The practical answer

- Short answer

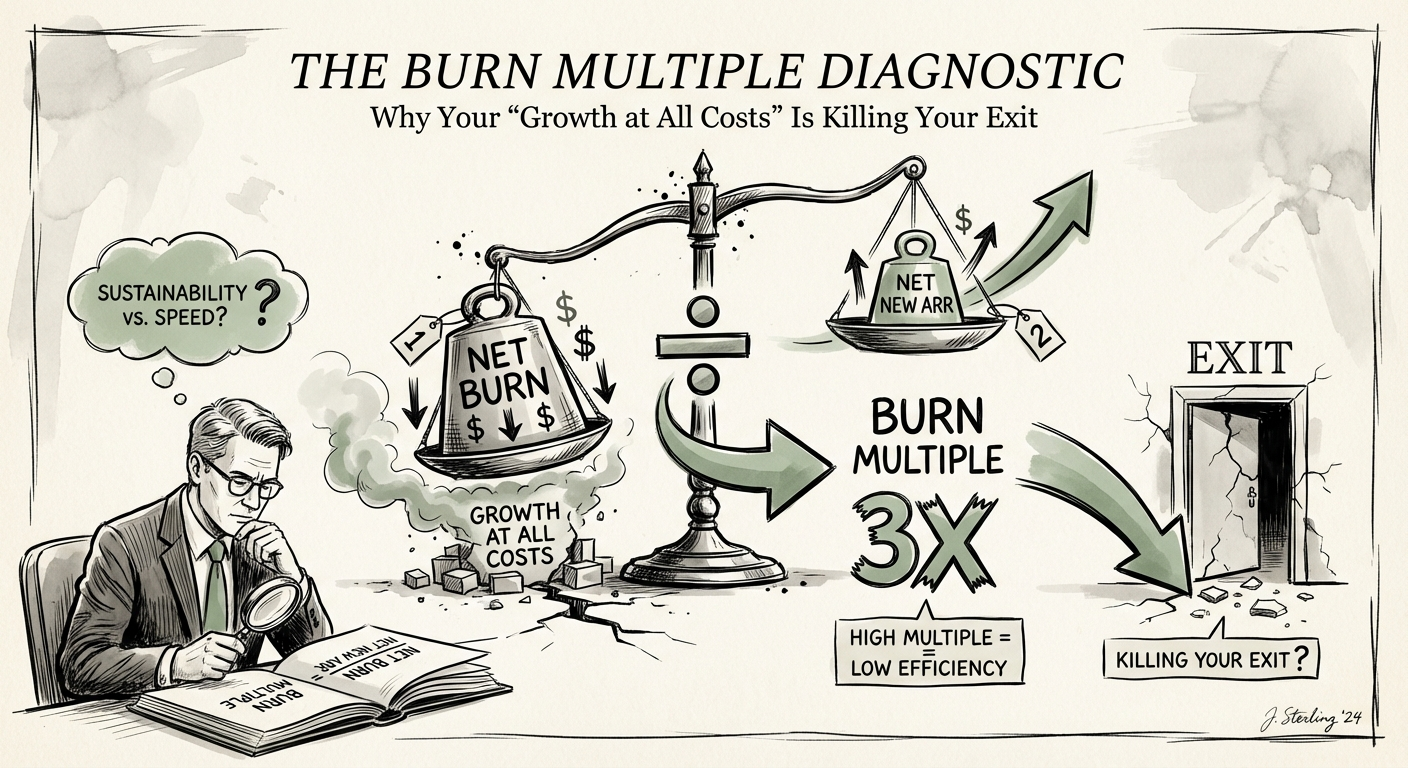

- Is your startup burning cash too fast? Use the Burn Multiple formula (Net Burn / Net New ARR) to diagnose your capital efficiency. 2026 benchmarks included.

- Best fit

- Industry: B2B SaaS / Tech Services. Function: Office of the CFO

- Operating path

- Financial Infrastructure → Commercial Performance → Valuations

- Key metric

- 1.5x The maximum safe Burn Multiple for Series B companies in 2026.

The Truth Serum for Your P&L

If you are a Series B founder, you have likely been trained to worship at the altar of “Growth at All Costs.” For the last decade, that was the playbook: triple, triple, double, double, double. If you burned $3 to get $1 of ARR, nobody blinked—as long as the topline chart moved up and to the right.

That playbook is dead. In the current rate environment, capital is no longer a commodity; it is a constraint. Investors have shifted their obsession from raw growth to efficient growth. The metric that exposes the truth about your efficiency isn't EBITDA (which you're likely miles away from) or the Rule of 40 (which can be gamed by lumpy growth). It is the Burn Multiple.

The Formula

Popularized by David Sacks of Craft Ventures, the Burn Multiple is the single most unforgiving metric in your board deck because it captures every sin in your company—bloated headcount, inefficient marketing, high churn, and runaway cloud costs. The formula is deceptively simple:

Burn Multiple = Net Burn / Net New ARR

If you burned $2M in Q1 to generate $1M in Net New ARR, your Burn Multiple is 2.0x. You spent two dollars to buy one dollar of growth. In 2021, that was acceptable. In 2026, that is a red flag that will stall your next round.

In 2021, if you burned $3 to get $1 of ARR, nobody blinked. In 2026, a Burn Multiple over 2.0x isn't just inefficient—it's an existential threat to your next fundraise.

The 2026 Efficiency Grid: Where Do You Stand?

You cannot fix what you do not measure, and you cannot measure without a baseline. Based on data from 2025-2026 reporting cycles across VC portfolios (including data from Bessemer, ICONIQ, and Craft), the bar has tightened significantly.

Here is the diagnostic grid for a Series B/C company ($10M - $50M ARR):

- < 1.0x (The Efficient Frontier): You are generating ARR faster than you are burning cash. This is elite status. Investors will compete to lead your next round because you control your own destiny.

- 1.0x – 1.5x (The Good Zone): This is the new standard for “healthy.” You are investing in growth, but your unit economics are sound. You have a clear path to profitability.

- 1.5x – 2.0x (The Danger Zone): You are suspect. Unless your year-over-year growth is >100%, investors will question your operational discipline. You are likely over-hired or have a leaky bucket problem in Customer Success.

- > 2.0x (The Death Spiral): You are lighting money on fire. If you are not growing at triple-digit percentages, you are uninvestable in this market. You need to cut burn immediately, not “grow into it.”

The "Heroics" Tax

High burn multiples often correlate with what we call the “Heroics Tax.” If your multiple is 2.5x, it usually means you are throwing bodies at problems instead of building systems. You have hired more sales reps to cover for a bad product, or more support staff to cover for bad implementation processes. You aren't scaling; you're just getting heavier.

How to Fix a Broken Multiple (Without Killing Growth)

If your diagnostic returns a 2.2x, panic is not the strategy. Operational engineering is. Lowering your Burn Multiple requires a pincer movement: increasing Net New ARR (the denominator) while compressing Net Burn (the numerator). But you must pull the right levers.

1. The Sales Efficiency Audit

The fastest way to fix the denominator is to stop carrying dead weight. In many Series B firms, 20% of the sales reps generate 80% of the revenue. The bottom 30% are often yielding a negative ROI when you factor in CAC. Audit your rep ramp times and quota attainment. Cutting the bottom quartile of performers often improves total output because it frees up management bandwidth and leads for the top performers.

2. The Churn Plug

Net New ARR is composed of New Sales + Expansion - Churn. Most founders obsess over New Sales. But if your Gross Revenue Retention (GRR) is <90%, you are trying to fill a bucket with a hole in the bottom. Improving retention by 5% has the same impact on your Burn Multiple as growing new sales by 20%, but costs significantly less.

3. The Cloud & Tooling Purge

Review your "non-headcount" burn. We frequently find Series B companies paying for 500 seats of software when they have 200 employees. Or cloud bills that have grown linearly with revenue because no one refactored the code. This is where technical debt becomes financial debt. A 10% reduction in OpEx often drops straight to the bottom line without impacting growth velocity.