The practical answer

- Short answer

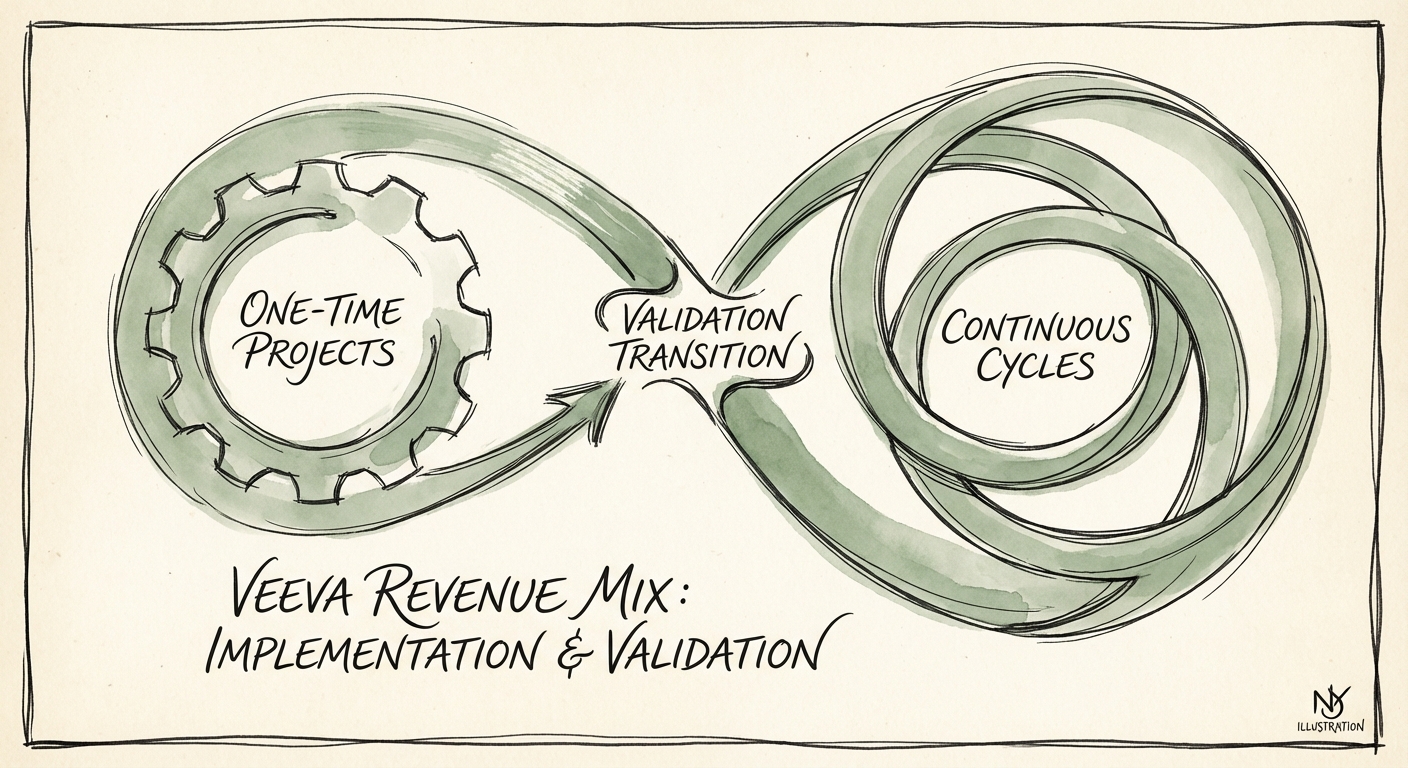

- Why Veeva partners focused on implementation trade at 6x EBITDA while managed validation firms command 12x. A revenue mix diagnostic for PE sponsors.

- Best fit

- Industry: Life Sciences Technology. Function: Revenue Architecture

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 6x Typical EBITDA multiple for Veeva partners with >80% implementation revenue (Project-based).

The 'Vault CRM Migration' Sugar Rush

For Veeva partners, 2024 and 2025 have provided a historic windfall: the forced migration from Veeva CRM (built on Salesforce) to Veeva Vault CRM. This "replatforming" event has filled pipelines with massive, high-bill-rate implementation projects. However, for Private Equity investors and founders looking to exit in 2026, this revenue spike is a dangerous valuation trap.

The market is currently bifurcated between partners treating this migration as a construction project (Implementation) and those treating it as a utility hookup (Managed Validation). The former generates one-time spikes in revenue that QofE (Quality of Earnings) providers will heavily discount as "non-recurring." The latter builds a sticky, recurring revenue tail that drives 12x+ multiples.

Our diagnostic data shows that standard implementation shops are trading at 6x-8x EBITDA because their revenue is tied to "event-based" spend. Once the Vault CRM migration concludes (with the 2030 deadline being the hard stop, but the bulk of enterprise moves happening now), these firms face a "Revenue Cliff." In contrast, partners who use the migration to install Continuous Validation and Commercial Operations as a Service (COaaS) frameworks are trading at 12x-14x EBITDA.

In Life Sciences, project revenue can look attractive during a migration wave, but recurring validation is what protects the multiple after go-live.

The Pivot: From 'Project Validation' to 'Continuous Compliance'

In the Life Sciences sector, "Validation" (meeting FDA 21 CFR Part 11 requirements) has historically been a commoditized phase of the implementation waterfall—a checklist item billed by the hour. Low-value partners view validation as a hurdle to clear before go-live. High-value partners view it as a subscription product.

The "Managed Validation" model flips the economics. Instead of billing for a one-time validation script execution, elite partners sell a recurring compliance shield. This involves:

- Release Management: Veeva releases three major updates per year. A managed service partner validates these updates automatically, ensuring the client never drifts out of compliance.

- Regression Testing as a Service: Automated testing suites that run weekly, not just at go-live.

- Content Factories: Managing the lifecycle of commercial content (PromoMats) on a retainer basis rather than per-asset project fees.

The Benchmark: A healthy Veeva partner should aim for a revenue mix of 45% Managed Services / 55% Project Services. Firms below 20% managed services are effectively "staff augmentation" shops in the eyes of acquirers, regardless of their "Premier" partner badge.

Valuation Implications: The 'Body Shop' Discount

When PE firms evaluate Veeva partners, the primary risk filter is concentration in low-IP services. Implementation is labor-intensive and low-IP; it requires constantly hiring expensive consultants to sell their time. Managed Validation and Commercial Strategy rely on IP (proprietary test scripts, automation frameworks, data models) to decouple revenue from headcount.

According to 2025 HealthTech M&A data, tech-enabled services firms with strong recurring revenue (like Managed Validation) are trading at a 4-turn premium over pure professional services firms. The logic is simple: Acquirers will not pay for a revenue stream that is destined to evaporate when the migration wave subsides.

The Exit Readiness Checklist

To bridge the gap from 6x to 12x, partners must:

- Productize Validation: Stop selling validation hours. Start selling "Compliance Assurance" subscriptions.

- Audit the Revenue Mix: If project revenue > 80%, you are in the "danger zone" for a 2026 exit.

- Leverage the Vault Migration: Use the current migration projects to sign multi-year Managed Services agreements now, locking in the recurring tail before the project concludes.