The practical answer

- Short answer

- Technical debt isn't just an engineering problem; it's a 30% valuation haircut. Learn how aging codebases depress M&A multiples and how to quantify the 'Innovation Tax' in due diligence.

- Best fit

- Industry: Private Equity / Software M&A. Function: Investment Committee

- Operating path

- Technical Debt → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 33% Of developer time wasted on technical debt maintenance (Stripe Developer Coefficient)

The Hidden Balance Sheet Liability

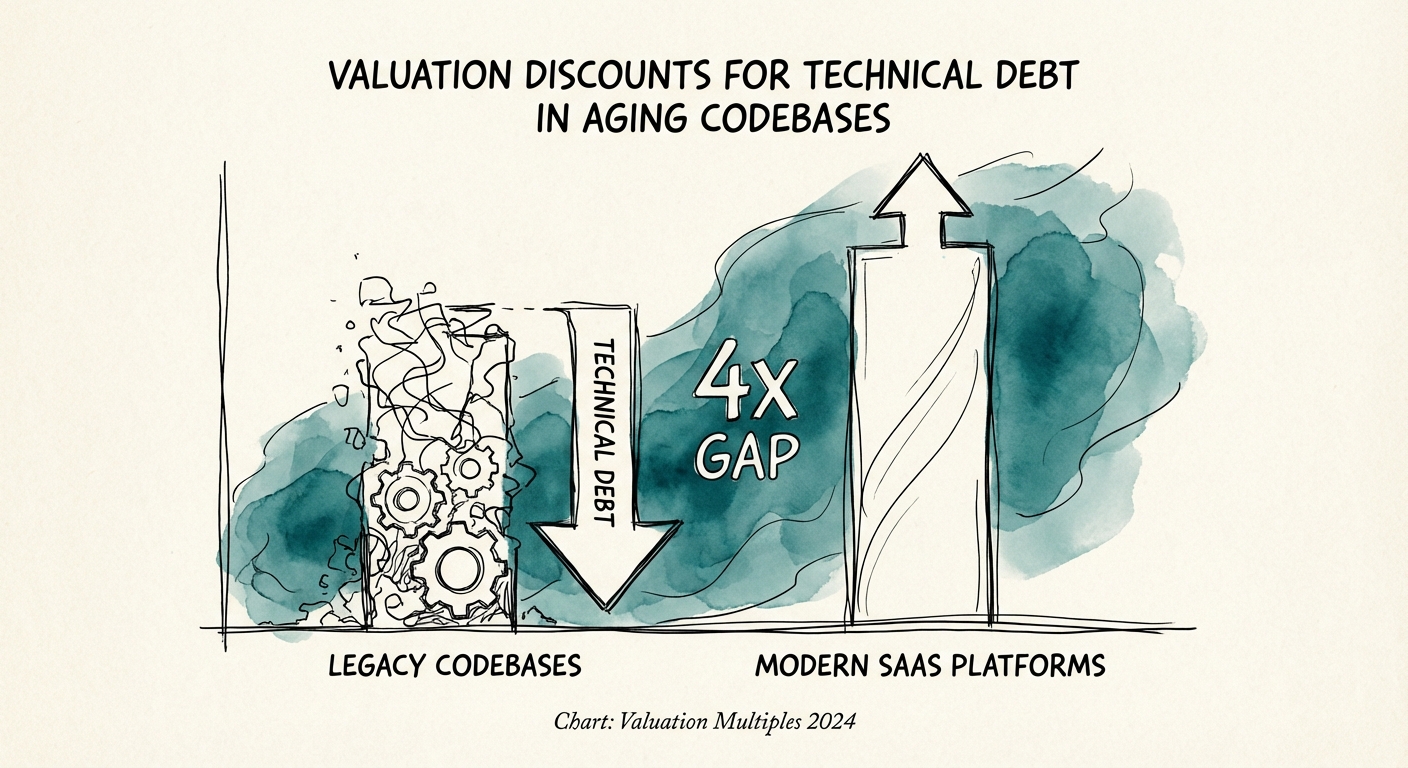

In the polished slide decks of a Management Presentation, “proprietary technology” is always an asset. But in the trenches of post-close integration, that same technology often reveals itself as a massive, off-balance-sheet liability. We call this the Legacy Code Discount, and in the 2025 M&A market, it is effectively repricing deals by up to 30%.

Technical debt behaves exactly like financial debt, yet it rarely appears on the CIM (Confidential Information Memorandum). It consists of two components:

- The Principal: The raw cost to refactor or rewrite the aging codebase into a modern, supportable state.

- The Interest: The daily “tax” paid in reduced engineering velocity, higher defect rates, and the inability to ship new features.

For a Private Equity sponsor, the “Interest” is the killer. Research from Stripe’s Developer Coefficient report indicates that developers spend approximately 33% of their time dealing with technical debt and bad code. That is one-third of your engineering payroll—an Operating Expense (OpEx) that produces zero enterprise value. When you acquire a target with an aging codebase (e.g., legacy .NET, older Java, or monolith PHP), you aren't just buying software; you are inheriting a mortgage where the interest payments are eating your R&D budget alive.

This is why Operating Partners are now mandating “Code Age” audits alongside Quality of Earnings (QofE). If the target’s technology stack is nearing End-of-Life (EOL), the cost of that “Principal” payment (the rewrite) must be deducted from the purchase price, just as you would treat a working capital adjustment.

Tech debt is the silent source of deal-value erosion. If 40% of your acquired R&D budget is spent fixing yesterday's code, you aren't buying a growth asset—you're buying a remediation project.

The 'Innovation Tax' Calculator

The most direct impact of technical debt is on your valuation multiple. Tech valuations are driven by growth and margins. Aging codebases attack both. We use a concept called the Innovation Tax to quantify this impact during diligence.

Consider a target company with $10M in EBITDA and a $5M R&D budget. On paper, they are spending 50% of EBITDA on product innovation. However, if their technical debt load requires 60% of engineering cycles for “maintenance” (keeping the lights on, fixing bugs, patching security holes), their effective innovation spend is only $2M. The other $3M is the Innovation Tax.

The Multiplier Effect

When you apply a 12x multiple to that business, you are paying for future growth. But if 60% of the engineering team is stuck in “digital concrete,” that growth is structurally impossible. This is why we see “legacy” assets trading at 7-8x EBITDA while their modernized peers command 12-14x. The market is pricing in the cost of the fix.

Benchmarks from Gartner suggest that by 2025, companies will spend 40% of their IT budgets simply maintaining technical debt. In M&A terms, this means your “Value Creation Plan” starts with a handicap. If you don’t factor this into the purchase price, you are paying a premium multiple for a discounted asset.

Smart acquirers are now using technical debt quantification frameworks to negotiate price adjustments. If a code audit reveals $2M in necessary remediation to secure the platform, that $2M is treated as “Deficit CAPEX”—a direct deduction from Enterprise Value.

The Due Diligence Diagnostic (The 'Code Age' Audit)

How do you spot the Legacy Code Discount before you sign the LOI? You don’t need to read code to read the signs. Ask these three questions during your technical diligence sessions to uncover the hidden liability:

1. The Framework Age Test

Ask for a list of all core languages and frameworks with version numbers. If the primary application is built on a framework that is no longer supported (e.g., .NET Framework 4.5, Python 2.7, AngularJS), you are buying a security risk, not an asset. This is the Classic .NET Trap. The cost to migrate is not incremental; it is exponential.

2. The 'Key Person Dependency' of Legacy Knowledge

In aging codebases, documentation usually rots first. The logic of the system lives in the heads of one or two senior engineers who have been there for a decade. If your diligence reveals that only “Steve” knows how the billing engine works, you have a Key Person Dependency of 1. This is a massive key-person risk that justifies a valuation discount or a significant holdback.

3. The Maintenance-to-Innovation Ratio

Ask for the percentage of engineering tickets tagged as “Feature” vs. “ Bug/Maintenance” over the last 12 months. If “Maintenance” exceeds 40%, the codebase is brittle. You aren't buying a growth platform; you are buying a maintenance project. This ratio directly correlates to the Technical Debt Percentage benchmarks we see across portfolios.