy partners tend to live in the twenties, because every point of growth costs them recruiting spend and every senior hire who leaves takes client trust with them. Managed services partners cross 40 routinely, and they do it the easy way: a Snowflake account that gets more data, more users, and more workloads every quarter is an expansion engine that does not require a new sale. Snowflake's own consumption disclosures (Snowflake Investor Relations) show net revenue retention well above 100% across their base, and a managed partner sitting on top of that base inherits the same organic tailwind. The consulting shop has to go win it back every year.

You cannot hire your way out of the body-shop multiple

If you are running 80%-plus project revenue, the gap does not close by adding consultants; it closes by changing what you sell. Here is what actually moves the line, in the order it works.

Productize the work you already give away. Every Snowflake client you migrated needs the same things forever: credit monitoring, RBAC auditing, query tuning, warehouse right-sizing. Right now you do this as ad-hoc favors that read as scope creep on a closed project. Package the exact same activity as a fixed monthly "Managed Data Platform" subscription and you have converted a cost center into the recurring line a buyer pays a premium for. This is the fastest first step in building managed services revenue on Snowflake, because the delivery muscle already exists.

Push your IP inside the client's account. The partners commanding the top multiples in 2026 deploy Snowflake Native Apps that run in the customer's own environment. If you have a proprietary data-quality routine or a vertical data model, shipping it as a Native App makes you genuinely hard to rip out; the switching cost is no longer "find another consultant," it is "rebuild the thing our analytics now depends on."

Pay for the mix you want. This is where most pivots quietly die. If your sales team earns the same commission on a $100K project as on $100K of ARR, the rep will sell the project every time, because it closes faster. Weight the comp hard toward the recurring component and watch the mix start to move within two quarters. The market has already made its decision: implementation hours are a commodity priced like staffing, and a managed Snowflake outcome is an asset priced like software. Your invoices, not your intentions, tell the buyer which one you are.