The practical answer

- Short answer

- An $80k SaaS deal triggers full enterprise procurement but commands zero C-suite attention. That's the outlier zone — where cycle times double and win rates collapse.

- Best fit

- Industry: B2B SaaS. Function: Sales

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 18% Win rate for single-threaded deals over $50k

The deal that takes as long to close as one four times its size

Here is the moment it goes wrong. A founder-CEO, fresh off a growth round, tells the sales team to "move upmarket." The ACV floor jumps from $40k to $80k. For about a quarter, everything looks great — top-of-funnel pipeline balloons, the dashboard glows, the board is happy. Then closed-won revenue quietly flatlines, and nobody can explain why.

What happened is mechanical, not mysterious. At $40k, a single director could expense the software and sign. At $80k, that same purchase crossed an invisible line inside the buyer's org — the threshold where finance demands a business case, security demands a review, and legal demands redlines. The deal didn't get 2x bigger; the buying process got 3x heavier. The cycle that used to close in 80-ish days now drifts past 190. Same product, same pitch deck, same reps — and a sales motion that no longer fits the deal it's chasing.

The benchmark curve makes the cliff obvious. In the 2025 Ebsta and Pavilion B2B Sales Benchmarks, small software deals clear in roughly six to eight weeks, and mid-five-figure deals settle around the 90-day mark. But the moment a deal crosses into the high-five-figure / low-six-figure band, it stops behaving like a bigger version of the last one. It triggers formal procurement, mandatory security review, and multi-departmental consensus — and the timeline lurches toward six months. Deal size versus cycle time is not a gentle upward slope. It's a staircase, and the $80k step is the tallest one in SaaS.

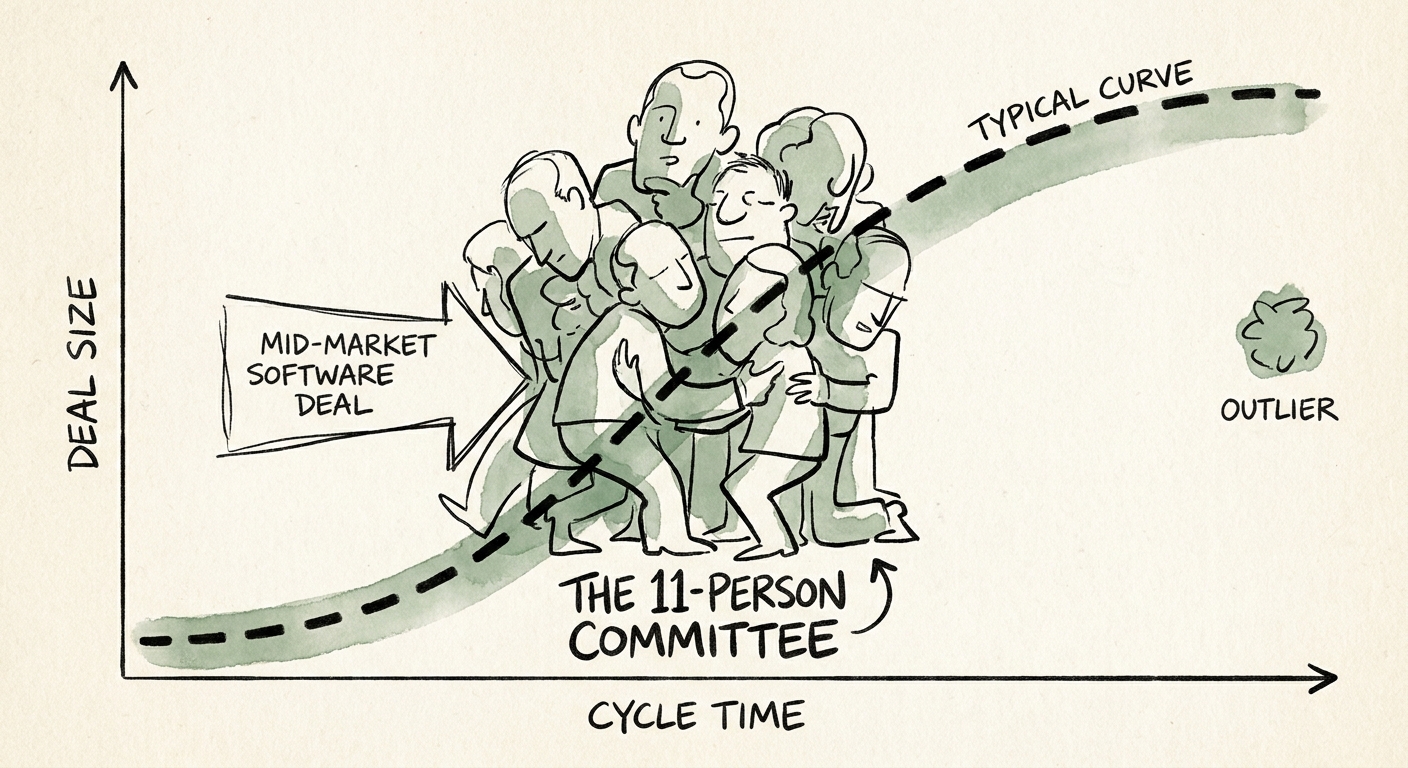

An $80k deal is the worst place in B2B SaaS to be priced: heavy enough to summon eleven gatekeepers, light enough that none of them care. You inherit enterprise friction and keep transactional economics.

The outlier zone: enterprise friction, transactional economics

Map your own deals on a scatter plot — ACV on one axis, days-to-close on the other — and a specific cluster will jump out. Somewhere between $60k and $120k, you'll find deals that took 250 days to close. That's the same calendar time as a $350k enterprise rollout, but for a fraction of the revenue. I call this the outlier zone, and it's the single most dangerous place a scaling SaaS company can park its price book.

The reason is a brutal mismatch. At $80k, your price is high enough to summon the full apparatus of corporate buying — but the strategic stakes are too low to earn an executive sponsor who clears the path. Gartner's research on B2B buying complexity describes the modern enterprise purchase as a committee sport, with a wide group of stakeholders who each have to say yes. A large platform transformation gets a VP who personally drags that committee into a room. Your $80k line item gets a mid-level champion who has no authority to do the same. They love the demo. They cannot herd the CISO, the VP of Finance, and corporate legal to a decision — and they were never going to.

This is where phantom pipeline is born. A rep logs the $80k deal, advances it because the champion is enthusiastic, and then it rots for six to nine months while the rep sends "just checking in" emails into a void. It's not a forecasting hiccup — it's a unit-economics failure wearing a forecasting costume. On a deal of this size, if you don't have at least three engaged contacts actively pulling, your odds of closing fall through the floor. A single-threaded $80k deal isn't a long shot you're nurturing; it's a sales process you're funding that mathematically cannot pay you back.

Two ways out — and the middle is the only losing move

I've rebuilt this exact motion more than once, and the fix always offends people the first time they hear it: you have to pick a side. Either cut the price hard enough to slip back under the procurement threshold and reclaim the high-velocity transactional cycle, or raise it deliberately and repackage the product as a C-level initiative that earns a real executive sponsor. What you cannot do is sit at $80k, inherit all the enterprise friction, and keep collecting mid-market economics. The outlier zone is where deals go to die slowly.

If you choose to climb, the discipline is non-negotiable. Stop measuring a 180-day cycle with 60-day instincts. Install hard qualification gates — if the economic buyer hasn't seen and engaged with a real business case by roughly day 45, the deal is dead no matter what the CRM stage says. Pull it from the forecast immediately. The reps will fight you, because hope feels like progress. Your job is to protect the board's trust in the number, which means a forecast made of three-threaded, executive-sponsored, gate-passing deals — not a graveyard of enthusiastic demos.

Then pay your people for the war you're actually sending them into. Forrester's work on B2B sales points at the same failure pattern: push upmarket without extending ramp times or rebuilding comp around a six-month cycle, and your best reps walk. You cannot starve someone for two quarters while they navigate a corporate procurement maze and expect them to stay. So here's what you do Monday: pull last year's closed-won and closed-lost into a scatter plot, circle the $60k–$120k deals that ran past 150 days, and count how much pipeline and payroll you've sunk into the valley. Then decide — for each segment — whether you're going down to speed or up to value. The curve is physics. You don't get to wish it away; you only get to choose which side of it you build for.