The practical answer

- Short answer

- A $10M ARR SaaS billing monthly carries ~$2.4M more working capital than billing annually. Here is the math, the churn cost, and the exact pivot playbook.

- Best fit

- Industry: B2B Software. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 2.5x Higher involuntary churn rate on monthly vs. annual contracts

The line item that decides whether you raise a bridge round

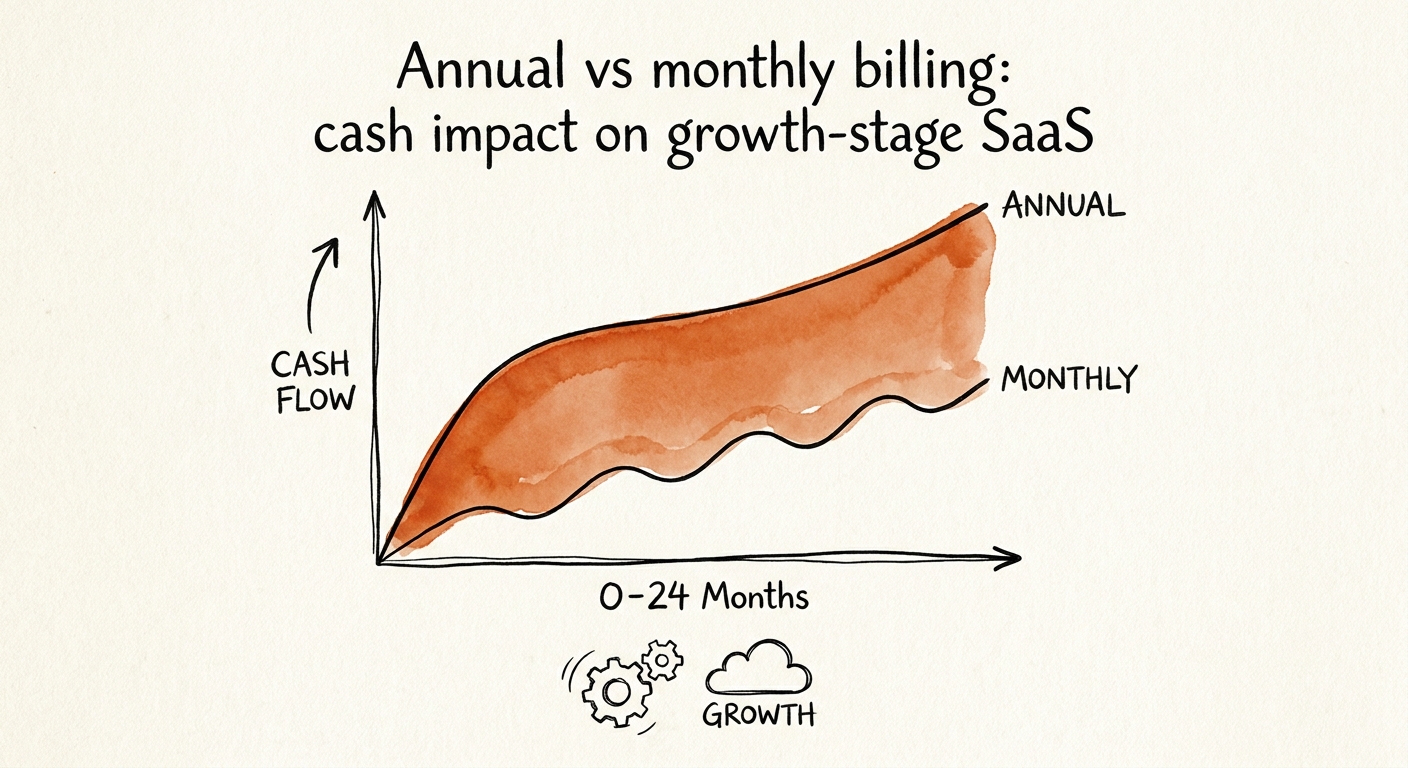

Picture the board deck of a $10M ARR Series B company that bills monthly. Net new bookings look healthy, NRR is fine, churn is "manageable." And yet the CFO is quietly modeling a bridge round, because cash keeps draining faster than the ARR chart suggests it should. The culprit is rarely in the deck. It is in the billing cadence.

Here is the math nobody puts on a slide. The median CAC payback period for mid-market software now sits around 15 to 18 months, per the KeyBanc Capital Markets SaaS Survey. Say you spend $15,000 to land a customer worth $12,000 a year. On monthly billing, that customer trickles back $1,000 a month — so you are underwater on them for roughly 15 months, financing their usage out of your own balance sheet the entire time. Multiply that trough across every new logo your sales team closes, and you have manufactured a structural cash deficit that scales with growth. The faster you sell, the deeper the hole.

Bill that exact same contract annually and $12,000 lands in your operating account on day one. Your cash payback collapses from 15 months to about 3. The product didn't change. The contract value didn't change. The only thing that changed is who fronts the working capital — and on monthly terms, the answer is you. At $10M ARR, the difference between the two models runs to roughly $2.4M in extra working capital tied up purely to subsidize the monthly cadence. That $2.4M is often the precise size of the bridge round a founder is about to take at a punishing valuation, to solve a problem the order form created.

When you bill a customer monthly while your CAC payback runs 15 months, you are not selling software — you are floating them an interest-free loan and calling it growth.

Why a Series B buyer prices monthly contracts as a liability

The cash trough is the operating problem. The valuation problem is sharper, and it surfaces the moment a diligence team opens your cohort data. A monthly contract is twelve renewal decisions a year. Each cycle exposes you to involuntary churn that has nothing to do with whether customers like the product: expired cards, hit credit limits, an AP clerk who left and never re-approved the charge. The Zuora Subscription Economy Index finds monthly-heavy subscription businesses run materially higher gross revenue churn than annual ones — enough to drag NRR down by points you can't claw back with upsell.

In a Quality of Earnings review, that churn signature is not a footnote — it is the cohort retention curve, and it directly compresses the multiple. If you want to see how the leak shows up in the unit economics before a buyer finds it, start with calculating true CAC payback with the hidden churn costs baked in.

Then there is the asset most founders treat as an accounting nuisance: deferred revenue. On the balance sheet it reads as a liability. Operationally, it is interest-free, non-dilutive capital your customers handed you in advance — a permanent float that funds burn. Scale annual-upfront ARR and you collect cash faster than you recognize GAAP revenue, which produces negative working capital. That is the most valuable shape a software business can take, and acquirers know it cold.

Run the comparison they run. Two companies, both at $20M ARR. Company A bills monthly; Company B bills annually. Company B is sitting on millions more in deployable cash and needs far less normalized working capital at close. So when the definitive agreement gets drafted, the monthly-billed business gets clipped — through a Net Working Capital target set high enough to make the buyer whole on the cash you never collected. You pay for the monthly cadence twice: once while operating it, and again at exit.

The annual pivot, without torching sales velocity

Founders resist the pivot because they assume enforcing annual terms will gut conversion and enrage the install base. That fear is real but the math behind it is usually wrong — the transition fails when it is announced as a policy and succeeds when it is engineered as three separate motions: net-new, exceptions, and renewals.

Start with the discount ceiling, because this is where margin quietly bleeds. Gartner's work on SaaS pricing shows discounts past ~20% erode lifetime value without buying you proportionally more conversions. Cap it at 16.6% — the "two months free" framing on a twelve-month term. You give up some recognized top line and you buy cash today, which compounds straight into your marketing engine instead of into a lender's interest payments.

For net-new mid-market and enterprise deals, pull the monthly option off the standard pricing page entirely. If a prospect insists on monthly, it becomes a priced exception carrying a 20% premium — you are simply quoting them the interest rate on the working capital you'd otherwise float on their behalf. Make the default annual and most buyers never ask.

For existing monthly customers, do not strong-arm a mid-term conversion. Use renewal as the wedge: announce a 12–15% increase on the monthly tier, then offer to freeze their current rate if they commit to annual upfront. Loss aversion does the selling. Most accounts take the lock-in, and you convert the riskiest part of your base into prepaid cash on the calendar you control. Run all three motions and your burn multiple improves without touching headcount or churn — and the bridge round you were modeling quietly disappears from the board deck. The single move worth making Monday: open your contract list, sort by monthly recurring revenue, and tag every account renewing in the next 90 days. That list is your conversion pipeline.