The practical answer

- Short answer

- Mid-market CRM migration is driving a valuation surge for HubSpot partners. Discover why PE firms are paying 12x EBITDA for RevOps consultancies.

- Best fit

- Industry: CRM & MarTech. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 12.1x Average EBITDA multiple for mid-market US buyouts in 2025, creating a premium exit window for high-performing technical consultancies.

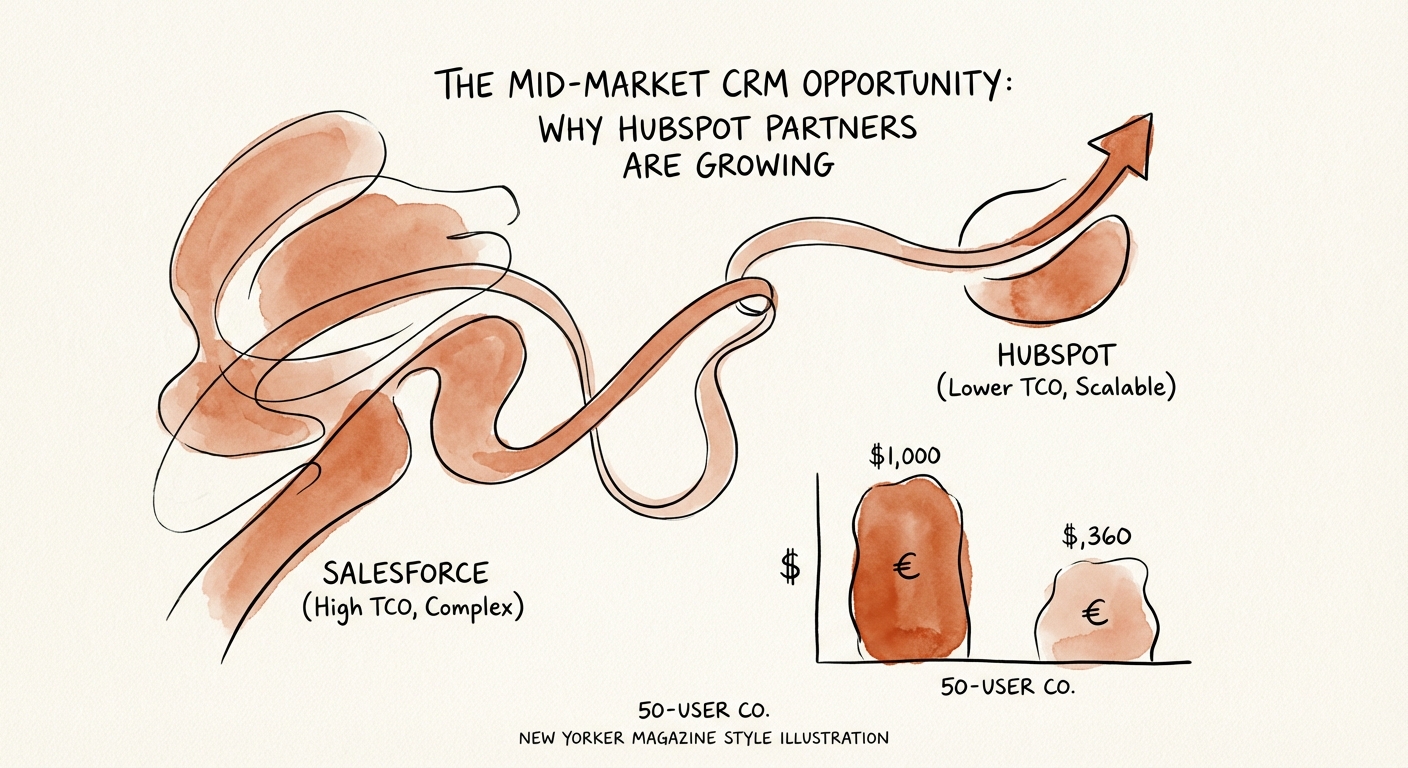

The Migration Tide: Escaping the "Admin Tax"

For the last decade, the phrase "nobody gets fired for buying Salesforce" was the operational gospel of the mid-market. In 2026, that gospel has been rewritten: "Nobody gets fired for buying Salesforce, but they might lose support over the Total Cost of Ownership (TCO) that comes with it."

We are witnessing a massive migration tide. Mid-market companies ($50M-$500M revenue) are fleeing legacy enterprise CRMs not because of feature gaps, but because of complexity fatigue. They are tired of needing a $180k/year administrator to change a dropdown menu. They are tired of six-month implementation cycles that stall revenue.

The Economics of Migration

The numbers driving this shift are undeniable. Recent data from 2025 benchmarking studies reveals a stark contrast in the cost to deploy:

- Average Implementation Cost: Salesforce ($14,595) vs. HubSpot ($2,945).

- TCO Savings: Companies switching to HubSpot report an average 30-40% reduction in 3-year Total Cost of Ownership.

- Time-to-Value: HubSpot implementations average 4-8 weeks, compared to 4-6 months for comparable Salesforce deployments.

For private equity operating partners, this is not just IT savings; it is velocity. Every month spent implementing a CRM is a month of lost data, lost forecast accuracy, and lost revenue. The market has realized that "Enterprise Power" is worthless if it requires a PhD to operate. The new gold standard is adoption, and HubSpot is winning that war.

The market has realized that 'Enterprise Power' is worthless if it requires a PhD to operate. The new gold standard is adoption, and HubSpot is winning that war.

Revenue Architecture: From "Agency" to "RevOps Systems Integrator"

This migration tide has created a bifurcated market for service providers. On one side, you have the traditional "Inbound Marketing Agency." They sell content, SEO, and social media retainers. They trade at 4x-6x EBITDA because they are viewed as low-moat, high-churn service businesses.

On the other side, a new breed of partner has emerged: the RevOps Systems Integrator. These firms don't just "do marketing." They architect the entire revenue engine—sales pipelines, service ticketing, and data orchestration. They are capturing the implementation and migration budgets that used to go to global consultancies.

The Valuation Pivot

If you are a Founder running a HubSpot partner firm, your valuation depends entirely on how you position your revenue architecture:

- Marketing Revenue (Low Value): "We write blogs and manage ads." High churn, low switching costs.

- Technical Revenue (High Value): "We integrate ERPs, migrate data, and build custom API workflows." High switching costs, critical infrastructure.

The partners commanding premium valuations are those who have moved upstream. They are leveraging HubSpot's "Breeze Copilot" and AI agents to replace manual labor, increasing their own gross margins. They are selling outcome-based transformations, not hours. When you shift from selling "activities" to selling "infrastructure," you stop being a vendor and start being a strategic asset. This is the difference between a "lifestyle business" and a RevOps engine that PE firms fight to acquire.

The Valuation Gap: Why 12x is the New Benchmark

In 2025, the private equity market for mid-market buyouts saw entry multiples rise to 12.1x EBITDA. This surge is not evenly distributed. It is concentrating around "Platform" investments—companies that can serve as the foundation for a roll-up strategy.

HubSpot partners are currently the darling of this trend. Why? Because the ecosystem is fragmented, but the underlying software growth is robust (HubSpot projected ~$3B revenue in 2025 with expanding margins). PE firms are aggressively consolidating regional "Elite" and "Diamond" partners to build national challengers to the Big 4 consultancies.

The Due Diligence Checklist for Partners

If you are looking to exit, or if you are a PE sponsor looking to buy, here is what separates the 12x asset from the 4x commodity:

- Revenue Mix: Is >40% of revenue derived from complex integrations, migrations, and technical consulting?

- Net Revenue Retention (NRR): Is NRR >110%? (implying you are expanding accounts, not just replacing churn).

- Specialization: Do you have a "right to win" in a specific vertical (e.g., FinTech, Manufacturing) or are you a generalist?

The window is open. The "Teal" ecosystem is maturing, and the smart money is moving away from "creative services" toward "technical engineering." If you speak fluent EBITDA and fluent API, you are sitting on a gold mine.