The practical answer

- Short answer

- Prevent value destruction in Snowflake partner acquisitions. A post-merger playbook for PE sponsors to navigate the 'Consumption Cliff' and retain elite data talent.

- Best fit

- Industry: Private Equity. Function: Post-Merger Integration

- Operating path

- Migration & Integration → Turnaround & Restructuring → Transaction Advisory Services

- Key metric

- 42% Average attrition of key technical talent (SnowPro Advanced) within 18 months of acquisition in poorly integrated deals.

The Valuation Thesis vs. The Integration Reality

Private Equity activity in the Snowflake partner ecosystem has reached fever pitch, with elite specialized firms trading at 12x to 15x EBITDA while generalist IT consultancies struggle to break 6x. The thesis is seductive: you aren't just buying a services firm; you are buying a data product company disguised as a consultancy. These firms don't just bill hours; they architect the consumption engines that drive Snowflake's own 30% YoY growth.

However, the integration reality often shatters this valuation within 12 months. The primary failure mode is treating a Snowflake Elite Partner like a generic Staff Augmentation shop. When PE sponsors impose traditional "billable utilization" metrics on a team designed to drive consumption, they trigger what we call the Consumption Cliff.

In a traditional IT services model, revenue is linear: Hours × Rate. In the Snowflake ecosystem, the real enterprise value lies in Influence Revenue—the long-term data consumption your architects enable. A single optimized data pipeline can generate recurring value for the client (and influence credit for the partner) for years. But if your integration plan forces your Lead Data Architects to chase short-term billable hours instead of strategic data modeling, two things happen immediately: client consumption stalls, and your best talent leaves.

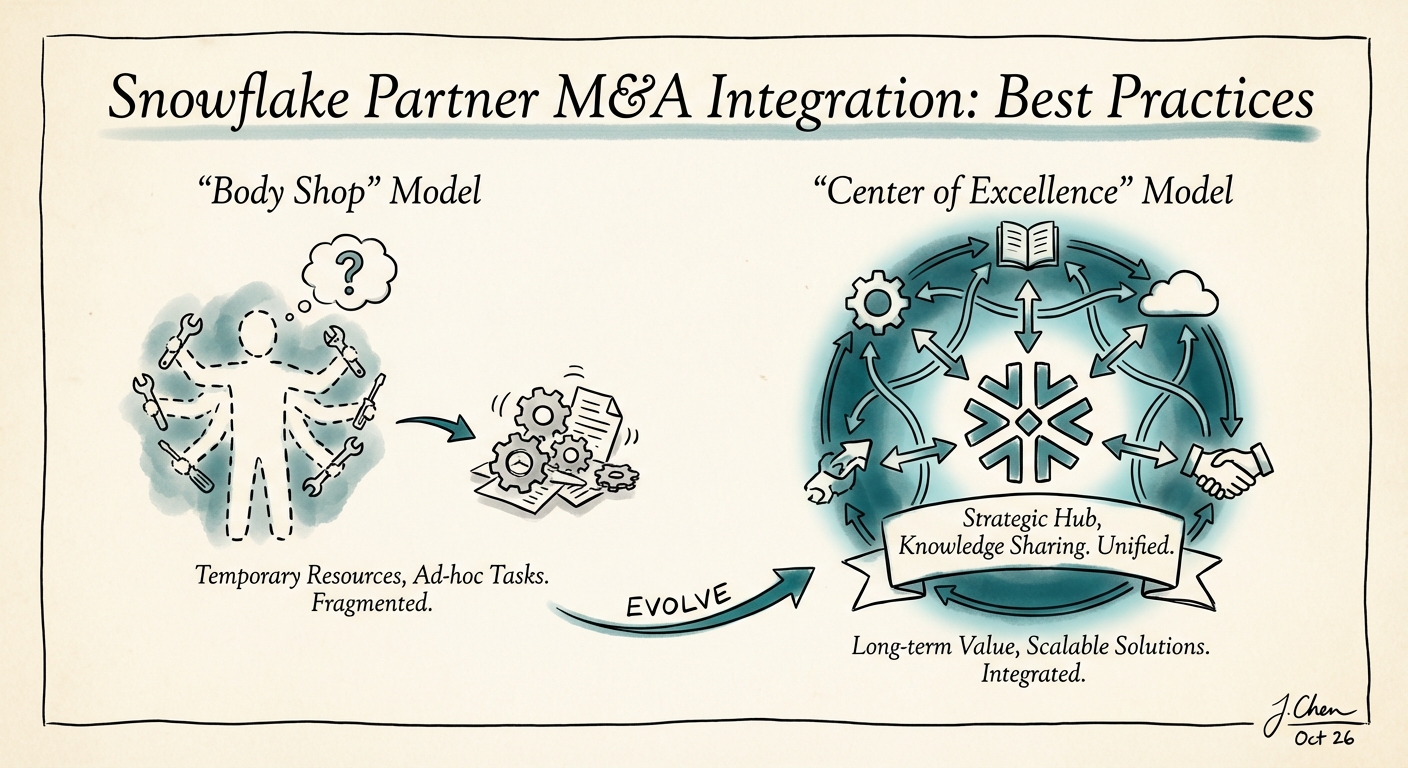

The "Body Shop" Trap

We consistently see acquirers make the mistake of merging a high-value Snowflake practice into a lower-margin generalist Managed Service Provider (MSP) to "capture synergies." This is mathematically flawed. You cannot blend a 60% gross margin "Data Product" business with a 35% gross margin "Infrastructure Support" business without diluting the former. The result is a culture clash that destroys value: SnowPro Certified architects, who view themselves as software engineers, refuse to work in a "ticket-based" support environment. They don't just quit; they go to your competitors, taking their client relationships—and the associated consumption revenue—with them.

You cannot blend a 60% gross margin 'Data Product' business with a 35% margin 'Infrastructure Support' business without diluting the former. The result is a culture clash that destroys value.

The "Consumption Cliff" and Revenue Quality

The most dangerous risk in Snowflake partner M&A is hidden in the revenue mix. Unlike SaaS companies with contractual ARR, Snowflake partners rely on Consumption-Based Pricing dynamics. Their "recurring" revenue is often tied to Managed Services wrappers around Snowflake consumption. If the partner stops innovating on the client's data estate, consumption flattens, and the client eventually churns or optimizes costs down.

Standard Private Equity integration playbooks focus on cost optimization—cutting "non-billable" time. In a Snowflake practice, that "non-billable" time is often R&D spent on building Accelerators and Native Apps that drive future consumption. Cutting it is akin to cutting R&D in a software company.

Diagnostic: Signs of Integration Failure

If you have recently acquired a Snowflake partner, check these three warning signs immediately:

- Utilization Spikes, Consumption Drops: Your team is billing more hours (short-term win), but client Snowflake consumption growth has flattened (long-term valuation killer). This means you are solving low-value tickets instead of building high-value data capabilities.

- The "SnowPro" Exodus: You are tracking overall attrition, but are you tracking certification attrition? Losing three junior analysts is noise; losing one SnowPro Advanced Architect is a signal that your technical culture is breaking down.

- Accelerator Stagnation: If the firm hasn't released a new industry-specific data model or Streamlit app in the last quarter, innovation has halted. You are now just a body shop.

Our data suggests that integration budgets are frequently under-scoped for these specialized firms. While the median retention budget is 1-2% of deal value, preserving a Snowflake practice often requires 3-5%, specifically allocated to retaining technical leadership who hold the "tribal knowledge" of complex data environments.

The 100-Day Integration Playbook

To preserve the 14x multiple you paid for, you must integrate differently. The goal is not just cost synergy; it is capability preservation.

1. Segregate the Operating Model

Do not fold the Snowflake practice into the general "Cloud Infrastructure" P&L. Keep it as a distinct Data & AI Center of Excellence (CoE). This allows you to maintain different compensation bands, utilization targets (lower is often better if high-value IP is being built), and cultural norms. This segregation prevents the "Body Shop" discount from eroding your premium asset.

2. Retention Beyond Cash

Cash retention bonuses have a half-life of 12 months. To retain SnowPro architects, you must offer Career Architecture. They want to work on the bleeding edge—Snowpark, Cortex AI, and Iceberg Tables. If your integration roadmap forces them to do legacy migrations for the next year, they will leave. Create a "Fellowship" track for top technical talent that exempts them from standard utilization pressures, allowing them to focus on high-impact presales and IP development.

3. The "Influence" KPI

Replace standard "EBITDA" targets for the practice leader with a balanced scorecard that includes Snowflake Partner Influence metrics. If they hit their EBITDA number but lose their "Elite" partner status due to dropping consumption or certification counts, the integration has failed. Align your incentives with Snowflake's own partner scorecard: Consumption Growth, Net New Logos, and Certified Individuals.

Ultimately, successfully integrating a Snowflake partner requires recognizing that you have acquired a technical IP business, not a staffing firm. The firms that win in 2026 will be those that can combine the operational discipline of Private Equity with the innovation engine of a data startup.