The practical answer

- Short answer

- The day a SaaS deal closes, your principal engineers go fully liquid and their reason to stay drops to zero. Here is the tier-by-tier equity refresh math that holds them.

- Best fit

- Industry: B2B SaaS / Technology M&A. Function: Human Resources / Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 43% of critical technical talent is lost within 14 months post-close due to mathematically flawed equity refreshers.

The most dangerous moment in a software deal is the day it closes

Picture the wire clearing on a $120M DevOps platform. The founders are celebrating. The sponsor's deal team is already onto the next target. And somewhere in a Slack channel the diligence team never read, three principal engineers — the ones who can still explain why the billing service was built the way it was — just watched their unvested options accelerate, cash out, and disappear. As of that morning, the smartest people in the codebase have exactly zero financial reason to open their laptops tomorrow.

This is not a culture problem. It is a cap table that was designed for the wrong people. Buyers will build a forty-tab LBO model that prices the cost of debt to the basis point, then treat the retention of the actual intellectual property — the people — as a line item HR will "handle post-close." I have sat in the room when that bill comes due. On that DevOps integration, the sponsor tried to hold the core team with a flat 1% pool peanut-buttered across forty people. I told them the math wouldn't hold. Inside 90 days a Series C competitor had cherry-picked the two architects who held the system in their heads, $30M of enterprise value walked out with them, and the roadmap stalled for three quarters. Rebuilding that tier cost the sponsor roughly triple the original equity ask — paid out in panicked cash sign-on bonuses and slipped release dates.

The mechanism is brutally simple. Buyers force founders and the C-suite to roll 20-30% of their proceeds into the new entity, because alignment matters at the top. That requirement almost never reaches the individual engineers who wrote the code. So the ICs hit acceleration, take the check, and find their unvested upside has evaporated — what I call the acceleration trap, and what I've written about in detail in how option acceleration provisions interact with exit readiness. Harvard Business Review's research on the M&A talent retention dilemma is blunt about the cost: acquirers that don't issue substantial refreshers immediately watch productivity crater in the first hundred days. You cannot patch that with a 0.05% grant that demands another five years of grinding before it means anything.

When you buy a software company, you are not buying the repo. You are renting the four or five minds that can still explain it under pressure — and on close day, their lease is up.

Why the standard MIP guarantees a brain drain in tech deals

Here is the legacy assumption that breaks the moment you apply it to software. Classic buyout math reserves a 10-15% Management Incentive Plan, and it points that pool almost entirely at titles: CEO, CFO, CRO, VP Engineering. That works when you're buying a distribution business where value lives in contracts and a depreciating asset base. It is malpractice when you're buying a codebase, because in software the IP is not in the VP's head — it's in the head of the staff engineer two levels below her who actually owns the service that generates 40% of revenue.

The fix is to stop allocating by org chart and start allocating by who can stall the product. Carta's private markets data points to a post-close pool of roughly 15-20% of fully diluted shares for tech integrations — but the number that matters is the carve-out inside it: a ring-fenced 5-7% reserved exclusively for top-decile technical talent below the VP line. You do not spread that across the whole engineering org and call it fair. You identify the handful of people whose departure would set the roadmap back two quarters, and you make their grants large enough to change their life math.

The unpriced liability sitting in your diligence file

Run the test on your own target. Say it has $20M in ARR, and when you map the codebase you find that 60% of the critical architecture is genuinely understood by three senior developers — none of whom hold meaningful unvested equity once the deal closes. That is not a staffing footnote. That is a concentrated, unpriced liability against your entire thesis, and pricing it belongs in diligence, not the first board meeting. Treating it seriously is exactly why evaluating technical talent retention risk before signing has become standard practice for the sharper funds. Bain & Company's M&A research quantifies the drag: failing to aggressively refresh technical talent translates into a direct hit on the integration synergies you underwrote. You can model that loss, or you can fund the grants that prevent it. One of those is cheaper.

What an engineer refresh grant actually looks like

First, kill the instinct to use cash earnouts on engineers. Earnouts get tied to company-level EBITDA or revenue targets — outcomes a backend engineer cannot move no matter how good their week was. The moment an engineer sees their retention hooked to a 30% revenue growth number they had no hand in setting, they mentally mark it to zero and start taking recruiter calls. Use equity they can feel: time-based RSUs or performance-tied phantom equity on a schedule fast enough to matter. The classic four-year vest with a one-year cliff is built for hiring, not for holding someone through the chaos of an integration. For a refresh, the market has moved to a three-year vest with quarterly or monthly vesting after a short six-month cliff — close enough that staying always beats leaving.

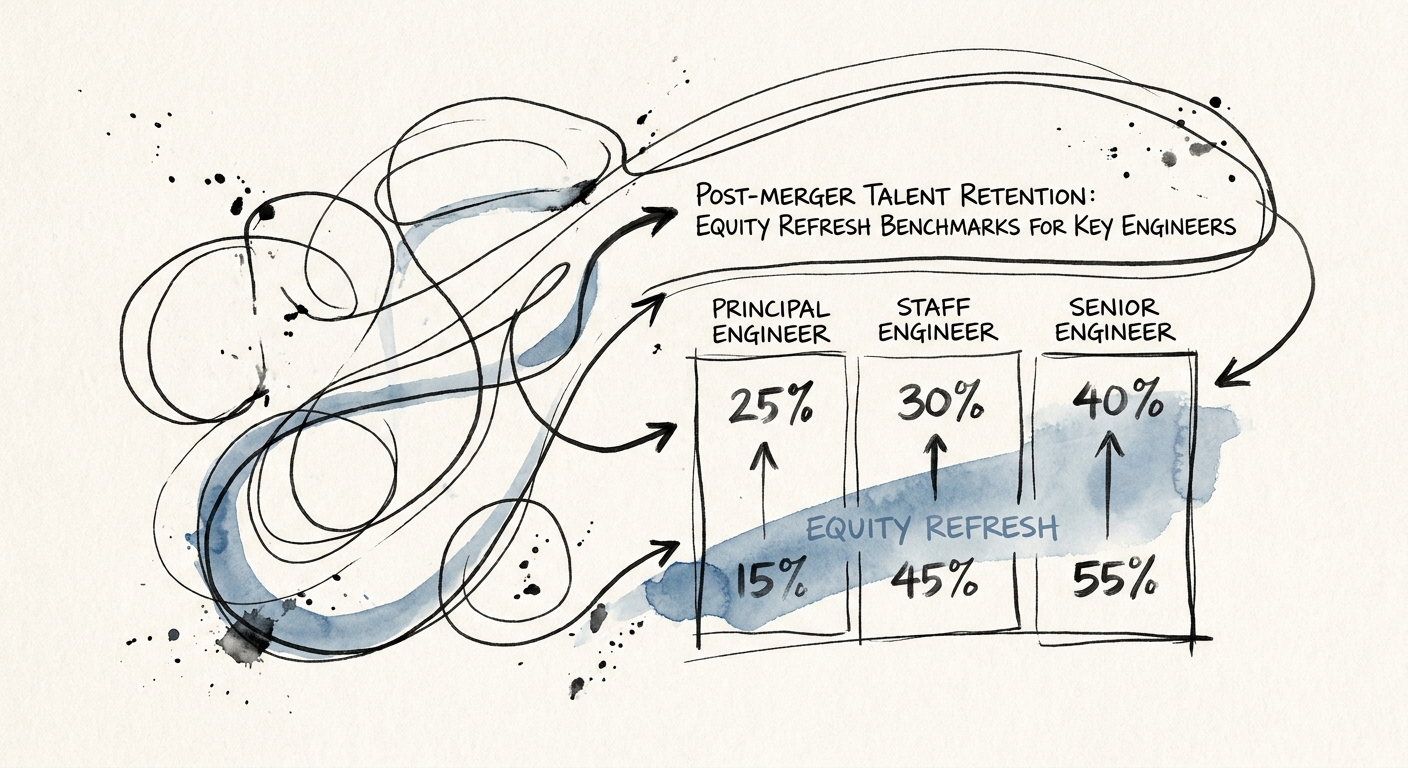

The refresh matrix for a $50M-$250M EV software buyout

These are the ranges, drawn from how these deals actually get papered in the middle market. The point is the relative spread, not false precision — calibrate to your specific cap table and flight-risk map:

Principal / Distinguished Engineers — 0.35% to 0.60% of post-money fully diluted. These are the people who can rewrite a core microservice over a long weekend and have it be better. One of them walking is a guaranteed product stall, so this is where you over-index, not where you negotiate.

Staff / Lead Engineers — 0.15% to 0.30%. They run the day-to-day velocity of the sprint teams and they're the ones who answer the 11pm page. Lose enough of them and the principals start spending their time firefighting instead of building.

Senior Engineers, top quartile only — 0.05% to 0.10%. Reserve this strictly for the seniors flagged as flight risks who carry deep, undocumented domain knowledge. Not a participation trophy for everyone with the title.

If those numbers make you flinch, do the replacement math instead. Losing a principal engineer means six months to recruit, three to onboard, and another six before they're at full productivity on an unfamiliar codebase — a fifteen-month velocity tax, and that's the optimistic case where the surrounding team doesn't follow them out the door. The attrition cliff that hits after acquisition is a documented deal-killer, not a soft risk. So treat these grants for what they are: a calculated capital expenditure that protects the exact thesis you wrote the check on. Identify the four or five people whose absence would hurt most, size the grants before the wire goes out — not after the resignation does — and protect the multiple you're underwriting for.