The practical answer

- Short answer

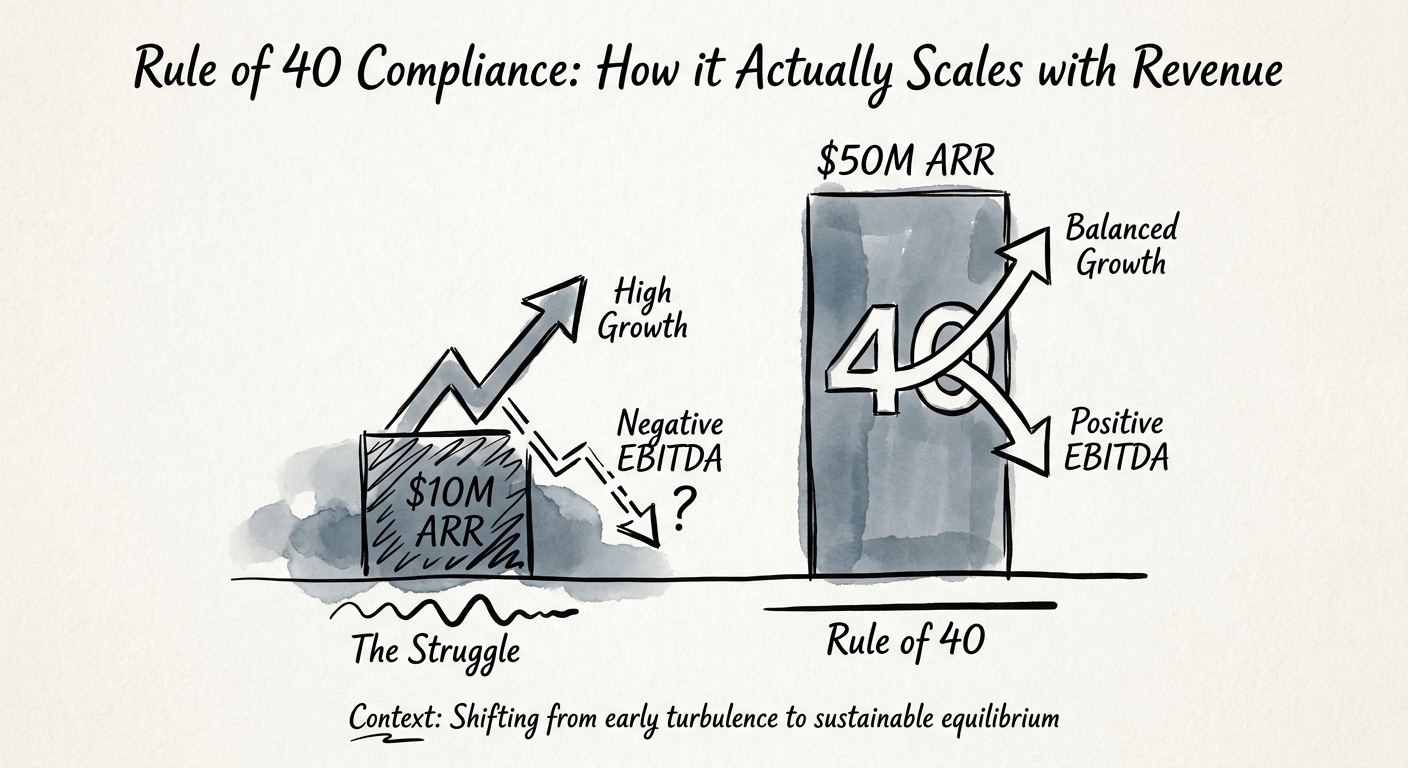

- At $10M-$50M ARR, a tidy 40 score can mean you starved growth. Here's how the Rule of 40 actually changes by revenue tranche before a SaaS exit.

- Best fit

- Industry: Technology. Function: Finance & Strategy

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 78% Minimum gross margin required to sustainably maintain Rule of 40 at scale.

A 41 that cost you the deal

Picture a founder-CEO at $14 million ARR who has done everything the board asked. Growth is a respectable 18%, EBITDA margin is 23%, and the composite Rule of 40 score lands at a clean 41. The deck looks bankable. Then the growth-equity term sheet comes back lighter than expected, and the partner says the quiet part out loud: "Your growth doesn't justify a software multiple, and your margin doesn't justify a buyout multiple. You're stuck in the middle." That founder didn't fail the Rule of 40. They optimized for it at exactly the revenue stage where the metric lies to you.

Here is the part most decks miss. Below roughly $50 million in revenue, a point of top-line growth is not worth a point of margin. McKinsey's Rule of 40 diagnostic for software companies finds growth contributes up to roughly twice as much to the valuation multiple as profitability for companies under $50 million. So a 40 assembled from 18% growth and 22% margin is structurally cheaper than a 40 assembled from 30% growth and 10% margin, even though the headline number is identical. When you throttle acquisition to manufacture margin at $14 million ARR, you are trading the expensive half of the score for the cheap half and telling the room your addressable market has tapped out.

It's worth remembering the metric's origin. The Rule of 40 was a public-market heuristic for mature, large-cap software, not a governor for a company still building its first repeatable revenue engine. At the bottom of the mid-market it simply does not hold. The KeyBanc Capital Markets Annual SaaS Survey consistently shows the median private SaaS company well under the 40 line at smaller revenue scale, because the fixed cost of standing up a predictable go-to-market motion eats margin first and pays it back later. Forcing the number early means cutting the engineering hire, delaying the second sales pod, or trimming the team that renews your base. Each one shows up later as a longer path to a liquidity event.

A 40 score built by cutting sales is a different animal than a 40 built on 80-point gross margins. Diligence tells them apart in an afternoon, and only one of them pays.

The score means three different things between $10M and $50M

Treat the Rule of 40 as one benchmark across the $10M-$50M band and you will misread your own company. The composite is the same arithmetic at every stage; what a sophisticated buyer reads into it changes completely.

Sub-$10M ARR. Profitability is noise here. A buyer wants to see whether the motion works at all: net revenue retention holding above 100%, a payback period that isn't widening, and a logo count that proves the pitch lands outside the founder's network. A negative-20% EBITDA line paired with 40%+ growth is a healthier signal than a tidy breakeven, because breakeven this early usually means you stopped spending before you proved the channel.

$10M-$30M ARR. This is the transition zone, and it's where the most expensive mistakes happen. Growth should still lead — call it 30%-plus — while EBITDA trends deliberately toward breakeven rather than lunging at it. The instinct to "look profitable" before a raise is strongest here and almost always premature. Bain & Company's Rule of 40 software analysis notes that only a minority of software companies sustain true Rule of 40 performance for more than three years running, which is exactly why diligence indexes on durability over any single quarter.

$30M-$50M ARR. Now the metric earns its reputation. A balanced 25% growth and 15% EBITDA is the profile that supports a premium multiple, because at this scale operating leverage should be showing up on its own. Buyers stop subsidizing inefficient growth and start pricing whether each new dollar of revenue costs less to win than the last.

The trap across all three is the quarter-before-exit margin spike. Say a $32 million logistics-software business halts territory expansion and freezes marketing two quarters out; the composite jumps to 43, but the SaaS Quick Ratio craters as new-bookings momentum stalls against churn. A buyer reads the gross-add collapse on the first diligence call. This is the same dynamic underneath the weighted view of the Rule of 40: growth bought with an escalating customer acquisition cost gets discounted, not rewarded, no matter what the composite says.

The 40 that survives diligence is built one layer down

A defensible Rule of 40 is not engineered in the EBITDA line. It is engineered two layers below it, in gross margin and cost of acquisition — and that work doesn't reverse the week after close. Gartner's SaaS gross margin and profitability benchmarks point to a common trait among companies that hold true compliance: gross margins comfortably north of the high-70s. That single line is doing more for the multiple than any expense cut a CFO can find.

Run the test on your own P&L. If gross margin sits around 65% because every implementation leans on a professional-services bench that loses money on each deployment, no amount of sales efficiency saves your score when you reach $50 million ARR — the structural drag scales right along with the revenue. The fix is unglamorous and slow: automate deployment, standardize configuration so it stops being a custom project, and move delivery toward IP rather than headcount. You cannot cut your way to a premium multiple, because the thing being priced is the slope of your unit economics, not this quarter's expense ratio.

The companion lever is knowing what acquisition actually costs you. Strip out the marketing attribution noise, load the fully burdened sales cost, and compute your true CAC payback period. Past 18 months in the mid-market, the growth motion is too expensive to ever fund its own profitability, and that shows up in valuation long before it shows up in the bank account. None of this is hidden from the buyer's side, either. EY's analysis on redefining the Rule of 40 describes how quality-of-earnings reviewers look straight past the headline and apply discounts when margin was borrowed from underinvestment in technical debt, security, or customer success. So pick one number this week: pull the true CAC payback, and the loaded gross margin behind your largest customer segment. Whichever is worse is the one quietly setting your ceiling — and it's the one to fix while you still have runway to fix it.