The practical answer

- Short answer

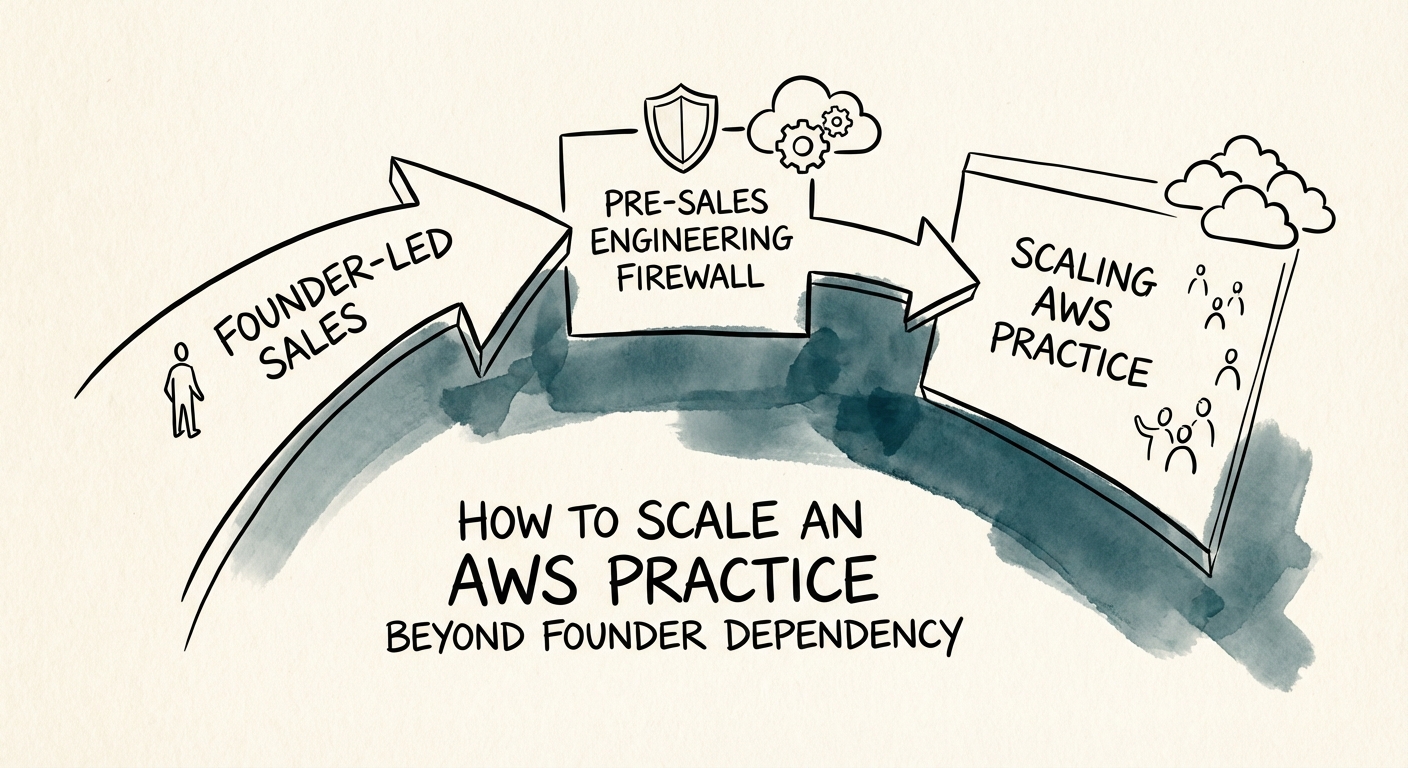

- Stuck at $5M revenue? Here is the diagnostic playbook to scale your AWS practice beyond founder-led sales, increase valuation multiples, and capture the $7.13 ecosystem multiplier.

- Best fit

- Industry: Cloud Consulting / MSP. Function: Operations & Sales

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- $7.13 Revenue partners generate for every $1 of AWS sold (Omdia 2025)

The 'Hero' Trap: Why AWS Practices Stall at $5M

You built this company on your ability to solve problems that confused everyone else. In the early days, your "Superpower"—the ability to jump into a failing migration, re-architect the VPC on the fly, and save the client's launch—was your competitive advantage. It's how you got to $3M ARR. It's how you got to $5M.

But at $5M-$10M, that same superpower becomes your valuation killer. We call this the "Founder-Led Ceiling."

In the 2026 AWS ecosystem, the market rewards specialized systems, not individual heroes. According to Omdia and Canalys data, the "Partner Ecosystem Multiplier" has hit $7.13 in service revenue for every $1 of AWS consumption sold. But you cannot capture that multiplier if you are personally architecting every deal.

The Valuation Gap

The market is currently bifurcated. On one side, we see "Body Shop" consultancies trading at 4x-6x EBITDA. These firms rely on founder relationships and ad-hoc delivery. On the other side, we see Tech-Enabled MSPs and IP-led partners trading at 10x-14x EBITDA.

The difference? Transferability.

When a Private Equity buyer looks at your Founder Delegation Paradox, they ask one question: "If you became unavailable for a month, does the revenue stop?" If the answer is yes, you don't have a business; you have a high-paying job with massive liability. To break the $10M ceiling, you must stop being the Chief Architect and start being the Chief Systems Engineer of your own company.

You can have a $5M lifestyle business where you are the hero, or a $50M asset where you are the architect. You cannot have both.

The System: Replacing Intuition with Engineering

Scaling beyond founder dependency requires three specific shifts in your operating model. This isn't about "hiring better people"—it's about building better guardrails.

1. Productize the Service Catalog

Stop selling "whatever the client needs." Founder-led sales often default to "Yes, we can do that," which leads to custom, unscalable delivery nightmares. You need to package your expertise into SKUs. Instead of "Cloud Migration Services," sell a "6-Week Redshift Modernization Accelerator."

This allows you to:

- Standardize pricing (protecting margins).

- Hire mid-level engineers who follow a playbook (lowering delivery costs).

- Predict outcomes (increasing customer NRR).

2. The 'Pre-Sales Engineer' Firewall

You are likely the only person currently capable of scoping complex deals accurately. This is a failure of documentation. You must implement a Pre-Sales Solutions Architecture (SA) layer. Download your brain into scoping calculators, questionnaires, and reference architectures.

The Metric to Watch: If your Revenue Per Employee (RPE) is below $200,000, you are over-staffed or under-priced. High-performing AWS practices in 2026 operate closer to $250k-$300k RPE by leveraging automation and reusable IP rather than just throwing bodies at tickets.

3. From Projects to Managed Services (The Margin Shift)

Project revenue is lumpy and exhausting. The goal is to convert every migration into a long-term managed service contract. But you can't do this if your managed service is just "we'll fix it if it breaks." It must be proactive.

Compare the margins: Managed Services vs. Professional Services. Pure professional services struggle to break 40% gross margin due to the "bench tax." Tech-enabled managed services can hit 60%+ because software (monitoring, automation, scripts) does the work, not hours.

The Exit: How to Position for the 12x Multiple

To attract a premium buyer or growth equity partner, you need to prove that the machine runs without you. This is where "Founder Extraction" moves from theory to data room reality.

The 'Key Person Dependency' Audit

Conduct a disciplined audit of your calendar. Any task that only you can do is a threat to your exit value. If you are still approving code merges, you are creating technical debt in your org chart.

Leveraging AWS Specializations

In 2026, generalist "Advanced" partners are a commodity. The premium valuations go to partners with competencies (Security, Data & Analytics, Migration) and service delivery programs (SDP). These badges are not just marketing fluff; they are third-party validation that your process meets a standard, independent of the founder.

The Strategic Pivot:

- Phase 1 (Founder-Led): $0-$5M. You sell trust. Valuation: 1x Revenue.

- Phase 2 (Process-Led): $5M-$20M. You sell a methodology. Valuation: 8x EBITDA.

- Phase 3 (Platform-Led): $20M+. You sell outcomes/IP. Valuation: 12x+ EBITDA.

The jump from Phase 1 to Phase 2 is the hardest thing you will ever do. It requires you to fire yourself from the jobs you love (architecture, closing deals) to do the job you hate (building governance). But that is the price of the multiplier.