The practical answer

- Short answer

- Why UiPath implementation partners trade at 6x EBITDA while Managed COE firms command 14x. A diagnostic guide for scaling RPA consultancies.

- Best fit

- Industry: RPA & Intelligent Automation. Function: Revenue Architecture

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for UiPath partners with >45% recurring COE revenue.

The 80/20 Project Trap: Why "Diamond" Status Won't Save Your Multiple

In the UiPath ecosystem, there is a dangerous misconception that "Diamond" partner status equals high enterprise value. While badge levels drive leads, they do not drive valuation multiples. The market has bifurcated into two distinct asset classes: Project Factories and Automation Platforms.

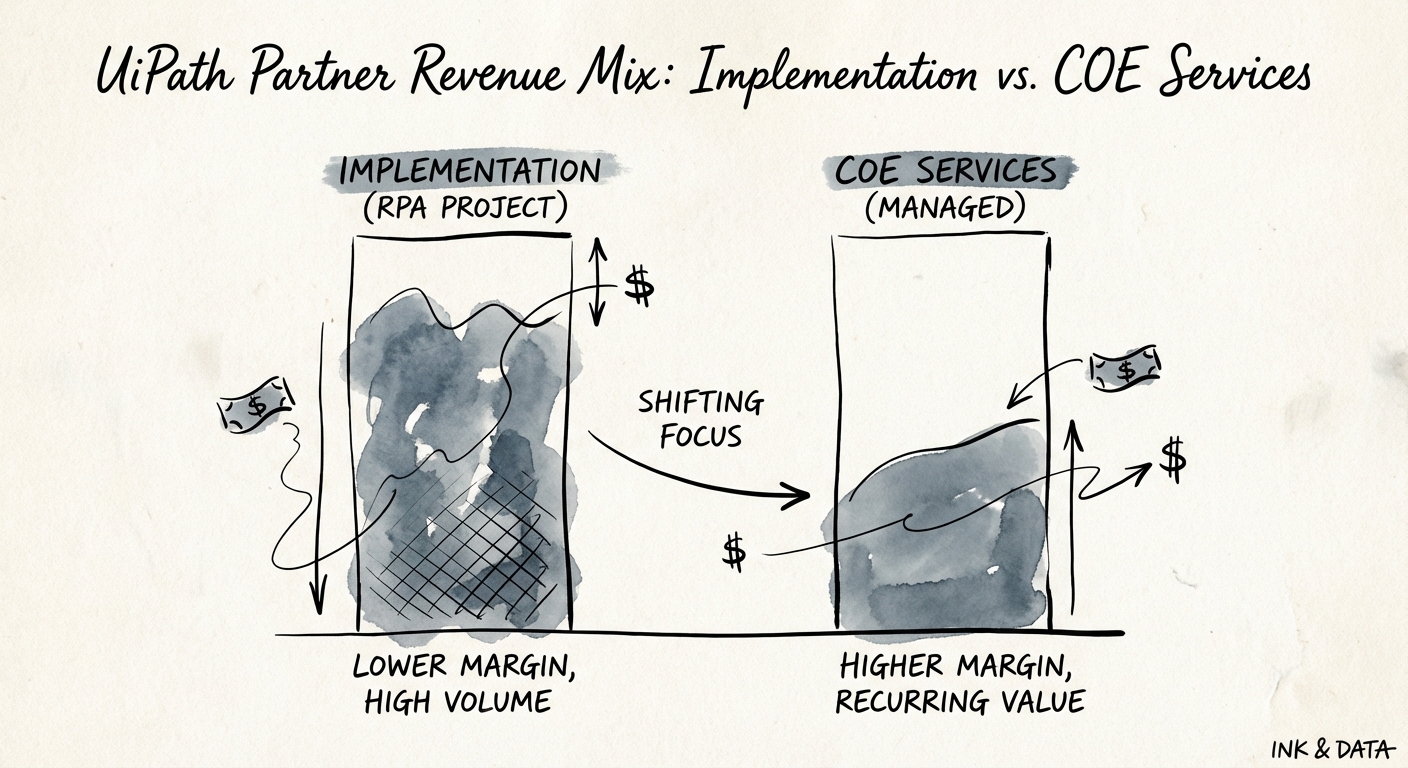

Project Factories—firms where 80% or more of revenue comes from one-off implementations—are currently trading at 5x to 7x EBITDA. These firms are effectively high-end staffing agencies. They suffer from the "hamster wheel" effect: every quarter starts at zero, and growth is linearly capped by headcount. Despite high hourly rates for senior RPA architects ($200+), the quality of this revenue is viewed as low by private equity buyers because it lacks predictability.

The hidden killer in this model is Bot Decay. Our data across 50+ RPA consultancies shows that without a structured maintenance contract, the average client churns 40% of their bot portfolio within 18 months due to application UI changes and process drift. If your revenue model is built solely on building new bots, you are constantly refilling a leaky bucket.

The market has stopped paying a premium for bot builders. Higher multiples go to partners who can own process uptime and governance. If you are still selling hours, you are selling a commodity.

The "Bot Decay" Arbitrage: Pivoting to Managed COE

The partners commanding 12x to 15x EBITDA multiples have flipped the script. Instead of selling "hours of development," they sell "outcomes availability." They have productized the Center of Excellence (COE) into a recurring revenue stream.

The "Automation-as-a-Service" (AaaS) Model

This model shifts the engagement from a Statement of Work (SOW) to a multi-year subscription. The math is compelling:

- Project Model: Client pays $50k for a bot. You build it, leave, and maybe get a $5k support ticket six months later.

- COE Model: Client pays $25k/year per process for "Guaranteed Uptime." You build the bot (at cost), but you own the maintenance, the infrastructure monitoring, and the exception handling.

While the Year 1 revenue is lower in the COE model, the Lifetime Value (LTV) increases by 3x. More importantly, the gross margin profile shifts. A mature COE utilizing shared infrastructure and junior support engineers (L1/L2) can achieve 60%+ gross margins, compared to the 40% ceiling of senior implementation staff. This recurring, high-margin revenue is what drives the valuation premium.

The Roadmap to 14x: Benchmarks for 2026

To bridge the gap from a 6x Project Shop to a 14x Platform Partner, you must aggressively restructure your revenue mix. The target profile for a premium exit in 2026 requires:

- Revenue Mix: At least 45% of total revenue must be recurring (Managed Services, Support, or IP).

- Net Revenue Retention (NRR): Must exceed 110%. In RPA, this is achieved by "farming" existing accounts for new processes to automate, not just maintaining old ones.

- USN Status: Achieving UiPath Services Network (USN) certification is no longer optional. It is the due diligence "check-the-box" item that validates your delivery methodology is standardized enough to scale without the founder's direct involvement.

The Agentic AI Wave: The next valuation multiplier is Agentic AI. Partners who can demonstrate not just static RPA maintenance, but the ability to deploy and manage AI agents (using UiPath Autopilot and Clipboard AI) within their COE contracts, are seeing early offers approaching 16x EBITDA. However, you cannot sell "AI Agents" if you don't first have the COE infrastructure to govern them.