The practical answer

- Short answer

- The integration tax of a best-of-breed stack quietly discounts your exit. Here is how a diligence buyer reads 17 point tools, and when to consolidate.

- Best fit

- Industry: Technology. Function: Information Technology

- Operating path

- Process Documentation → Operational Excellence → Transaction Execution Services

- Key metric

- 40% Engineering bandwidth consumed by maintaining point-solution integrations

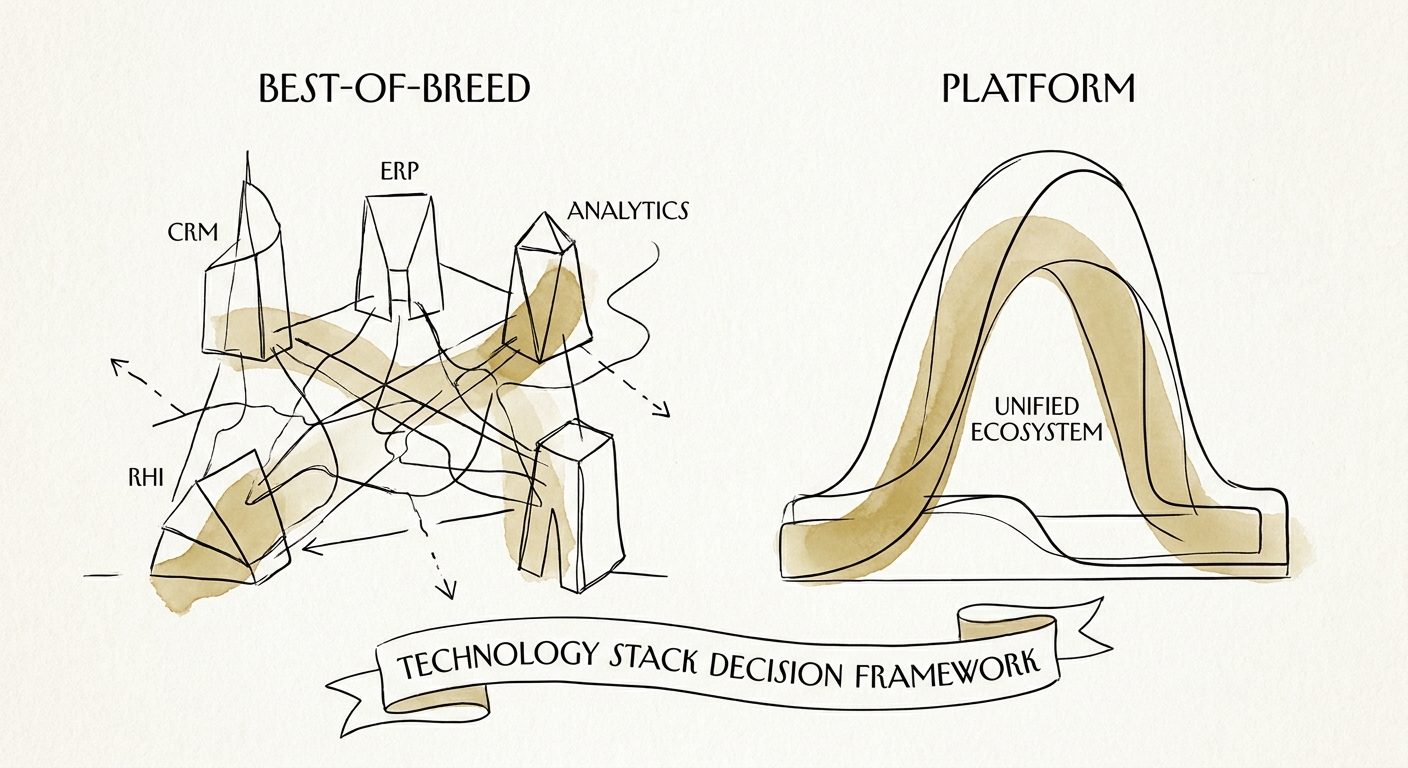

Seventeen tools, one onboarding flow, and a $2.5M discount

On a recent engagement I spent 120 days inside a $45M ARR SaaS company, mapping how a single customer moved from "signed" to "live." The answer ran through five vendors: Salesforce for the contract, an enrichment tool to fill in firmographics, a custom middleware script nobody had touched in eighteen months, Jira for provisioning tasks, and a marketing automation platform that fired the welcome sequence. The founder called this his competitive moat — the best tool for every job. The buyer I represented called it a $2.5 million operational liability and priced it straight into the offer.

That is the gap nobody warns founders about. A best-of-breed stack looks brilliant in the room where each department demos its own software. It falls apart the moment someone asks a cross-functional question: who owns the customer record when an enrichment vendor pushes a bad update at 2 a.m. and the onboarding queue silently stops moving? In a fragmented stack, the answer is "a senior engineer, manually, after the customer complains."

The real cost was never the subscription invoices — those are rounding error. It is the integration overhead I underwrite as a valuation discount. Every connection between two best-of-breed tools needs API maintenance, a middleware layer, and a human babysitter. Cyclr's 2026 analysis on B2B SaaS interoperability puts that tax at 30% to 40% of engineering bandwidth. Read that as: nearly half of the team you're paying to build product is instead plumbing connections between other people's software.

A best-of-breed stack wins the department demo and loses the diligence room. Buyers don't pay for tools; they pay for a process they can run on day one.

How a diligence buyer actually reads your stack

When I'm on the buy side, I am not grading the elegance of any one department's workflow. I'm grading three things: can this scale, where does it break, and can a new management team run it without the founder in the room. A heavily fragmented stack fails all three, and the artifact that exposes it is the one most founders never bother to produce cleanly — the process documentation.

Here is the test I actually run. I ask an operator to write down, end to end, how the sales-to-customer-success handoff works. If that document is one page describing one system, your company transfers with the keys. If it is a seven-tab diagram with arrows crossing four vendors and a footnote that says "ask the engineer named in the wiki," I write a discount. A documented process inside a single platform changes hands on day one. A documented process spanning seven tools is a glaring warning that operations live in someone's head, not the system.

The deeper risk surfaces in the code audit, and it lands in the quality-of-earnings memo as supply-chain exposure. When the product itself leans on a dozen third-party APIs, a single vendor deprecating one endpoint can take the product down. That fragility is also why integration is where deals quietly lose their math: Bain's analysis on process and systems integration in M&A finds that more than half of deal synergies depend on migrating to one set of systems fast, while fragmented targets routinely drive IT integration cost overruns of 20% to 50%. The fragmentation you bought as flexibility, the acquirer inherits as overrun. Before you ever go to market, run your own technology due diligence assessment and find the seams before a buyer's analyst does.

The consolidation decision — and how to make it 24 months out

Consolidating is not "platform good, best-of-breed bad." It's a sequencing call. The question to ask of every tool is narrow: does this system own a system of record, or does it just decorate one? Forecasting, ticketing, enrichment, and marketing automation almost always belong inside the system that already holds the customer — Salesforce, ServiceNow, or a consolidated ERP — because that is where the auditable record of the customer lifecycle should live. The specialized tool stays only when it does something the core platform genuinely cannot, and the migration cost is real and recurring rather than a one-time annoyance.

The waste this exposes is larger than most operators expect. Zylo's 2025 SaaS Management Index found large enterprises now manage hundreds of SaaS applications on average, a meaningful share of them licenses nobody opens. You are funding a graveyard of point tools while starving the core platform that drives enterprise value. The broader market already sees it — Cyferd's analysis of disconnected systems describes the same shift away from integration-heavy stacks toward unified platforms built for cross-functional work.

AI raises the stakes rather than changing the rule. You cannot bolt agents onto a fragmented stack and expect good decisions; they reason off whatever data layer you give them, and a fractured one produces confident wrong answers. BCG's 2026 report on AI in the tech function stresses that the deployments that pay off run on a shared platform that keeps agent logic separate from core systems — which is impossible when your "core" is seventeen tools held together with scripts. So here is what to do Monday: if you are inside 24 months of a liquidity event, pull a list of every active SaaS contract, mark which system of record each one touches, and circle every overlap. Then work my vendor consolidation playbook to retire the duplicates. A unified stack tells an institutional buyer the same thing a clean one-page process doc does: this business is mature, the data is trustworthy, and a new team can run it without you.