The practical answer

- Short answer

- Why most NetSuite implementation partners flatten near $10M, the utilization and EBITDA numbers that signal the stall, and the SuiteApp-plus-managed-services mix buyers actually pay up for.

- Best fit

- Industry: Professional Services / ERP. Function: Operations & Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 68.9% Average Billable Utilization for Services Firms in 2025 (Down from optimal 75%)

The deal where $12M of revenue was worth half what the founder thought

A NetSuite implementation partner with $12M in trailing revenue wanted 10x EBITDA. The buyer opened at 5x. The founder was furious — same Oracle alliance badge, same certified consultants, same client logos as the shops trading higher. What collapsed the number was one line in the data room: of that $12M, roughly $8M was one-and-done implementation work with no renewal attached, and the "managed services" line was hourly support blocks dressed up as a recurring product. Take out the founder, and you take out the revenue.

This is the quiet trap in a market that looks like a layup from the outside. Oracle NetSuite is compounding at 18% year-over-year, clearing $1.0 billion in quarterly revenue in fiscal 2025 (Anchor Group, 2025). Implementations are everywhere. Yet the typical partner gets stuck somewhere between $8M and $10M and cannot figure out why more demand isn't turning into more margin.

The honest answer: you scaled the part of the business that doesn't scale. You hit $3M-$5M on referrals and heroics — you scoped the deal, you closed it, you took the 11pm go-live escalation. At $8M-$10M you've hired your way to twice the headcount, but the delivery model is the same one that only worked because you were the quality control. The number on the page that gives this away is utilization. Across services firms it's running near 68.9% against a healthier target around 75% (Deltek SPI, 2025). You're carrying bench you can't bill because deals slip and you "want to be ready," and that bench is eating the margin that used to look like 25% back when you underpaid yourself.

A buyer doesn't pay 10x because you implement NetSuite well. They pay it because your firm books revenue in March that someone else already committed to in October — and you weren't in the room when they signed.

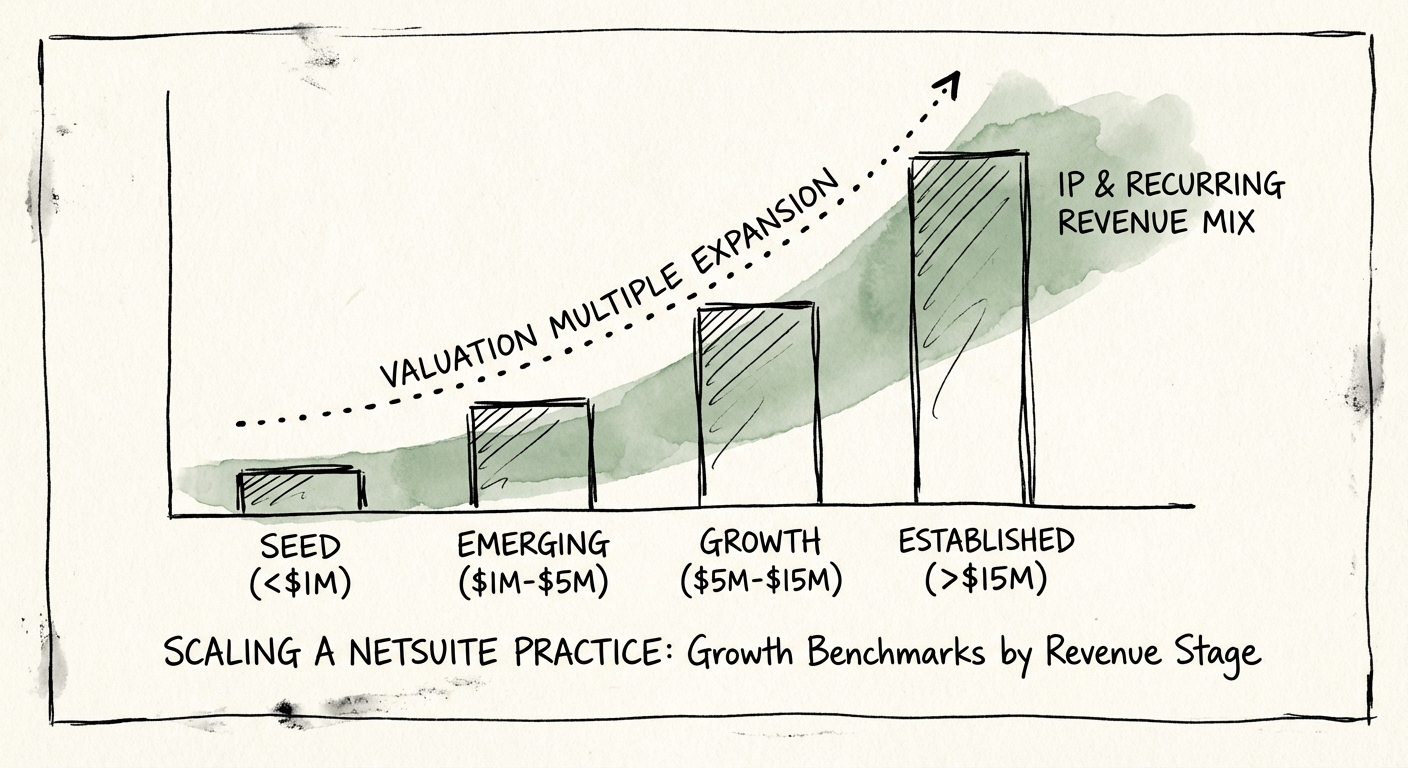

What changes at each stage isn't size — it's where the revenue is allowed to come from

The partners who get unstuck don't add bodies. They change the shape of their revenue, and the valuation multiple follows the shape, not the headcount. Here's how the curve actually moves for NetSuite practices.

$1M-$5M — the "yes to everything" shop

Retail today, a nonprofit next week, a 3PL after that. Every implementation is a custom snowflake, so nothing you built last quarter makes this quarter faster. Buyers price this at roughly 4x-5x EBITDA because the asset is the founder's calendar. The one number worth defending here is gross margin: if delivery isn't clearing 50%, you're not scaling a business, you're underpricing your own labor. Fix the rate card before you fix anything else.

$5M-$15M — pick a lane and build the bundle

This is where the math turns. You become the NetSuite partner for, say, subscription SaaS revenue recognition, or for medical-device inventory and lot tracking, and you stop rebuilding the same SuiteApp configuration on every engagement. Pre-configured industry bundles and reusable SuiteScript can cut implementation time meaningfully, which is what finally pulls utilization back toward 75% — not because people work harder, but because they stop scoping from a blank page. Target 60% of revenue concentrated in your top two verticals. That concentration is what moves the multiple to roughly 6x-8x: a buyer can underwrite a niche you dominate, but not a grab bag.

$15M-$50M — own the renewal, not just the build

Now you graduate from Alliance Partner to Solution Provider: you carry the license relationship and the renewals, and you run a real managed-services practice — monthly optimization retainers, not break-fix hours billed after the fact. The goal is 30%+ of revenue recurring, and that's where multiples reach 10x-12x (or revenue multiples if the IP is the product). The reason is unglamorous and decisive: recurring revenue is worth materially more at exit than project revenue, often 2x-3x on the same dollar, because it survives a Tuesday when the founder is on vacation (Market Research Intellect, 2025).

Three tests a NetSuite buyer runs on your business before they name a number

Go back to that $12M founder. The gap between his 10x and the buyer's 5x wasn't a negotiation — it was three diligence questions he failed. Run them on yourself now, while there's still time to change the answer.

1. Is there a SuiteApp or accelerator with your name on it? Not a folder of scripts you reuse internally — a packaged, ideally listed product that creates a reason for the client to stay and for a buyer to call you tech-enabled instead of "another services firm." This is the line item that moves you off the commodity shelf. Say a 60-person practice that productizes its lot-tracking config into a published SuiteApp: that one asset reprices the whole company.

2. Can someone who is not you scope a $500K project within 10% accuracy? Pull your last ten fixed-bid engagements. If 20-30% blew past budget — the typical overrun rate once the founder stops personally scoping — the buyer assumes every future deal carries that risk and discounts accordingly. Documented, repeatable scoping isn't a process nicety; it's what lets the firm function without you in the loop.

3. Is your "managed services" actually recurring, or is it hourly support with a nicer label? Monthly optimization retainers under contract are an asset. Blocks of break-fix hours are consulting you haven't sold yet. Buyers can tell the difference in about four minutes of looking at your renewal rates.

The Monday move: open your revenue report and tag every dollar as either project, IP/license, or contracted recurring. If recurring is under 15%, that — not your pipeline — is the constraint on your next valuation. For how this same logic plays out across the whole sale process, see our breakdown of exit-readiness signals.