The practical answer

- Short answer

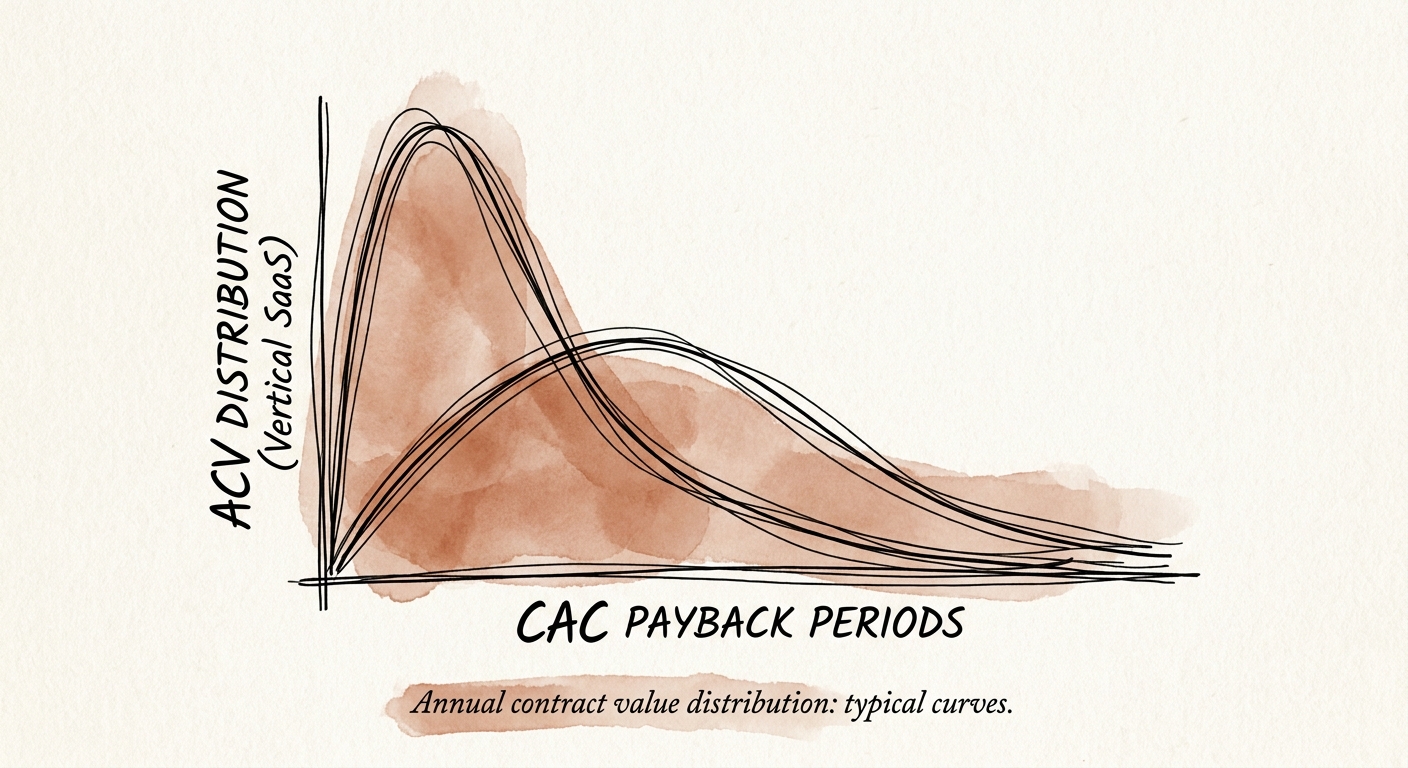

- A tidy bell-curve ACV around $26K feels like product-market fit. In vertical SaaS it's usually a margin sinkhole. Here's how to read the curve and fix it.

- Best fit

- Industry: B2B SaaS. Function: Revenue Operations

- Operating path

- Unit Economics → Commercial Performance → Transaction Advisory Services

- Key metric

- 14-18 Months for CAC payback in the $15K-$100K mid-market valley.

The slide that should have scared the founder

A prop-tech CEO once flipped to his ACV chart like it was a trophy: a clean bell, roughly 80% of logos packed between $25,000 and $50,000, almost nothing on the tails. He read it as discipline. Tight clustering, one repeatable motion, no weird outliers. I read it as a building full of deals that each cost like an enterprise deal to win and keep, while paying like a mid-market deal. That gap is where his cash was disappearing, one renewal at a time.

Here is the part that makes vertical SaaS specifically dangerous. Your buyers all live in one industry, so they talk to each other, share the same procurement playbook, and demand the same custom redlines, the same security review, the same niche integration into whatever system-of-record their vertical runs on. A $30,000 contract in that world triggers nearly the identical sales multi-threading and technical validation as a $130,000 contract. The dollars differ by 4x. The cost to land them barely differs at all.

And the median is no escape hatch. The 2026 SaaS Benchmarks Report from Prospeo puts the median ACV for private vertical SaaS at $26,265 — close enough to that prop-tech fat middle to matter. Anchor your whole go-to-market to roughly that number and you've designed a company that does high-touch onboarding, named account management, and bespoke implementations for a price that can't carry any of it. The bell curve isn't a sign of fit. It's a bet that every revenue dollar costs the same to acquire and serve, and in a vertical market that bet is simply wrong.

A perfect bell curve in your contract values isn't fit. It's a building full of $30K deals that each cost a $130K deal to close and keep alive.

Why the middle is a trap and the edges aren't

The capital-efficient vertical SaaS businesses I see don't have a bell. They have a barbell — a dense cluster of low-touch, self-serve accounts at one end, a smaller set of six-figure enterprise accounts at the other, and a deliberate, almost uncomfortable emptiness in between. It looks reckless on a chart. It's the opposite. It's the only shape where each customer is matched to a cost structure that can actually carry it.

The payback math is what forces the shape. Figures from the ScaleXP 2025 SaaS Benchmarks show mid-market deals in the $15,000 to $100,000 band running 14 to 18 months to recover CAC. That's the valley. Below it, self-serve SMB motions recover in roughly 8 to 12 months because almost no human touches the deal. Above it, a 24-month enterprise payback is fine, because net revenue retention north of 130% means the account keeps growing long after it's paid you back. The middle gets none of those mechanics. It carries enterprise sales cost without enterprise expansion, and SMB price without SMB efficiency.

So when you staff for the $26K median, you build two organizations that are both wrong on purpose: an inside sales team too thin to win real enterprise, and a customer success team too expensive to ever serve a $5K logo profitably. The fix isn't harder negotiation. It's gating value so cleanly that a true enterprise buyer can't get what they need from the cheap tier, and a self-serve buyer never has to talk to a human. Consumption and usage models are one lever for nudging accounts up the curve over time — I broke that mechanic down in The Consumption Premium — but the first move is admitting the middle has to thin out, not grow.

How to thin the middle without torching revenue

You don't migrate a bell into a barbell by optimizing the existing motion. You break it on purpose, in two directions at once. Pull the top up: take pricing off the website for anything above roughly $15,000 in annual value and require a discovery call to reach the premium tier. That single change removes the psychological ceiling that list pricing quietly stamps on your largest deals. OpenView's 2025 SaaS Benchmarks tie value-based pricing to about 25% higher net revenue expansion over cost-plus in the first three years — and you only capture that by gating the things enterprise buyers actually pay for: advanced integrations, SSO, custom reporting, premium SLAs. Done right, you find your top decile was prepared to pay more than you were charging them.

Then push the bottom down to zero-touch. If deploying a $5,000 ACV contract requires an implementation specialist or a technical account manager, you don't have a scalable software company — you have an IT consulting firm wearing a subscription model. The discipline test is blunt: every dollar of recurring revenue should map to a delivery cost that can carry it. Build a genuinely self-serve onboarding tier for the low end, or stop selling into the low end in its current shape. Pick one.

For most vertical SaaS founders this is a 12-to-18-month migration, not a relaunch, and it tends to run quieter than expected because the deals you cut were the ones bleeding you anyway. One concrete move for Monday: pull your last 50 closed contracts, plot ACV against fully loaded cost-to-acquire-and-serve, and circle every logo sitting in the $15K to $50K band with enterprise-grade delivery cost. That circle is your fat middle, in dollars. Customer concentration risk runs alongside this work, since thinning the middle reshapes who your largest accounts are — I covered how that flows into valuation in B2B SaaS Customer Concentration Risk in 2026. Thin the middle, match every cohort to a cost structure that fits it, and you hand a buyer the one thing they reward most: an EBITDA profile they can underwrite without flinching.