The practical answer

- Short answer

- Don't sell your NetSuite practice for a 4x multiple. Follow this 18-month roadmap to shift revenue mix, extract the founder, and target 10x+ valuations.

- Best fit

- Industry: IT Services / ERP Ecosystem. Function: Operations / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Peak EBITDA multiple for specialized IT consulting firms in 2025, compared to 8.8x for generalists.

The 'Service Multiple' Trap in the NetSuite Ecosystem

If you are a NetSuite Solution Provider or Alliance Partner doing $10M to $50M in revenue, you are sitting on a valuable asset. But unless you restructure your operations in the next 18 months, you will likely sell it for 50% of its potential value.

Here is the brutal math of the 2026 IT services M&A market: Generic professional services firms trade at 5x-7x EBITDA. Specialized, IP-enabled partners with predictable revenue trade at 10x-14x EBITDA.

For a founder with $3M in EBITDA, that is the difference between a $15M exit (which might barely cover taxes and earnouts) and a $40M exit (which is life-changing wealth).

The problem is that most NetSuite partners are built for cash flow, not exit value. They rely on:

- Founder-led sales: You close the big deals because you are the only one who knows the "art of the possible."

- Lumpy project revenue: You feast on big implementations but starve when the pipeline dries up.

- Tribal knowledge: Your best functional consultants carry the delivery methodology in their heads.

Private Equity buyers see this profile and price it as a "risky job shop." To get the premium multiple, you need to execute an 18-month operational pivot.

Private Equity buyers don't buy 'consulting hours.' They buy systems that generate predictable cash flow. If your revenue walks out the door every evening, you don't have a company; you have a job.

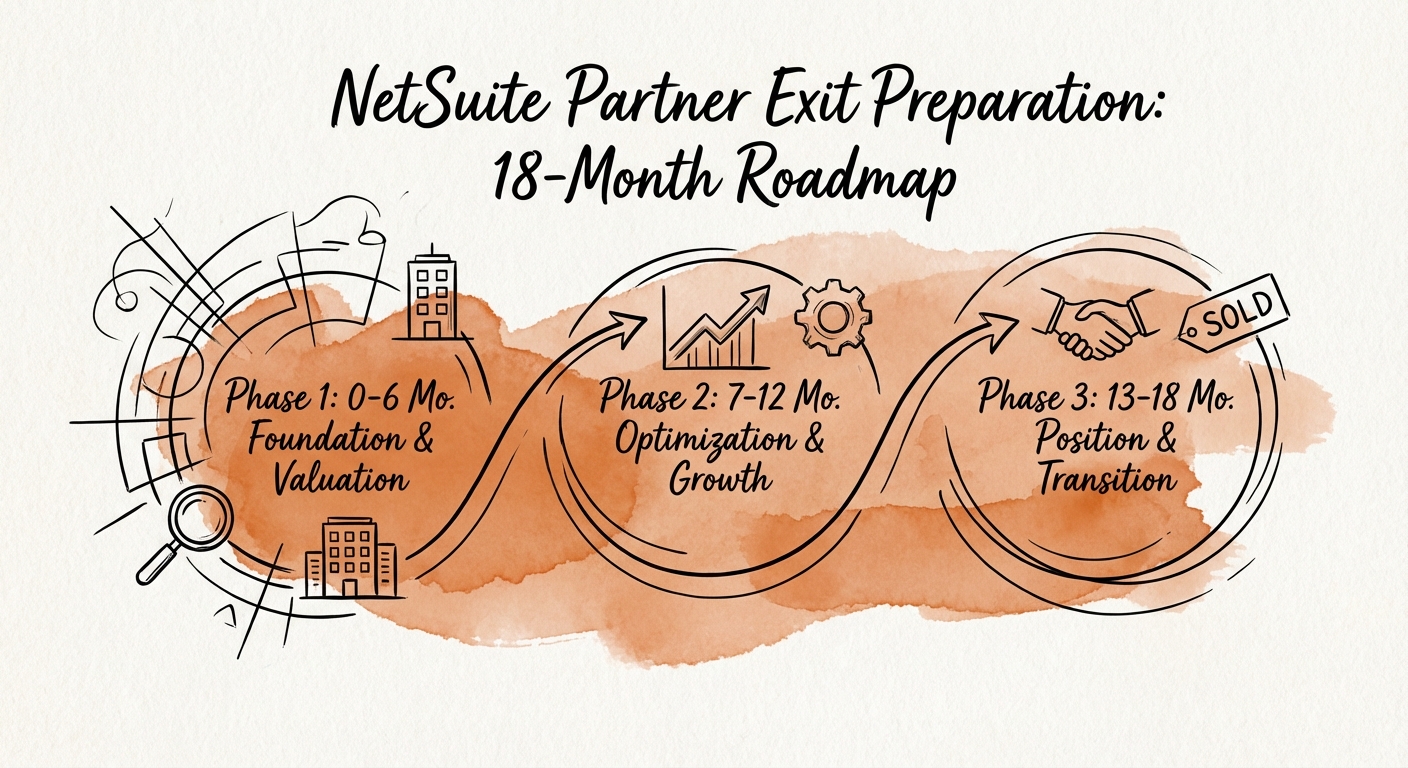

Phase 1: Revenue Architecture (Months 18-12)

The first six months are about changing what you sell, not just how you sell it. Buyers in the Oracle ecosystem are allergic to pure one-time implementation revenue. They want to see "stickiness."

Shift from 'Projects' to 'Managed Services'

Stop selling 300-hour blocks of support. Package your post-go-live support into annual Managed Services (AMS) contracts. Your goal is to get Recurring Revenue to >30% of total revenue. Valuation data from 2025 shows that firms crossing this 30% threshold see a 2-turn expansion in their EBITDA multiple.

Productize Your IP (The 'SuiteApp' Factor)

If you have built a custom integration for 3PL logistics or a specific revenue recognition workflow for SaaS clients, document it. Better yet, package it. You don't need to be a full-blown ISV, but you must demonstrate that your delivery relies on proprietary assets, not just hours. This defensibility is what strategic acquirers pay for.

Phase 2: Founder Extraction (Months 12-6)

Once the revenue mix is healthier, you must fire yourself. If you are the lead rainmaker or the escalation point for every red account, your business is unsellable.

The 'Second Layer' Test

Can your VP of Sales close a $500k deal without you in the room? Can your Delivery Director handle a failed go-live without your intervention? If the answer is no, you have a Key Person Dependency issue that will trigger a massive earnout structure (locking you in for 3+ years post-sale).

Metric to Watch: Track the percentage of revenue attached to deals where you were the primary closer. In Month 12, it might be 60%. By Month 6, it needs to be <10%.

Phase 3: Financial Hygiene & Data Room (Months 6-0)

The final sprint is about ensuring your numbers tell the story you've built. In the NetSuite world, this means impeccable hygiene around revenue recognition.

ASC 606 & The 'WIP' Trap

We see countless NetSuite partners fail diligence because they recognize revenue on invoicing rather than milestone delivery. When a PE firm's Quality of Earnings (QofE) team looks at your books, they will restate your EBITDA downward if you've been aggressive. Clean this up now. You want your TTM (Trailing Twelve Months) EBITDA to be bulletproof before you sign an LOI.

The Partner Ecosystem 'Health Check'

Your standing with Oracle NetSuite matters. Are you hitting your tier targets? Do you have a diverse channel of referrals, or does 80% of your business come from two specific NetSuite reps? Customer concentration is bad; channel concentration is fatal.

The 18-month timeline is unforgiving. You can't cram three years of operational maturation into a 60-day exclusivity period. Start now.