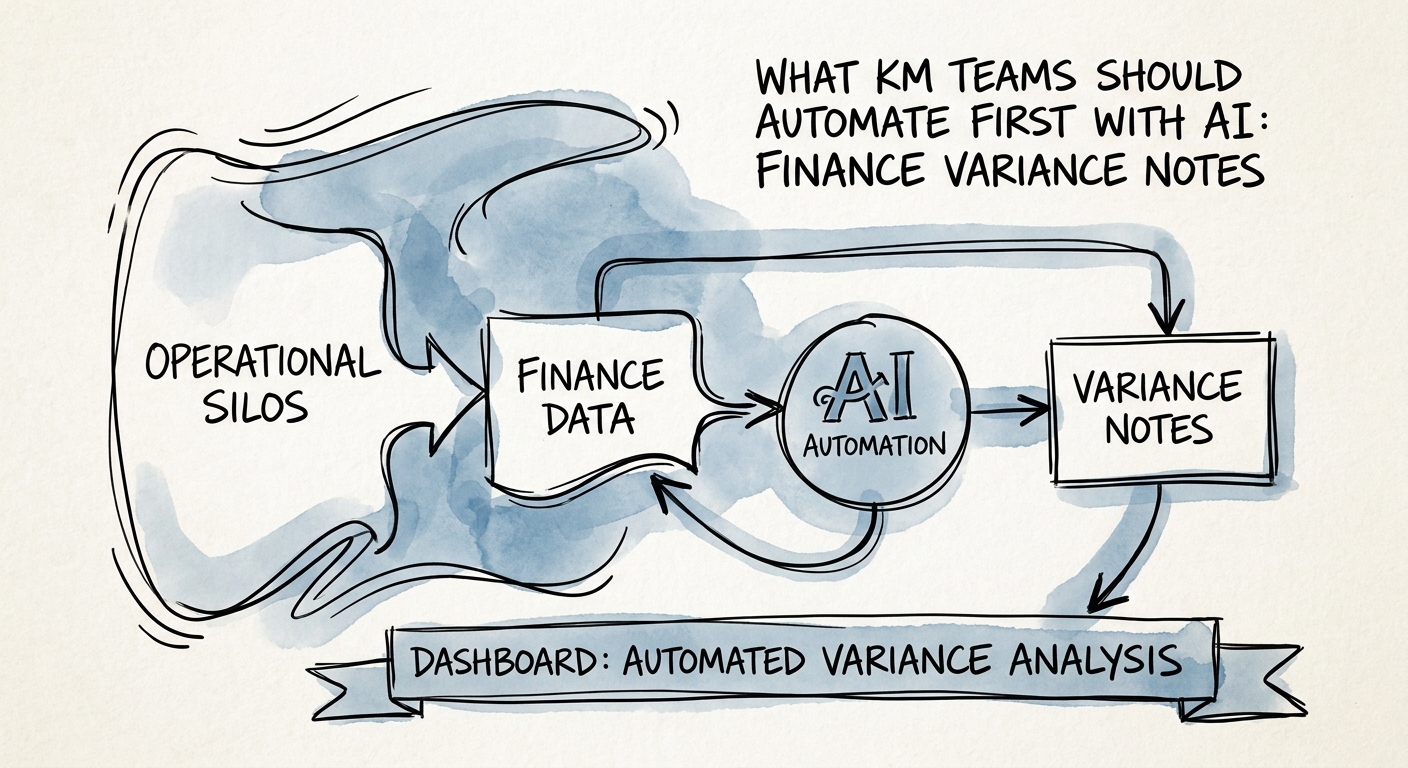

The note that holds up the whole close

It's day four of the monthly close. Marketing spend came in 31% over budget, gross margin slipped two points, and a controller is sitting in a Slack thread asking three different department heads "why?" while the CFO waits on the management pack. Nobody disputes the numbers. What's missing is the sentence that explains them — and the evidence behind that sentence. That sentence is the variance note, and in most growing companies it's assembled by hand, under deadline, by the person who can least afford the time.

That is exactly why it's the right first thing to point AI at. A variance note isn't really accounting; it's knowledge work wearing an accounting costume. Producing one means pulling the GL detail, checking the budget assumption that was set six months ago, seeing whether a CRM deal slipped or a delivery milestone moved, and then asking the department owner what actually happened. The number is the easy part. The hunt for context is the slow part — and the part AI is genuinely good at.

This isn't speculation about where the technology is headed. The RSM middle-market AI survey, the San Francisco Fed small-business AI analysis, and the OECD SME AI adoption report all describe the same pattern: smaller companies adopt fastest where the work is repetitive, evidence-bound, and currently eating a senior person's hours. A close-cycle variance note is all three. The trick is to translate "adoption is happening" into a specific design — which source feeds the note, who owns the explanation, and where a shaky answer gets escalated instead of shipped.

The line you draw down the middle of the workflow

Here is the failure mode that will burn you, and it's specific to this document. Ask a general assistant "why did marketing spend run 31% over budget," and it will give you a fluent, confident, plausible answer — "increased campaign investment ahead of Q3 pipeline targets" — that nobody can trace to a transaction. It sounds like a variance note. It reads like finance wrote it. And it might be completely wrong, because the real driver was an annual software renewal that landed a month early. A wrong variance note isn't a typo; it's a false statement in a document leadership uses to make decisions.

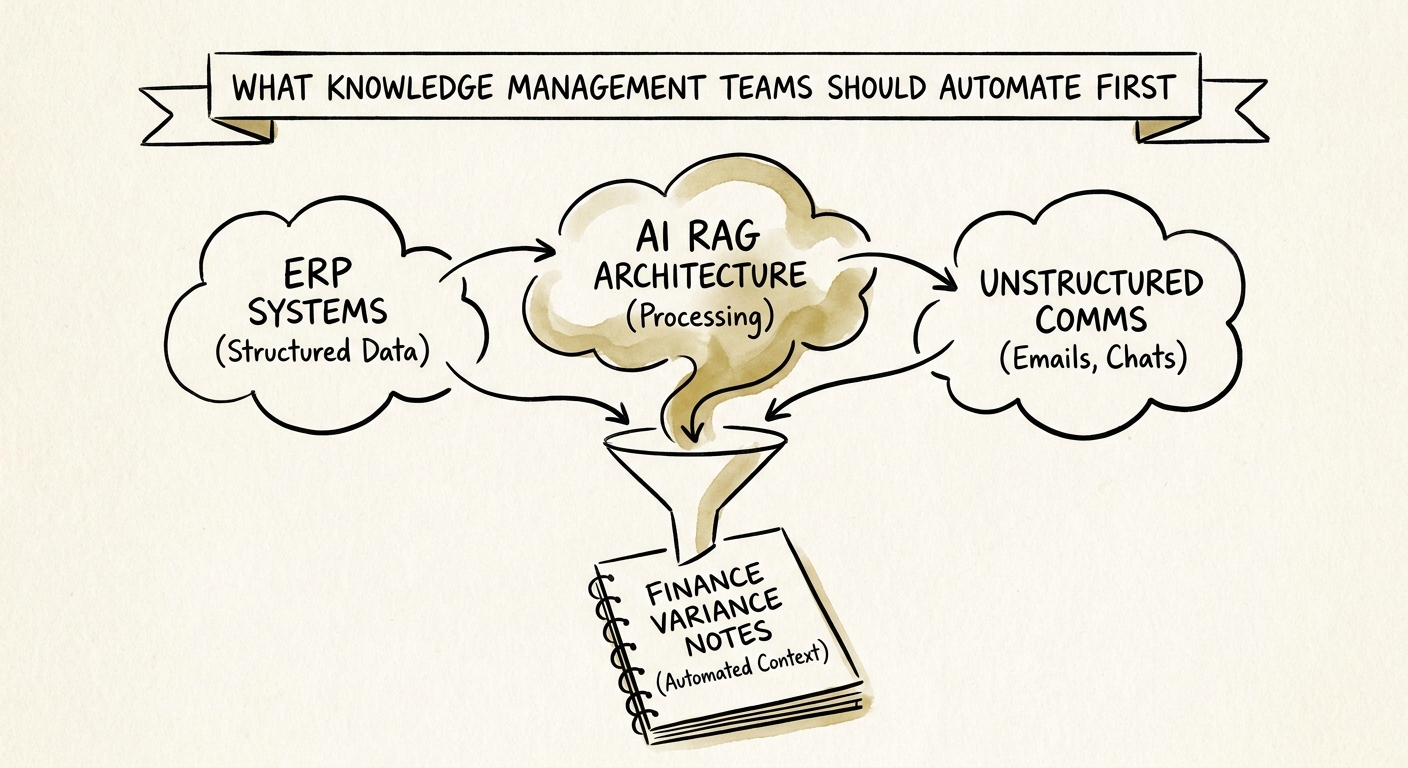

So draw a hard line: AI assembles evidence, finance decides causality and final wording. Everything on the gathering side of that line is fair game to automate — retrieving the GL transactions behind a variance, surfacing the original budget assumption, flagging which CRM deals and delivery milestones moved in the period, pulling last quarter's commentary on the same line. Everything on the judgment side stays human: what caused the movement, how confident we are, and the exact sentence that goes in the pack.

Build the data discipline before the prompt. The NIST AI Risk Management Framework gives you the language for context, reviewer accountability, and measurable risk on this specific note; CISA AI Data Security Best Practices tells you how to treat the sensitive feeds — ledger detail, budget files, headcount, vendor spend, deal-level CRM data — in terms of what gets exposed to a model, what gets logged, and what never leaves the building. If you run a hosted assistant, the OpenAI enterprise privacy commitments are part of that exposure decision, not an afterthought.

Then give every note a structure the reviewer can audit at a glance: the variance threshold that triggered it, the source records behind the explanation, the named owner who explained it, a confidence flag, finance signoff, any unresolved question, and whether it made the management pack. That packet turns "the AI said so" into a trail somebody can defend in a board meeting.

Run it on one variance class, and watch the close meeting

Don't roll this across every line on the P&L. Pick one material variance class — say, the recurring fight over marketing or services-delivery cost — and have the assistant do nothing but assemble the source packet for it. Finance still writes the verdict. The job in the pilot is to prove the model can show its work: every explanation must point back to a GL, CRM, or delivery source. The moment it can't — the moment it produces an explanation with no traceable evidence — you've found a broken source system, not an AI problem, and you fix the plumbing before you add another model on top of it.

Deloitte's State of AI in the Enterprise 2026 makes the useful point that the question is no longer "did we run a pilot" but "did it produce production value." For a variance note, production value is measurable and unsexy: time to draft the evidence packet, what share of flagged variances have a source behind them, how often finance corrects the AI's draft, how fast department owners respond, and how much rework the close meeting still generates. If the controller spends day four deciding actions instead of hunting transactions, it's working. Keep a visible unresolved bucket too — some variances genuinely need an owner to chase something down before any evidence becomes commentary, and pretending otherwise is how bad notes get shipped.

Two things to do this week. Use the manual-work scoring guide to confirm your variance process is actually worth automating before you build anything. Then stage the real work with the 90-day AI implementation plan — source cleanup first, then a single-variance prototype, reviewer training, launch, and only then a decision about expanding to more lines. The signal that you're ready to widen the lane is simple: the close meeting stops being an evidence scavenger hunt and starts being a conversation about what to do next.