The practical answer

- Short answer

- A Series C SaaS firm gave away 20% to close by Friday and torched its margin. Here's the line between a discount that builds value and one that bleeds it.

- Best fit

- Industry: Technology. Function: Revenue Operations

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 2.4x Higher valuation multiples for companies that enforce rigid discount floors at exit.

The last Friday of the quarter is where SaaS margins go to die

Picture a $40M Series C SaaS company three days before the quarter closes. Two enterprise deals are stuck in procurement, the VP of Sales needs them to make the board number, and the fastest lever in the building is a 20 percent discount. So the reps offer it. The signatures come in. Everyone exhales. And nobody notices that the company just repriced its entire enterprise book downward, because the next buyer's procurement team will have heard about that 20 percent before the first call.

That is the version of discounting that looks like velocity and behaves like a slow leak. On an 80 percent gross-margin product, a 20 percent price cut doesn't cost you 20 percent — it carves a quarter out of your gross profit, which means your reps now have to close roughly a third more volume just to stand still. Founders past $10M ARR paper over that with top-line growth right up until a quality-of-earnings review pulls the discount log and asks why realized ASP keeps drifting below list. The answer to that question is what moves your multiple, and not in your favor: McKinsey's work on B2B pricing discipline ties firms that hold defensible price floors to materially stronger valuation outcomes.

The reframe that fixes this is small and uncomfortable: a discount is not a sales tool, it is a financing decision. Every time a rep knocks the price down and gets nothing back, they have issued an interest-free loan with no maturity date and no covenant. In 2026, every buyer's playbook opens with "ask for 20 percent." If your team folds the first time, you haven't won a deal — you've confirmed the buyer's suspicion that the list price was fiction. That belief spreads. We unpack how fast it spreads in The Discounting Death Spiral: How Price Cuts Destroy Win Rates.

A price cut with nothing coming back is an interest-free loan you never agreed to make. The moment your rep signs it, your list price becomes a story the buyer no longer believes.

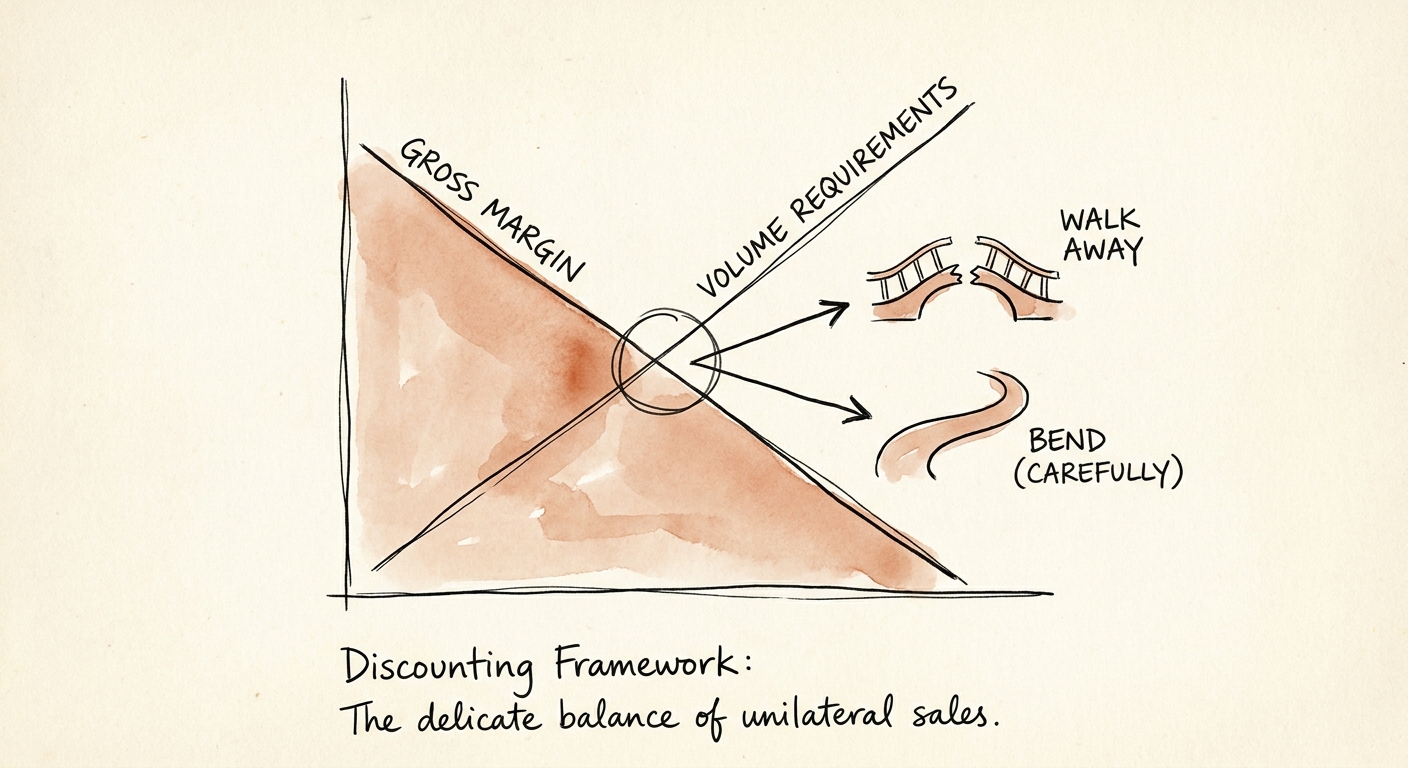

The walk-away test: would they take a worse deal if the price held?

You can't ask a sales team to hold the line if you've never told them where the line is. So draw it concretely: walk away when a prospect demands a price cut and offers nothing structural in return — no scope reduction, no longer term, no better payment timing. We call that the naked discount, and its only function is to let the buyer win the negotiation. There's a clean diagnostic for it: if the buyer won't accept a single trade — shorter feature set, three years instead of one, pay-up-front instead of monthly — in exchange for the lower number, the price was never the real objection. They wanted to test whether you'd flinch. Pull the proposal. A deal won purely on price is a deal you will eventually lose on price, and that churn is exactly the volatility a buyer discounts your multiple for.

Three patterns that should end the negotiation

The late-stage procurement ambush is the most common. Your champion has given the technical win, the deal feels done, and then procurement materializes demanding 30 percent for no reason except that it's their job to demand it. Hold. Caving here tells the entire account that your software is a commodity priced in a back room. Second pattern: the prospect who refuses any multi-year commitment but still wants volume-tier pricing — they want the discount that rewards loyalty without offering the loyalty. Third, and this one is arithmetic, not judgment: if a discount drops that specific deployment below a 65 percent gross margin, the deal is already dead; it just hasn't been buried. Run the math first — our breakdown of self-serve vs. high-touch gross margins shows how fast a "small" concession on a high-touch account goes underwater.

Walking away also protects something that doesn't show up on the pricing sheet: the cost of the customer you almost acquired. The Harvard Business Review found that customers landed through heavy discounting churn at far higher rates and consume well over twice the support load — they escalate more, expect more, and burn out the team. Every "no" to a deal like that is bandwidth returned to the customers who actually value what you build. Train your revenue org to read "no" as a margin-protection action, not a missed quarter.

When bending is the smart move: the price moves only if the terms move with it

Holding the line is not the same as never moving. There are concessions that genuinely improve a Series C company's unit economics — they just share one non-negotiable property: the price only drops when the terms get better for you in the same breath. Don't lower the price. Change the package. Here are the three trades worth making.

1. Cash now, in exchange for a discount

A customer who pays the full multi-year contract upfront is handing you capital you'd otherwise raise as expensive debt or dilutive equity. Giving back 10 to 15 percent for that is rational financing, not weakness. The Paddle 2026 SaaS pricing data ties annual-prepay-for-discount structures to roughly a third lower baseline churn and a CAC payback period cut in half — because a prepaid customer is a committed one. The discipline is in the modeling: know your true payback before you trade, which is the whole point of calculating real CAC payback rather than the flattering version.

2. A marquee logo, with expansion written into the contract

You can bend on the entry price for a logo that opens a market — but only if the contract carries legally binding expansion triggers, not a handshake about "growing together." That means a clause stating the price steps to standard rates at month thirteen, or seat thresholds that auto-reprice. If it isn't enforceable, it isn't a strategy, it's a hope.

3. Starving a competitor in a winner-take-all account

Occasionally you discount offensively — to lock a competitor out of an account that will become a category reference. That's defensible only while your LTV-to-CAC on the deal stays above 3.0. Below that, you're not playing offense; you're subsidizing a customer who'll leave the moment someone underbids you.

Here's what to do Monday: pull your last 20 discounted deals and sort them into "got something back" versus "naked." Then publish two numbers your reps can recite without checking — the gross-margin floor below which a deal is dead, and the standing list of trades that earn a price cut. The goal isn't fewer discounts. It's that every discount you grant bought you cash, a term, or a moat.