The practical answer

- Short answer

- A $20-100M ARR SaaS company will overpay full-stack engineers by ~$35K and underpay its data-platform lead. Here are 2026 bands and how to rebuild them.

- Best fit

- Industry: B2B SaaS. Function: Talent & Operations

- Operating path

- Team & Hiring → Operational Excellence → Transaction Execution Services

- Key metric

- Role-by-role Compensation bands should separate scarce specialist roles from broad generalist capacity.

Two offer letters, same engineering org, same week

Picture a $40M ARR vertical-SaaS company sitting inside a private equity portfolio. In a single week, the talent team approves two offers. One is a Senior Full-Stack Engineer at $180,000 base, because the band has read that number since the 2021 hiring frenzy. The other is a backfill requisition for a data-platform engineer the company already lost — to a competitor who paid $215,000 for skills the legacy band priced at $160,000. Both numbers came from the same compensation file. Both are wrong, in opposite directions.

That is the actual shape of comp risk in mid-market SaaS right now: not a single ranges-are-stale problem, but a widening split inside one spreadsheet. The labor market has settled from its peak, yet plenty of talent teams still set engineering and go-to-market pay using datasets carried over from the zero-interest-rate years. The cost shows up as overpayment for capacity that is now abundant and underpayment for the handful of roles that actually move the product roadmap.

And the source matters. You cannot anchor pay for a mature, cash-generating enterprise-software company to a Carta State of Startup Compensation report weighted toward venture-funded startups burning toward a Series B. Those companies pay for growth optionality with someone else's money. A $20M-$100M ARR business with a defined exit window and real margin targets is buying something different — and its bands should reflect role scarcity, geography, and cash discipline, not a founder's willingness to dilute.

Pay bands fail quietly. You keep one offer letter on the desk at $180K, lose your only data-platform architect to a $215K counter, and call it a market problem. It was a banding problem.

Where the spread actually lives

Stop treating "engineering" as one band. By 2026 the inside of the engineering org has pulled apart into two pay realities, and a single range hides the gap that costs you money on both ends.

The roles you are quietly overpaying

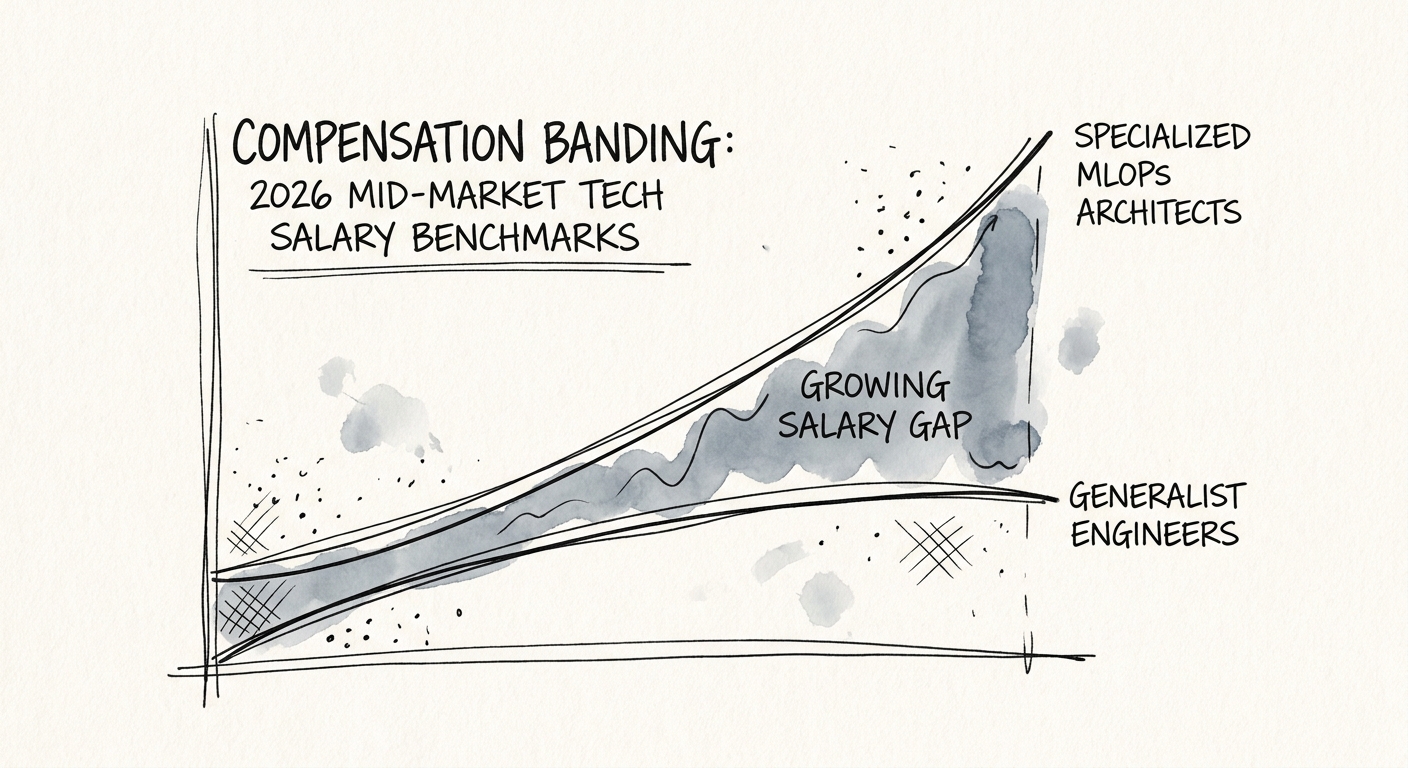

Senior full-stack developers, standard front-end engineers, and legacy QA-automation roles have become abundant — partly because AI-assisted coding compressed the productivity gap between a strong generalist and an average one, partly because the post-boom layoffs flooded the pool. In the $20M-$100M ARR tier, a Senior Full-Stack Engineer should land between roughly $135,000 and $155,000 base. If your file still reads $180,000 for that profile, that is about $35,000 per head of pure margin leakage — and on a 15-person team where five seats fit this description, you are looking at six figures of annual EBITDA you are handing back for no incremental output. The CompTIA State of the Tech Workforce report shows hiring volume for generalized IT roles falling year-over-year as budgets move toward specialized integration and AI infrastructure. The demand simply is not chasing this profile anymore. Your band should follow.

The roles you cannot afford to lose

The other side runs hot. MLOps engineers, cloud-security architects, and data engineers fluent in modern governance and applied-AI infrastructure now clear roughly $195,000 to $225,000 base in competitive markets. These are not seats to bargain-hunt. When you lose the one person who owns your data platform, you do not just pay a recruiter fee — you absorb roadmap slip, a re-onboarding ramp measured in quarters, and the risk that the replacement inherits decisions they cannot explain. Underpaying here is the most expensive way to save $20,000.

GTM has cooled, not collapsed

On the revenue side, the wild VP of Sales package is gone. At around the $30M ARR mark, VP of Sales on-target earnings have settled near $260,000 to $280,000 on a disciplined 50/50 base-to-variable split. Guaranteed draws and non-recoverable sign-on bonuses are an artifact of a market that no longer exists. The mechanics of structuring that package so the variable half actually protects unit economics are worth getting right — we walk through them in The VP of Sales Compensation Trap: Why Traditional OTE Kills Unit Economics. The headline for banding: the OTE number is fine, but the split and the recoverability are where deals get made or lost.

Rebuilding the file so it stops drifting

Re-pricing once does not fix this. A static band starts decaying the day you publish it. You need an architecture that holds geography honest, treats equity as a real currency, and refreshes fast enough for the roles where the market actually moves.

Make location a multiplier, not an afterthought

Remote hiring does not obligate you to pay San Francisco rates to an engineer living in Columbus. Run a deliberate geographic multiplier: the highest-cost labor markets set the baseline, mid-cost metros take a moderate discount, and lower-cost regions take a larger one when the role can genuinely be filled outside the premium pools. The Robert Half Salary Guide is a useful localized input, but it is input, not the answer — the final band still has to weigh how scarce the skill is and how much of the roadmap rides on the seat.

Trade equity for cash on purpose

A mid-market SaaS company cannot out-cash a public tech giant, so equity has to do real work for the scarce specialists. Make it an explicit trade rather than a sweetener: offer a high-equity / lower-cash track and a standard-cash / lower-equity track, and let the candidate choose. Preference is useful signal about how someone thinks about the upside — but it is one input, not a hiring test on its own. The payoff is that you protect burn while reserving the cap table for people who are actually buying into the exit, not just the paycheck.

Review the top of the org twice a year

The annual comp review is too slow for the roles that get poached. For roughly the top 15% of engineering talent — the specialists above — move to a six-month adjustment cadence so you can close gaps before a well-funded competitor opens one. Holding your lead security architect on a 12-month review is how you wake up to a resignation that was avoidable for a fraction of the backfill cost.

The move this quarter is narrow and concrete: pull your current bands, split the engineering range into commodity and scarce profiles, re-price both ends against 2026 data, apply the geographic multiplier, and flag every seat that is overdue for a mid-cycle look. The buffer-the-bench instinct that quietly inflates these numbers deserves the same scrutiny — we unpack it in The 'Growth Bench' Fallacy: Why Your Talent Buffer Can Hurt Valuation. And when you are sizing up a target's whole human-capital picture in diligence, the same discipline applies in The Human Capital Audit: A Quantitative Framework for PE Management Assessment. Comp inertia does not announce itself — it just shows up as a softer margin and a harder exit story.