The practical answer

- Short answer

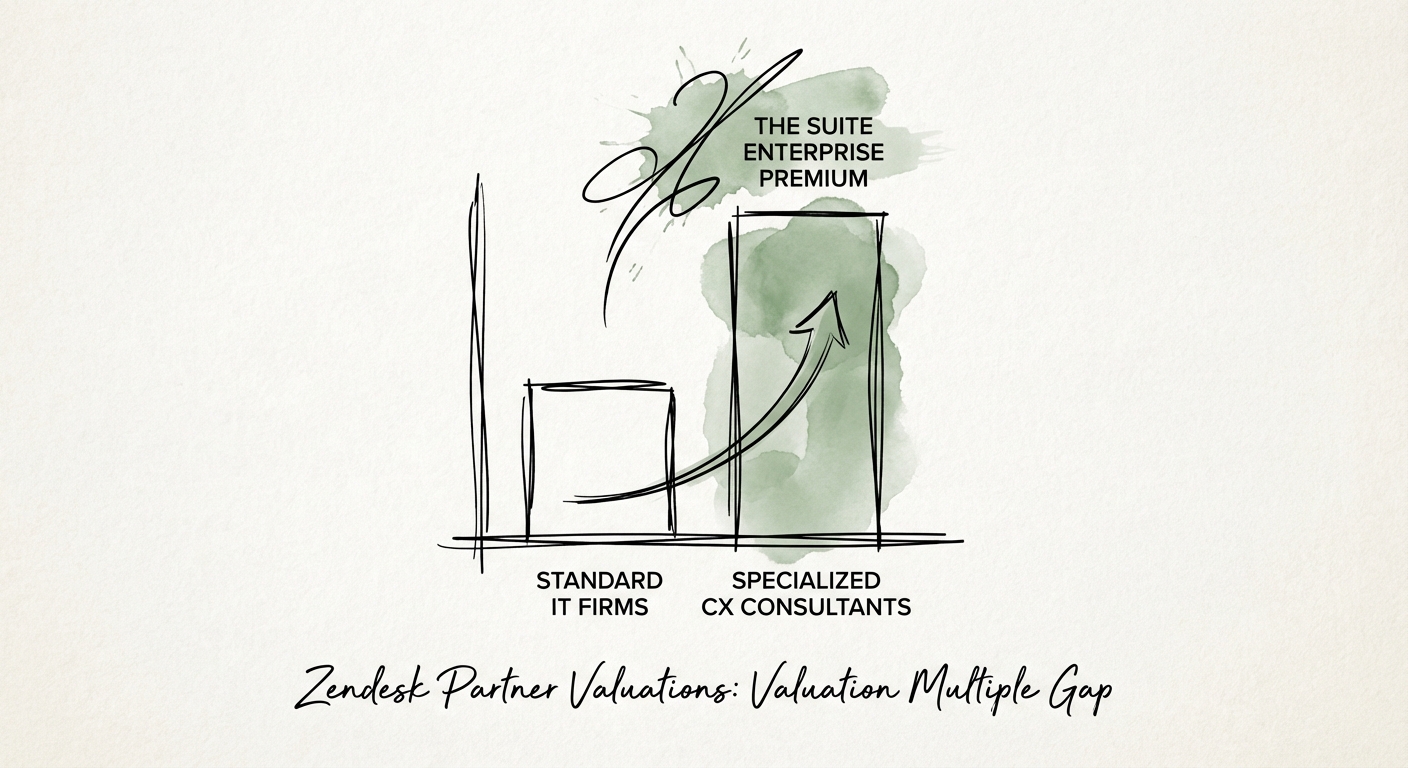

- Why Zendesk partners focusing on Suite Enterprise and Sunshine trade at 12x multiples while 'ticket deflection' shops stall at 6x.

- Best fit

- Industry: CX Technology. Function: Valuation

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Median EBITDA multiple for specialized IT consulting firms in 2025.

The Great Bifurcation: Ticket Deflectors vs. Resolution Architects

In the private equity ecosystem, not all Zendesk partners are created equal. We are witnessing a sharp bifurcation in the valuation landscape that mirrors the broader IT services market, but with a specific CX twist. On one side, we have the "Ticket Shops"—partners whose primary revenue stream comes from implementing standard Zendesk Support instances for SMBs. These firms are essentially digital plumbers; they connect the pipes, turn on the water, and walk away. Their revenue is transactional, their retention is tied to the software license rather than their service value, and they are currently trading at 5x to 7x EBITDA.

On the other side of the chasm are the "Resolution Architects." These are the partners who have embraced the upper bounds of the Zendesk Suite Enterprise SKU. They aren't just setting up email ticketing; they are deploying omnichannel messaging, configuring complex routing via Zendesk Sunshine, and, most importantly, implementing the new wave of Zendesk AI agents. Because they embed themselves into the client's revenue operations and customer retention workflows, they command significantly higher stickiness. In 2025, we are seeing these specialized firms trade at 10x to 14x EBITDA.

For private equity sponsors, the distinction is critical. A "Gold" or "Premier" badge is no longer a proxy for value. The real diligence question is: Is this firm implementing a help desk, or are they engineering an automated customer resolution platform? One is a commodity; the other is a strategic asset. If your portfolio company is still focused on "ticket deflection" rather than "autonomous resolution," you are leaving approximately 50% of your potential exit value on the table.

A 'Gold' badge is no longer a proxy for value. The real diligence question is: Is this firm implementing a help desk, or are they engineering an automated resolution platform?

The Technical Moat: Sunshine, AI, and the 'Agentic' Premium

The driver of this valuation gap is technical complexity. Basic Zendesk implementations are becoming increasingly commoditized, with Zendesk's own "out-of-the-box" AI capabilities making low-level configuration redundant. The premium valuation multiples are now reserved for partners who can navigate the Zendesk Sunshine platform and the emerging Agentic AI landscape. This is where the "Suite Enterprise Premium" becomes tangible on the P&L.

Consider the unit economics of an "Agentic" implementation. A partner that deploys autonomous AI agents using Zendesk's advanced APIs doesn't just bill for a one-time setup; they secure a high-margin, recurring managed service contract to tune, train, and optimize those models. According to recent market data, IT consulting firms with specialized intellectual property (IP) or deep platform expertise are trading at median multiples of 13.6x EBITDA, compared to generic implementation shops. In the Zendesk ecosystem, this "IP" often takes the form of custom apps built on the Zendesk Apps Framework (ZAF) or proprietary middleware connecting Zendesk to backend ERP systems.

Investors must scrutinize the Revenue Mix by Feature Set. If 80% of a partner's service revenue is derived from the core Support and Guide modules, they are vulnerable to vendor consolidation and AI automation. However, if 40%+ of revenue is tied to Sunshine Conversations, custom integrations, or AI agent orchestration, the firm has built a defensive moat. These integrations create high switching costs for the end customer, directly translating to the "quality of revenue" that buyers pay a premium for.

The Exit Readiness Playbook: Pivoting Revenue Quality

For Operating Partners and CEOs looking to maximize their exit multiple, the path forward requires a deliberate pivot in go-to-market strategy. You cannot simply "grow" your way to a 12x multiple by adding more SMB clients on the Team or Growth plans. You must migrate upmarket to the Suite Enterprise customer base, where the complexity of the problem demands a high-value solution. This involves three specific tactical shifts over a 12-18 month timeline.

First, audit your existing customer base for "Sunshine opportunities." Every client using Salesforce, NetSuite, or Shopify alongside Zendesk is a candidate for a high-margin integration project that transforms a simple help desk into a unified data platform. Second, re-package your managed services. Move away from "hours-for-dollars" support banks and towards "Resolution Optimization" retainers, where your firm is paid to continuously improve the client's automated resolution rates. This aligns your incentives with the client's outcomes and justifies a higher recurring price point.

Finally, look at your talent density. A 12x firm does not hire junior administrators; they hire solution architects and data engineers capable of building on AWS and interacting with Zendesk's open APIs. As we've seen in other ecosystems, there is a massive gap between 4x and 12x valuations that is driven entirely by the sophistication of the delivery team. Don't let your tier status fool you; in the M&A market, capability beats badging every time. Focus on Adjusted EBITDA quality, backed by deep technical moats, to unlock the true Suite Enterprise premium.