The practical answer

- Short answer

- A month-by-month plan to extract yourself from a $10M-$50M tech company before you sell — and close why founder-dependent firms trade at a 30-50% discount.

- Best fit

- Industry: B2B Tech & Services. Function: Operations

- Operating path

- Founder Extraction → Operational Excellence → Interim Management

- Key metric

- 50% Valuation discount applied to companies with high 'Key Person' risk.

The day your absence becomes a line item in someone else's model

Picture the diligence call. A PE associate is walking your data room, and on every other process map the same answer keeps surfacing: "Founder reviews this." "Founder approves this." "Founder owns the top 10 accounts." They are not impressed by how much you do. They are quietly building a model where the day you leave, a chunk of EBITDA leaves with you. That discount has a name in the deal — key-person risk — and for founder-dependent businesses it routinely lands in the 30-50% range versus systematized peers (Strategic Exit Advisors).

This is the trap specific to a Series B or C tech-services company doing $10M-$50M. At that scale you are profitable enough to be acquired but young enough that you are probably still the highest-leverage employee in the building — the one who closes the wobbly deals, unblocks the stuck migration, and makes the call nobody else will. Every one of those saves feels like leadership. In an acquirer's spreadsheet, each one is a reason to discount the multiple or load the deal with earnout.

The fix is not "delegate more" or "work less." It is a 12-month build with a defined output: a company that produces the same revenue, the same forecast accuracy, and the same client outcomes during a quarter you are not in the room. You are not trying to stop being valuable. You are trying to make your value transferable — which is the only kind a buyer will pay full price for.

The cleanest signal a buyer gets in diligence isn't your revenue chart. It's whether the answer to every hard question in the data room is your name.

What actually happens in each quarter

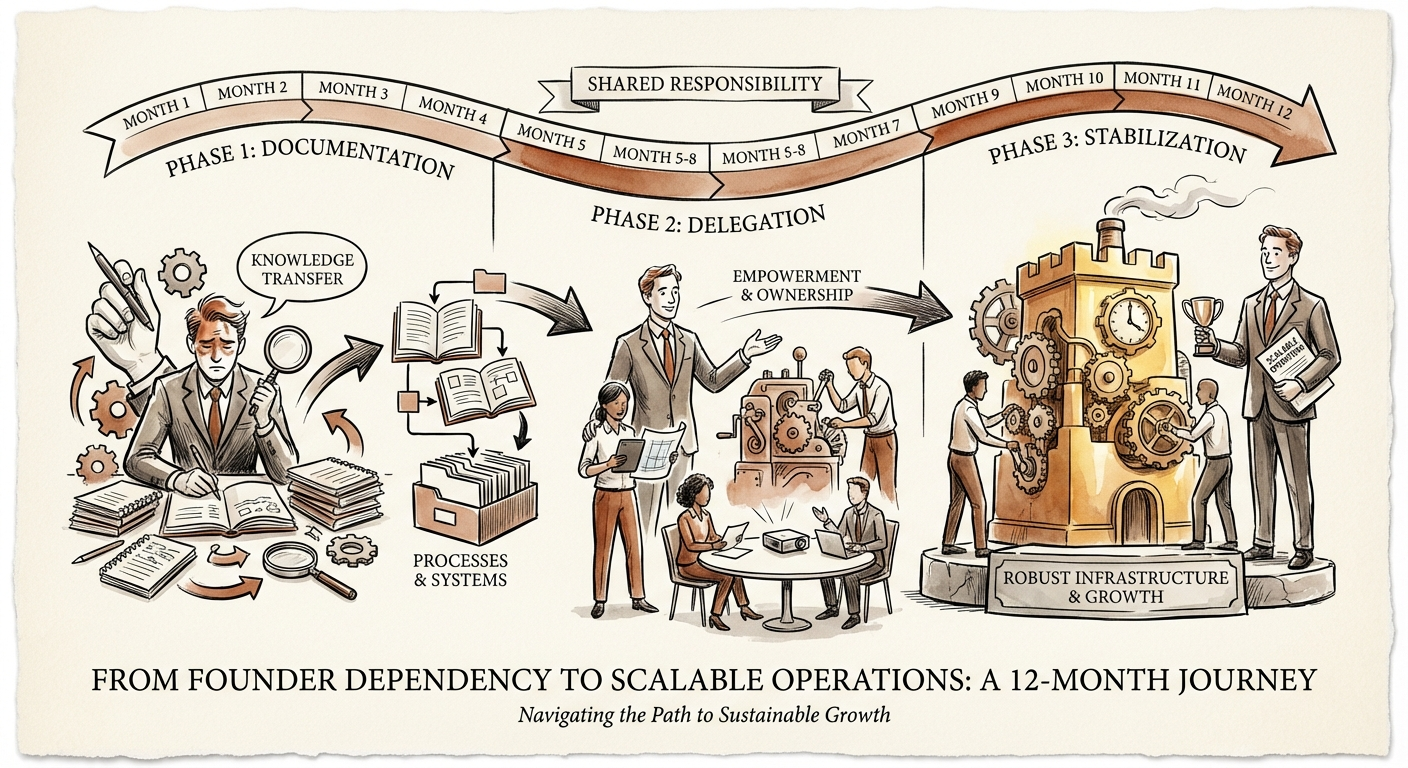

Founder extraction fails when it stays a vibe. It works when it has a quarterly artifact you can point to. Here is the version that survives contact with a real $10M-$50M ops team.

Months 1-3 — Find the bottlenecks, then write down the 80%

Spend the first month doing nothing but logging. Every decision that routes through you — every Slack ping that ends in "ask the founder," every proposal you red-line, every $400 SaaS approval — goes on a list. Most founders are shocked to find how much of that list is decisions a competent manager should never have escalated. Kill those with a spending threshold and a one-page decision-rights doc before you write a single SOP.

Then document the repeatable 80% of sales, delivery, and finance. Not the edge cases — the boring middle. The goal is "good enough for someone else to run," not a polished manual nobody reads. If a new hire can execute it without DMing you, it's done.

Months 4-9 — Install the team in the right order

This is where founders self-inflict the most damage, usually by hiring an expensive VP of Sales to "own revenue" before there's a playbook to own. The transition from founder-led selling to a real sales org takes 12-18 months to stabilize even when it goes well (SaaStr). Hire a VP into a vacuum and they will spend six months reverse-engineering what's in your head, then leave.

Run the two-rep test instead. Before any VP hire, put two ordinary reps on your documented playbook. If they can close deals you would have closed, the system is real and now you can hire a leader to scale it. If they can't, you just learned — for the price of two salaries instead of a botched exec search — that the problem is the motion, not the manager. The same logic applies to delivery and finance: hire builders who industrialize your rough process, not famous names who expect a machine to already exist.

Months 10-12 — Move from driver to governor

By the final quarter your job is the dashboard, not the wheel. Replace founder-gut reporting with the three numbers a board and a buyer actually trust: CAC payback, net revenue retention, and EBITDA margin. The reason M&A deals so often disappoint post-close is that the value was never really transferable in the first place (Harvard Business Review) — you are building the proof that yours is.

The two-week test that's worth more than any pitch deck

Here is the only acceptance test that matters, and you should run it in month 11, not after the deal. Take two weeks completely off. No laptop, no "quick calls," no quietly approving things from a beach. Then come back and look at one thing: did the revenue forecast hold? If pipeline moved, deals closed, and delivery shipped without you, you have manufactured something a buyer will pay a premium for. If the quarter wobbled the moment you went dark, you have found exactly which dependency to fix in the time you have left.

That premium is not abstract. The gap between a 4x EBITDA offer wrapped in a multi-year earnout and an 8x all-cash close is, more often than not, what the data room shows about you. A room full of documented processes, repeatable forecasts, and a management team that performs without the founder reads as a platform for growth. A room where every answer is "the founder handles that" reads as an integration headache to be priced down. Same business, very different check.

So pick your start date and treat the next twelve months like the engineering project it is. You already built the product. The work ahead is building the machine that sells and delivers it without you in the loop — because that machine, not your heroics, is what you actually get paid for when you sell.