"Timing." Three months running.

A 90-person consulting firm closes the month, and the project-margin variance note on the dashboard reads "timing differences in revenue recognition." It said the same thing last month. And the month before. Nobody is lying. The controller is closing eight engagements, reconciling the PSA tool against the GL, chasing two project leads who haven't logged final hours, and the note is the last thing written at 9pm before the deck goes out. "Timing" is what you write when you've run out of time to find the actual reason.

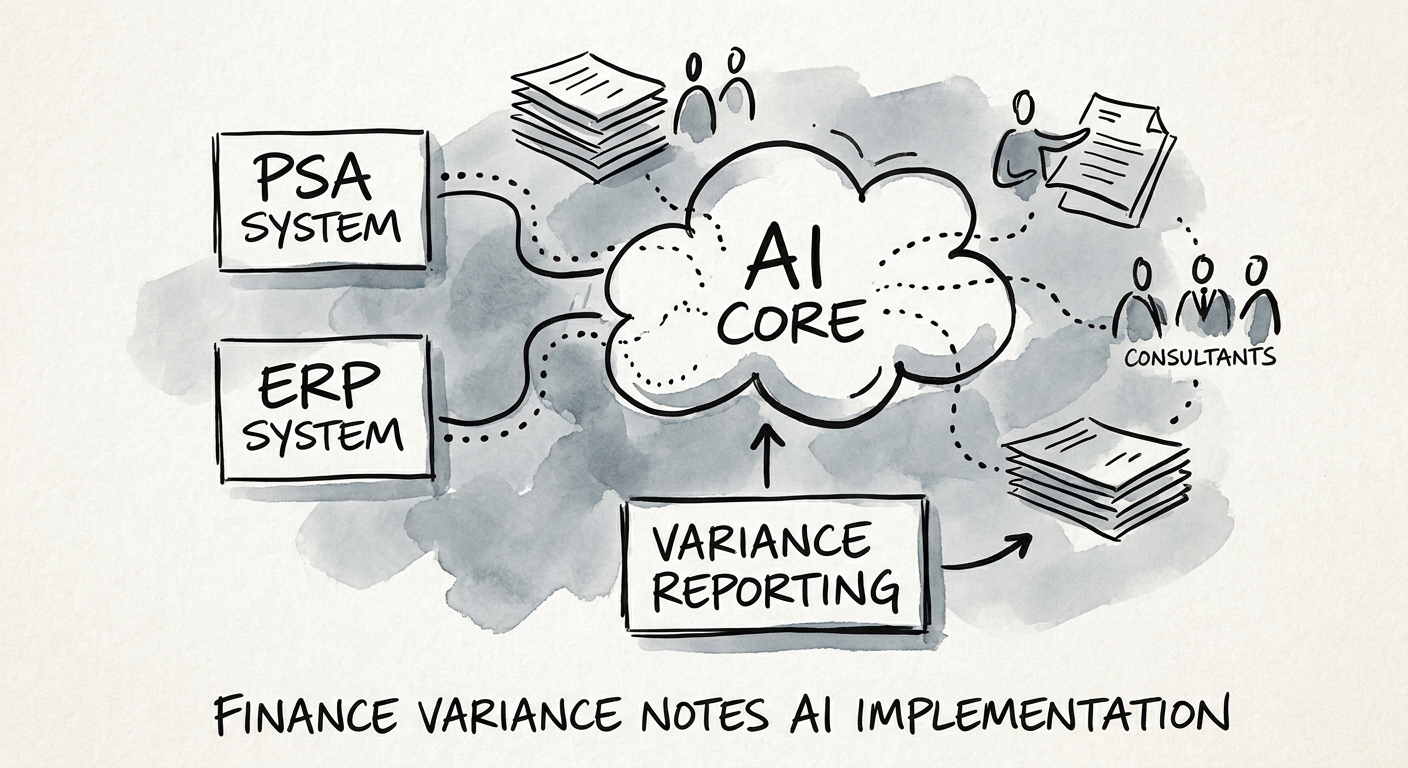

That sentence is exactly why finance variance notes are a strong first AI candidate inside a consulting firm — and exactly why most firms pilot it wrong. The variances that matter here are not generic. They are realization slipping because a fixed-fee build ran 30 hours over scope. A utilization dip because three consultants rolled off without a bench plan. A subcontractor cost that landed in the wrong project code. Deferred revenue that moved because a milestone got renegotiated mid-engagement. Each of those has a delivery decision behind it, sitting in a project lead's head, not in the ledger. Deloitte's State of AI in the Enterprise 2026 and the OECD's SME AI adoption report both show the adoption pressure is real and arriving in finance functions like yours; neither tells you what to point the model at first. Point it here: have AI draft the first-pass explanation from governed GL and PSA data, and keep the interpretation — the why — with finance and the engagement owner.

The failure mode is a note that reads beautifully and ties back to nothing. The model writes "project margin declined 4.2 points due to scope expansion on the delivery phase," it sounds authoritative, and no one checks that the PSA record actually shows the overage on that engagement. You haven't automated the explanation. You've automated the confidence with which a wrong explanation gets shipped.

Pick the number that proves it worked in one close

Run this for one close cycle and measure the right thing. The wrong metric is "how many notes did the AI draft" — drafting is easy and meaningless. The metric that matters in a consulting close is how many variance notes traced cleanly to a source: a GL line, a PSA project record, and a named engagement owner who confirmed the reason. Baseline it before you start. In most firms the honest baseline is uncomfortable: a real fraction of last quarter's variance notes were some flavor of "timing" or "phasing" — placeholder language for "we didn't get to it."

So track four things across the cycle. Days from final data load to a reviewed, owner-confirmed commentary. The count of variance notes the AI drafted that survived reviewer signoff without rework. Notes corrected because the source tie-out failed — the GL or PSA didn't actually support the claim. And notes still missing an engagement owner's input at signoff. If the AI shortens the close but the owner-input gap doesn't shrink, you sped up the wrong half: you're producing explanations faster without producing more accountability. The AICPA and CIMA AI resources are a useful reference for what "reviewed and supportable" has to mean before a note goes to a partner or a lender.

Only once those four numbers are tied to a named owner — not a tool, a person — is it worth running the AI Opportunity Score or the AI ROI Calculator to size the case across the rest of the close.

What you can put in place before the next close starts

The governance here is specific to finance data, and it's not optional — your variance notes feed partner comp models and, often, a bank covenant package. The NIST AI Risk Management Framework gives you the structure: write down the intended use (draft variance commentary), the risk (an unsupported note shipped as fact), the measurement (the four counts above), and who is accountable. The CISA AI data-security best practices should govern how the model touches engagement-level financials — access scope, retention, and what client-billing detail it's allowed to see at all, since a project ledger can expose more about a client relationship than the client would expect.

Concretely, before next close: require every AI-drafted note to cite its GL line and PSA record inline, so the reviewer can click through instead of trusting prose. Require an engagement owner signoff on any variance above materiality. Keep the close-calendar trail intact. And escalate — don't auto-draft — when the source data or the owner's reason is incomplete, because "the model wasn't sure" is information your controller needs, not a gap to paper over with "timing."

Expand to adjacent finance reporting — utilization forecasting, project-profitability commentary, the lender package — only after one full cycle proves the notes got shorter to produce and harder to wave through. If you want help mapping which close artifacts to pilot first and in what order, build the AI roadmap.