The duplicate that AI signs off in 0.4 seconds

Picture a 90-person B2B services firm. Same vendor sits in the master file three ways: "Acme LLC," "ACME, L.L.C.," and "Acme Consulting" with a slightly different remit-to address. An invoice arrives, AI reads it, can't find an exact match, creates a fourth record, routes it to an approver who recognizes the vendor name, and pays it. Three weeks later the original invoice — the one that was actually owed — gets paid against a different record. You just paid twice, and the audit trail shows two clean, fully-approved transactions. Nobody did anything obviously wrong. That's the trap.

Invoice routing looks like the perfect first thing to automate: high volume, repetitive, rules-driven. But routing is the last step in a chain — capture, vendor match, PO/receipt match, policy check, approval — and AI inherits every weakness upstream of it. The NIST AI Risk Management Framework is built around exactly this problem: you map the context, measure the failure modes, and manage the risk before the system changes consequential decisions. For accounts payable, the consequential decision isn't "which queue does this go in" — it's "does money leave the building."

So run three blunt checks before you automate anything. One: can you pull a deduplicated vendor list where every active vendor has a single, verified remit-to? Two: does your three-way match actually reconcile, or do half your invoices land as "PO not found" because receiving never gets logged? Three: is your approval matrix written down, or does it live in the controller's head as "anything over $10K, ask me"? If any answer is no, you're not automating routing — you're automating the propagation of bad data.

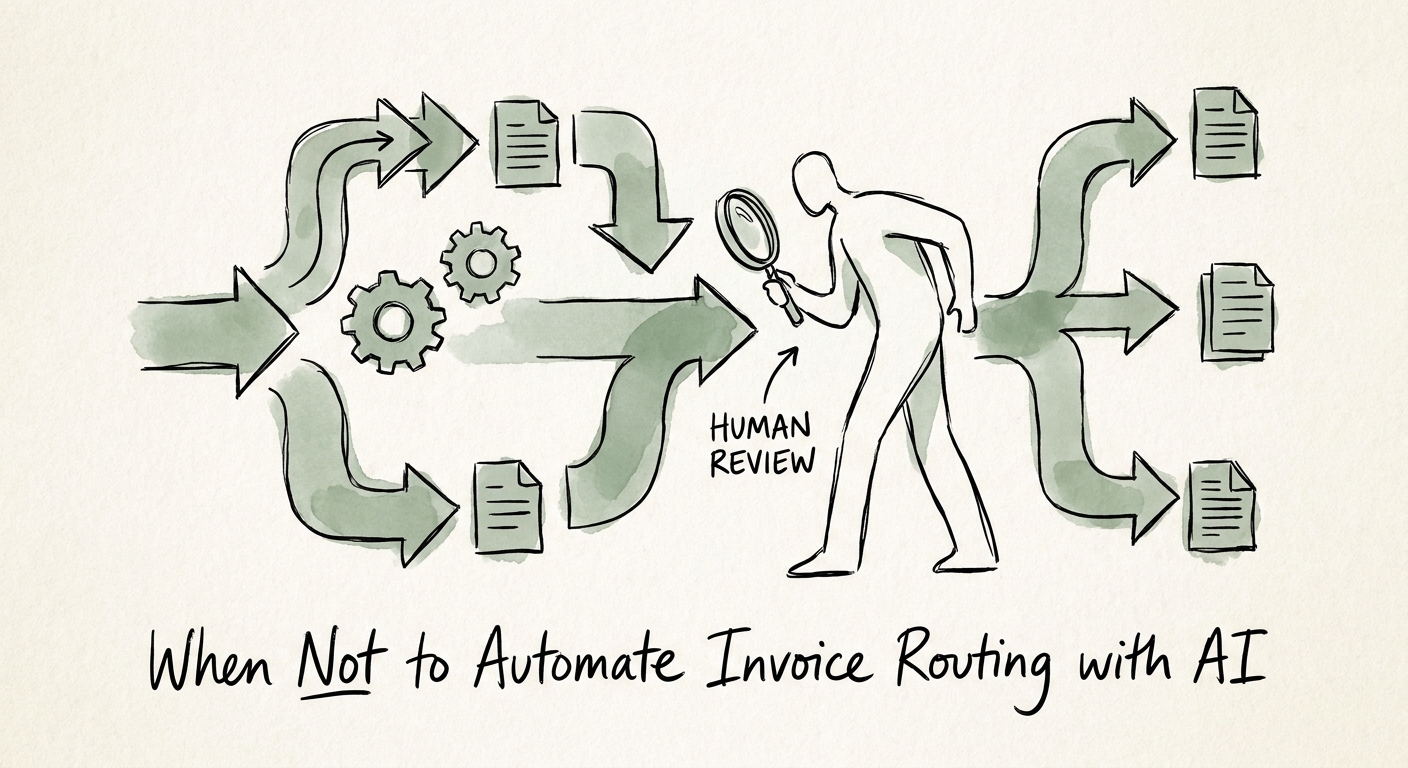

Point AI at the exceptions, not the happy path

Here's the inversion most teams miss. The clean invoices — matched PO, known vendor, under threshold — are already cheap to process; a clerk clears them in seconds and they're low-risk. The expensive, dangerous invoices are the exceptions: the new vendor with no history, the amount that's 8% over the PO, the duplicate-looking charge, the net-15 term that should be net-45. Automating the happy path saves you minutes on the invoices that never hurt you. The leverage is in making exceptions visible and routed to a human fast, not in pushing approvals through quicker.

The IBM Institute for Business Value AI capabilities research frames AI value around operating capabilities rather than the model itself — and in AP, those capabilities are unglamorous: a clean vendor master, codified policy logic, an exception queue someone actually owns, and a measurement loop. Used inside those rails, AI earns its keep: classify invoice type, suggest the right approver from the matrix, flag a remit-to that doesn't match the vendor record, catch a near-duplicate by amount-plus-date-plus-vendor, and drop anything ambiguous into a finance-owned exception queue with the reason attached.

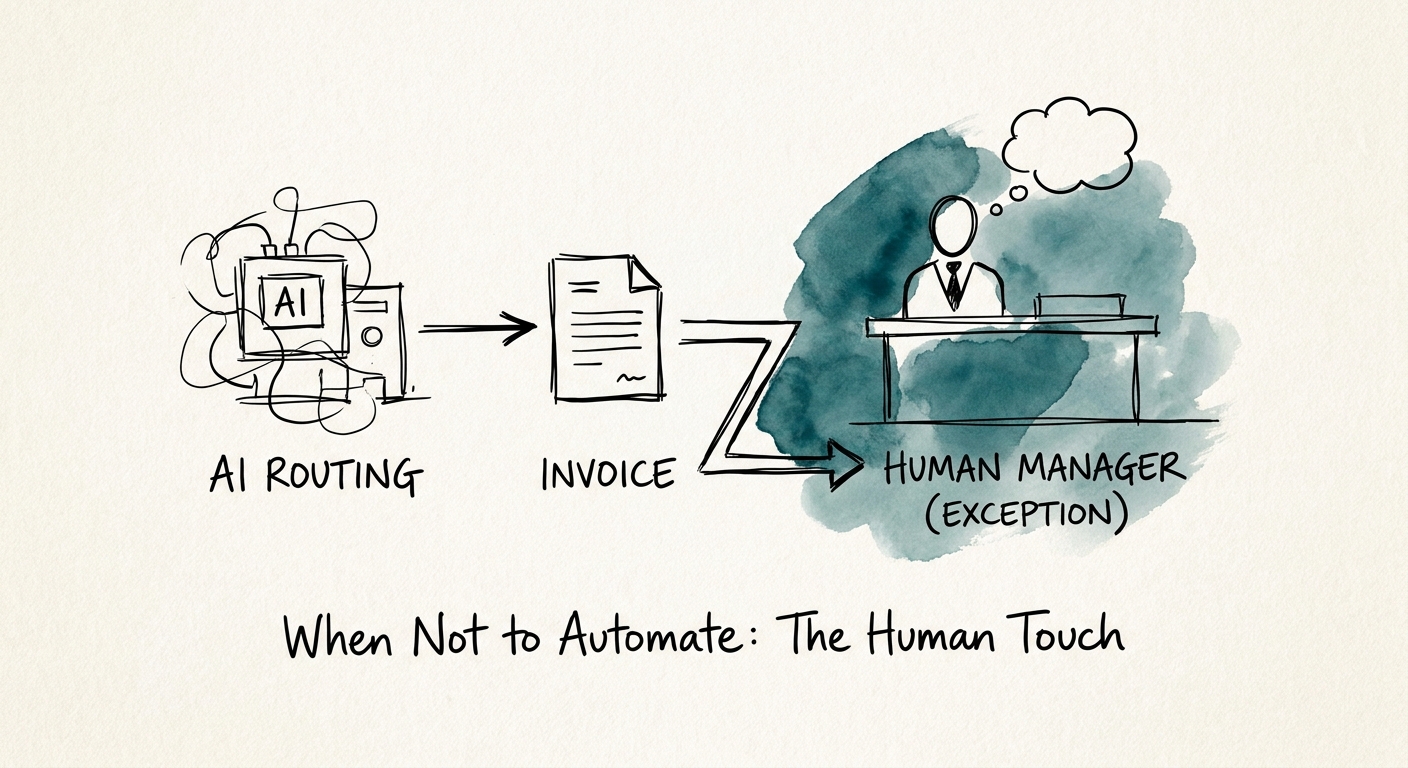

What stays human is the judgment AI can't be trusted with under pressure. The PwC Responsible AI survey reinforces why: the controls have to be deliberate, not assumed. Keep a person in the loop for first-time vendors, bank-detail changes (the single most common business-email-compromise vector in AP), amounts over the match tolerance, and any invoice that conflicts with policy. The AI's job is to make those four categories impossible to miss — not to wave them through because the OCR confidence score was high.

Measure controls, or you've shipped a faster mistake

The seductive metric is cycle time, and it's the one to be most suspicious of. A routing process that's 40% faster but quietly weakened your three-way match isn't a win — it's a longer leash on duplicate and fraudulent payments. Track the control metrics alongside the speed one: duplicate-detection rate, exception rate (and whether it's falling because controls improved or because the threshold got loosened), approval rework, false-approval catches, and audit completeness — can you reconstruct, for any payment, who approved it and against what evidence?

That last one is non-negotiable when AI touches financial records. The Microsoft 365 Copilot data protection architecture is a useful reference point for what "permissioned and auditable" should look like in practice: identity scoping, data protection, and a logged trail of what the system saw and did. Apply the same bar to AP. If your AI router can't produce a defensible record of why it routed an invoice the way it did, your external auditor will, eventually, make you produce it by hand.

The Monday move: don't kick off an automation project — kick off a vendor-master cleanup and write down your approval matrix. Pull the active vendor list, dedupe it, verify remit-to and bank details for your top 50 by spend, and document who can approve what at which dollar threshold. That work makes AI routing safe later and pays for itself immediately in fewer manual exceptions. When the foundation reconciles, Operations and Finance AI is where to scope what to automate next. Or run the five-minute AI Opportunity Score to see where your finance ops actually have room to automate safely.