The practical answer

- Short answer

- A single blended budget-vs-actuals number hides departmental margin leaks. Here are the category-specific monthly variance thresholds PE operators should enforce.

- Best fit

- Industry: Private Equity / B2B SaaS. Function: FP&A / Finance

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

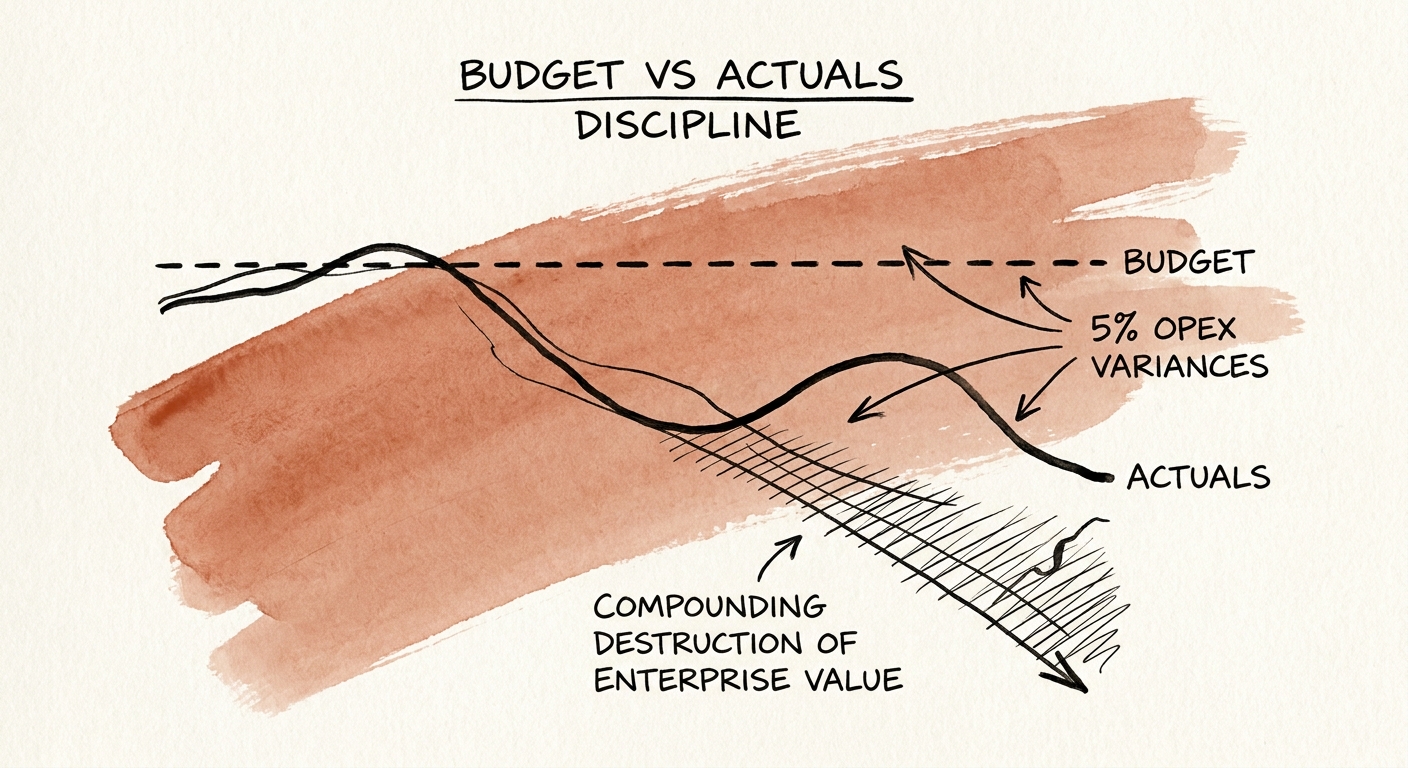

- 2.5% Maximum acceptable monthly OPEX variance for top-quartile FP&A teams.

It is the fourth business day of the month. The portfolio CFO of a $40M ARR tech-enabled services company sends the board package, and the budget-vs-actuals summary lands on a single, reassuring line: total OPEX, 3.8% over plan. Nobody flags it. Three percent feels like rounding. Everyone moves on to the pipeline slide.

That single blended number is the most dangerous artifact in finance, and I have watched it conceal the same fire across three different sponsors. Decompose that 3.8% and the story is never "everything ran a little hot." It is engineering payroll 9% over because two backfills landed early, software spend 14% over from a renewal nobody modeled, and revenue quietly 1.5% under plan that the overages politely cancel out on the summary line. The blend is not a metric. It is camouflage.

Here is the part operators underweight: in a recurring-revenue, services-heavy business, cost lines do not reset at month-end. A team that lands 6% over on payroll in February has not "missed February." It has re-baselined March, April, and every month after, because nobody unwinds a hire or claws back a signed vendor contract. The overage becomes the new normal, and by the time it surfaces as a missed quarter it has already eaten real EBITDA.

This matters more in the current hold cycle than it did five years ago. Bain & Company's Global Private Equity Report is blunt that margin expansion, not multiple arbitrage, has to carry value creation now. You cannot expand a margin you cannot see, and a blended monthly variance number is engineered to keep you from seeing it. If you are discovering a 14% software overrun at the quarterly board meeting instead of on day four, you have already lost the quarter — and you have skipped past the board reporting metrics that actually matter.

We do not accept "timing" as an explanation for a budget variance. If the timing was wrong, the forecast was wrong, the cash model was wrong, and the business was flying without instruments.

Set the threshold by what the line item actually is

The fix is not "watch budget-vs-actuals more closely." It is to stop reporting one tolerance band for fundamentally different kinds of spend. A revenue miss and a payroll miss tell you opposite things about a business, so grading them against the same percentage is how problems hide. I hold portfolio companies to three separate tripwires, each tied to how controllable and how sticky the line actually is.

Top-line revenue and ARR: flag at -2%. Upside is always welcome; nobody calls a meeting because bookings ran hot. But a 2% downside miss in a recurring-revenue model is rarely random. It is the early read on either gross retention slipping or a sales pipeline that stalled a quarter ago and is only now showing up in recognized revenue. The number is small precisely because it is leading — by the time it is large, it is structural.

Headcount and payroll: flag at 1%. This band is tight on purpose. Headcount is the most knowable variable on the P&L — you control the offer letters and the start dates. A payroll miss above 1% is not a forecasting mystery; it means the company hired ahead of revenue, or it committed to a reduction and then flinched. Either way it is a decision someone made, not weather that happened to them.

Software and vendor OPEX: cap at 2.5%. Gartner's FP&A research puts top-quartile finance teams under roughly this aggregate monthly OPEX variance, which makes it a fair external bar rather than an arbitrary one. The reason this line breaks discipline first is SaaS sprawl and contractor creep — spend authorized inside departments that finance never sees until renewal. The enforcement test is simple: if finance cannot attribute the variance down to the specific vendor within 48 hours of close, you do not have a forecasting problem, you have a visibility problem. That is the gap a weekly flash report is built to close, well before anything reaches the monthly board package.

The thresholds are 10% of the work — enforcement is the rest

Setting the numbers is easy. The discipline lives in what happens when someone breaches one, and there are two rules I do not relax.

The word "timing" is banned from the variance explanation. "It's just timing — the expense hit in April instead of May" is the most common explanation a department head will offer, and it is a non-answer. If an expense moved a month, the forecast was wrong, the cash model was wrong, and the business was operating without instruments. So the explanation has to name a root cause: was the vendor contract misread? Did sales miss the tier they projected? Did a start date slip and never make it back to finance? Each of those is a fixable process gap. "Timing" is a request to stop looking.

Two consecutive breaches triggers a discretionary-spend freeze. If a department leader — CMO, VP Engineering, head of customer success, anyone — blows the 2.5% OPEX threshold two months running, their discretionary authority defaults to zero-based: every dollar gets CEO sign-off until they re-earn the latitude. This pushes accountability to the operator who actually made the spend instead of leaving the CFO to reconcile a mess they did not create. It also changes behavior fast, because the freeze is a consequence, not a memo. The Association for Financial Professionals has documented that pairing BvA triggers with rolling forecasts can lift forecast accuracy materially — the mechanism is psychological as much as procedural.

The exit case for all of this is straightforward. EBITDA is a lagging number; by the time it prints, the decisions that made it are months old. A management team that lands inside its category thresholds month after month is the team a diligence process trusts — which shows up as a cleaner quality-of-earnings report, fewer disclosure-schedule surprises, and a defensible number at the closing table. If you have ever wondered why your board doesn't trust your numbers, start Monday: split the blended variance line into revenue, payroll, and OPEX, set the three bands, and watch where the fire actually is.