The practical answer

- Short answer

- Workday partners: your project revenue trades at 1x, recurring AMS at 3x. Here's how to build the attach motion and pod structure that doubles your exit.

- Best fit

- Industry: Tech Services. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 21.2% Projected CAGR of the Application Management Services (AMS) market through 2035.

Two firms, same revenue, $20M difference

Picture two Workday implementation partners. Both did $20M last year. Both run 20% EBITDA. On paper, a banker would value them identically. They will not sell for anything close to the same number.

The first firm books almost all of that $20M as project revenue. Every January 1st, the pipeline resets to zero and the founder starts the year fighting for survival. The second firm has quietly built 40% of revenue into recurring application management services (AMS), so it opens the year already at 80% of target. When buyers run the model, project revenue gets credited at roughly 1x revenue (5-7x EBITDA), while predictable recurring revenue gets 3x (10-15x EBITDA). The premium recurring revenue commands at exit is well documented, and the gap shows up in the wire transfer.

Run the arithmetic on those two firms: the project-heavy one clears around $25M, the AMS-heavy one closer to $45M. Same top line. Same team. The only difference is mix. That is not a rounding error; it is the difference between a good outcome and a great one — and the broader IT services M&A market keeps rewarding predictability over scale.

Most Workday founders know the multiple gap exists. Almost none of them act on it, because they treat AMS as the place they park bench consultants between projects. That instinct is the single most expensive mistake in the partner channel.

A Workday partner doesn't get a premium for delivering a clean go-live. It gets a premium for owning the two release cycles that come after it, every year, forever.

Why the "support bench" model quietly destroys your best practice

Here is what AMS looks like in 90% of mid-market Workday shops. A client goes live. Someone sells them a "bucket of hours" for post-go-live support. The hours get burned by whichever senior implementation consultant happens to be between projects that week. It feels efficient. It is poison, for three specific reasons.

- Your best builders quit. The consultant who can architect a complex EIB or a gnarly Workday Studio integration did not join to triage business-process security questions and chase a configuration tweak in absence management. Put your A-team on ticket duty and they leave for a competitor that lets them build.

- The margin math is upside down. A senior implementation resource carries a cost basis you can bill at $250-300/hr on a project. You cannot bill that rate for Tier 1 Workday support — the market won't pay it. So every support ticket your senior solves is a resource sold below its value. The "bench utilization" you think you're capturing is actually margin you're setting on fire.

- The client feels the neglect. The moment a new implementation goes hot, that consultant gets yanked off support and the client's tickets languish through the next semi-annual release. They notice. They leave for a dedicated AMS provider that treats them as a customer rather than a gap-filler.

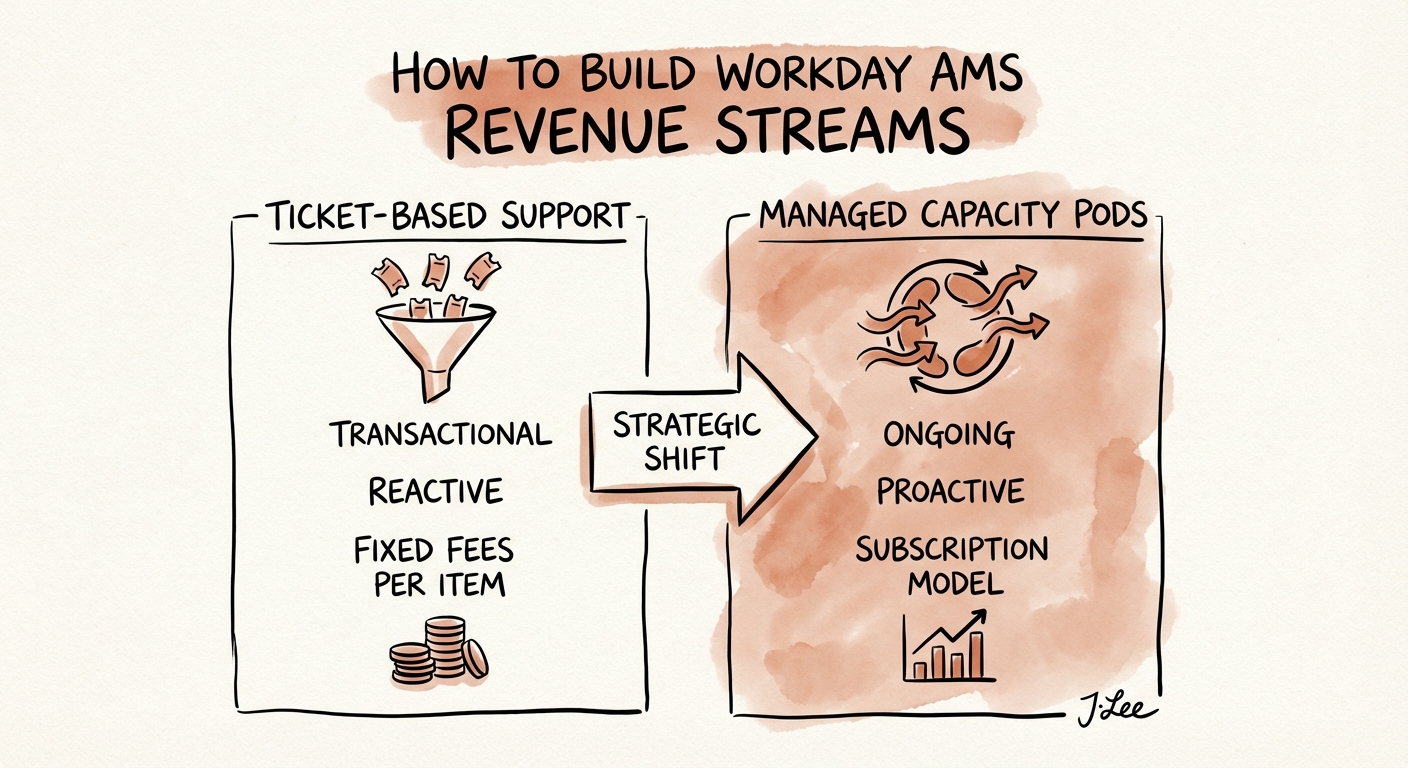

The fix is structural, not motivational. You have to decouple AMS from implementation entirely: a dedicated delivery pod with lead consultants owning architecture, nearshore or offshore resources executing the recurring config and ticket work, and a separate P&L owner whose only job is retention and expansion. The pod sells outcomes against Workday's release calendar, not hours against a depleting bucket.

The two moves that actually build the recurring line

Decoupling the org is necessary but not sufficient. Two specific moves convert it into valuation.

1. Sell AMS on Day 0, not at UAT

The reflex is to pitch ongoing support near the end — during user acceptance testing, when the relationship feels warm. That is exactly the wrong moment. By UAT the client is exhausted, over budget, and so sick of consultants that "and now pay us monthly" lands like a threat.

Sell it on Day 0, inside the original implementation proposal, framed around the one fact every Workday buyer already half-fears: Workday ships two major feature releases a year. Without a team dedicated to consuming each one, the multi-million-dollar platform you just bought drifts toward obsolete inside 18 months. Position the engagement as continuous optimization tied to that release cadence — not "support." You are not selling insurance against breakage; you are selling the thing that keeps the investment alive.

2. Sell Managed Capacity, not time-and-materials

The expiring hour bucket is a race to the bottom and a forecasting nightmare. Replace it with a monthly subscription to a defined slice of capacity — say, "20 hours/month of functional configuration plus release-readiness." It reads as a fixed monthly fee, it renews by default, and it shows up on your P&L as exactly the predictable revenue buyers pay 3x for. The AMS market is projected to grow at over 21% CAGR through 2035, so the demand to absorb this model is already there.

The number to watch is your attach rate — the share of implementation clients who sign AMS. Below 20% and you are building projects, not a business. Top Workday partners clear 40%+. Fix the attach rate and you fix the valuation. Start Monday: pull your last ten go-lives and count how many converted to recurring. That ratio is the single best predictor of what your firm will sell for.