The practical answer

- Short answer

- SAP services firms exit at 1.5x revenue. BTP-IP partners trade at 5-8x. Here is how to turn the custom code you already wrote into packaged SaaS.

- Best fit

- Industry: B2B Tech Services. Function: Product & Strategy

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 8x Typical Revenue Multiple for BTP-based IP revenue, compared to 1.5x for implementation services.

The Z-table you have built nine times

Open your firm's last ten S/4HANA engagements and look at the custom development log. Somewhere in there is the same object, rebuilt from scratch for every client: a freight-cost allocation routine, a batch-recall trace, a consignment-billing reconciliation. Different customer, same gap, same two senior consultants burning the same six weeks. You billed for it nine times. You own it zero times.

That is the quiet tragedy of the SAP services model. You are extraordinarily good at finding the place where standard S/4HANA stops and the customer's real process begins — and then you give that knowledge away one hourly invoice at a time. When you sell the firm, a buyer looks at headcount-bound EBITDA and offers you something in the neighborhood of 1.2x to 1.5x revenue. That is the valuation gravity every body-shop lives under.

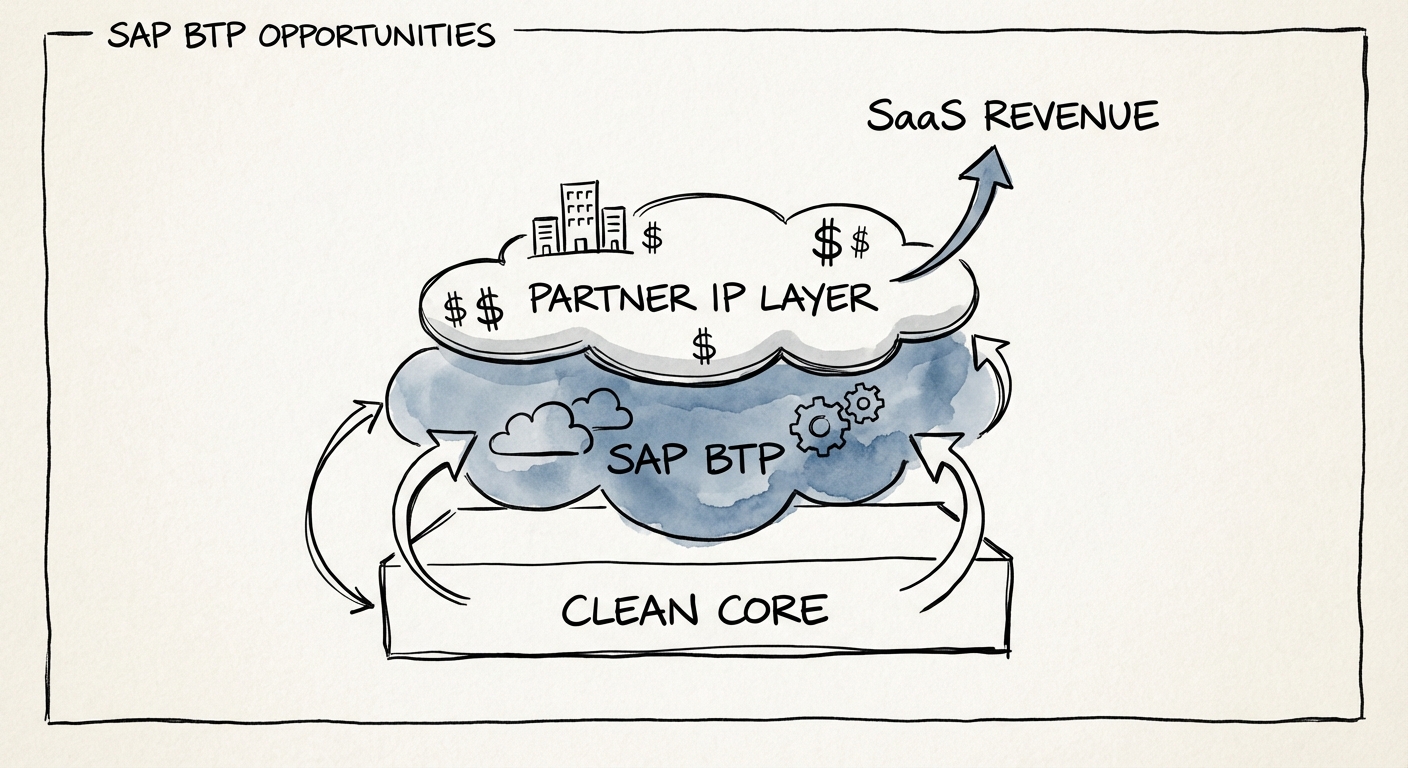

The partners who took that same custom object, rebuilt it once as a clean extension on the SAP Business Technology Platform, and listed it on the SAP Store are not in that conversation. They are being valued on recurring license revenue at 5x to 8x. The engineering work was nearly identical. The business model was not.

Why BTP changed the math, not just the menu

For years, "productizing your SAP IP" meant on-stack ABAP modifications that broke at every upgrade — so nobody productized anything. BTP severed that dependency. Your extension now runs beside the ERP on SAP's own runtime, with its own lifecycle, its own subscription billing through the Store, and its own upgrade path. The thing that used to be a maintenance liability is now a sellable, recurring-revenue asset. That is the structural change worth understanding before you write another custom object you will never own.

Every SAP partner has a folder of custom Z-objects they have rebuilt for nine clients. That folder is not technical debt. It is your unshipped product backlog, and Clean Core just handed you the deadline to ship it.

The multiplier is real, and it is not subtle

SAP commissioned IDC to measure what partners actually earn for every dollar of SAP software in play, and the spread by business model is wide enough to drive a roadmap through. Service-led partners pull roughly $5.00 to $8.81 in their own revenue for each $1 of SAP license. IP-led partners — the ones with packaged BTP solutions — pull closer to $10.00 (IDC: SAP Partner Opportunity & Ecosystem Multiplier). IDC's separate work on BTP itself documents why customers pay for these extensions in the first place — measurable cycle-time and integration value sitting on top of the core (CIO/IDC: Business Value of SAP BTP).

But the multiplier is the smaller story. The bigger one is what kind of revenue you create. A subscription to your batch-recall extension does not walk out the door at 5 PM, does not need to be re-sold every quarter, and does not depend on you keeping a senior architect from quitting. It compounds. You build the freight-allocation engine once and bill it across forty mid-market manufacturers with near-zero marginal cost.

How a buyer pulls your P&L apart

When an acquirer evaluates a hybrid SAP firm, they do not value it as one company. They split it. The services line gets valued on EBITDA, where every add-back is fought over in diligence. The BTP-subscription line gets valued on recurring revenue, where the questions are about net retention and ARR growth instead. Aventis Advisors' multiples data shows just how far apart those two worlds sit (Aventis Advisors: IT Services vs. SaaS Valuation Multiples).

Run the arithmetic on a hypothetical $20M SAP partner. As pure services at, say, 1.5x, that is a $30M outcome. Now move even a quarter of that revenue into BTP subscriptions valued at 6x: the $5M IP line alone is worth $30M, and the remaining $15M of services adds another ~$22M. Same company, roughly the same headcount, more than 1.7x the enterprise value — because you changed which spreadsheet your revenue lands in, not how hard your team works.

What to do Monday: mine the gaps, not the demos

You are not going to out-engineer SAP, and you should never try to rebuild a module — that path ends in a graveyard of half-built mini-ERPs. The money is in the seams S/4HANA leaves open on purpose: the industry-specific, regulation-specific edges SAP is too horizontal to perfect. Three concrete moves:

1. Run a development-log audit, not a brainstorm

Skip the strategy offsite. Instead, pull the custom-object inventory from your last dozen projects and rank by how many times you rebuilt the same thing. The object you have shipped five-plus times for the same vertical is not a coincidence — it is product-market fit you discovered by accident. That ranked list is your BTP roadmap, already validated by paying customers.

2. Let Clean Core write your sales deck

SAP's Clean Core push — keep the ERP standard, move every customization to BTP — is the most useful sales catalyst a partner has been handed in a decade. Every CIO now has a board-level mandate to get custom code off the core to escape the next upgrade trap. When your extension lives outside the digital core on BTP by design, you are not selling a feature; you are selling an architecture that survives the next S/4HANA upgrade. You are on the same side of the table as the buyer's mandate.

3. Niche until it sounds absurd, then go narrower

A "freight cost allocator" is a commodity that a bigger ISV will undercut by Tuesday. A "GxP-compliant batch-recall trace for FDA-regulated medical-device contract manufacturers" is a near-monopoly in a market too small for SAP or the megavendors to chase. The narrower the vertical, the more pricing power and the stickier the renewal. Pick the regulated, painful corner you already understand from delivery work — and own it.

The land grab on the SAP Store is happening now. The partners who list their first vertical extension this year capture a renewal stream that compounds for the next decade. The ones who wait will still be excellent at SAP delivery — and still defending their day rate in a procurement portal against three firms quoting the same scope.