The practical answer

- Short answer

- Zendesk is no longer just a help desk. Discover why specialized CX partners are seeing 12x valuation multiples by pivoting from ticket resolution to AI containment.

- Best fit

- Industry: CX Technology. Function: Alliances & Strategy

- Operating path

- Revenue Architecture → Commercial Performance → Office of the CFO

- Key metric

- 12x Potential EBITDA multiple for partners with 'Managed Intelligence' models vs. 5x for pure implementers.

The Shift: From 'Help Desk' to 'Resolution Architecture'

For the last decade, the Zendesk partner ecosystem was defined by a simple, reliable business model: implementation. You helped a mid-market company migrate from a shared inbox (or a clunky legacy system) to a structured ticketing environment. You set up macros, configured triggers, and trained agents. It was honest work, but in 2026, it is a commodity.

The market has shifted violently. Zendesk is no longer positioning itself as a mere "support tool." With its aggressive pivot to the Resolution Platform and a projected $200M in AI-driven recurring revenue in 2025, Zendesk has re-architected its value proposition around automation rather than organization. The old metric was "ticket volume handled." The new metric is "containment rate."

This splits the partner ecosystem in two. The "Ticket Resolvers"—firms that simply configure the software—are seeing their billable hours compress as time-to-value shrinks to under eight weeks. Meanwhile, the "CX Strategists"—firms that deploy AI agents, optimize resolution workflows, and integrate customer data—are seeing explosive growth. These partners aren't selling setup; they are selling vertical-specific efficiency and customer retention.

The market has moved from 'managing tickets' to 'eliminating them.' The partners who help clients use AI to stop problems before they reach a human agent are the ones who will command 12x exits.

The Valuation Gap: 5x Implementers vs. 12x Strategists

In the private equity markets, not all service revenue is created equal. We are observing a distinct valuation gap opening up within the CX systems integrator market, mirroring trends we've seen in the ServiceNow ecosystem.

The Commodity Trap (5x EBITDA)

Partners focused on "Lift and Shift" migrations trade at lower multiples. Their revenue is project-based, non-recurring, and highly susceptible to price competition. With Zendesk's out-of-the-box functionality improving, the "technical debt" that used to justify large implementation fees is vanishing. If your primary value prop is "we know how to configure the settings," you are in a race to the bottom.

The Intelligence Premium (12x EBITDA)

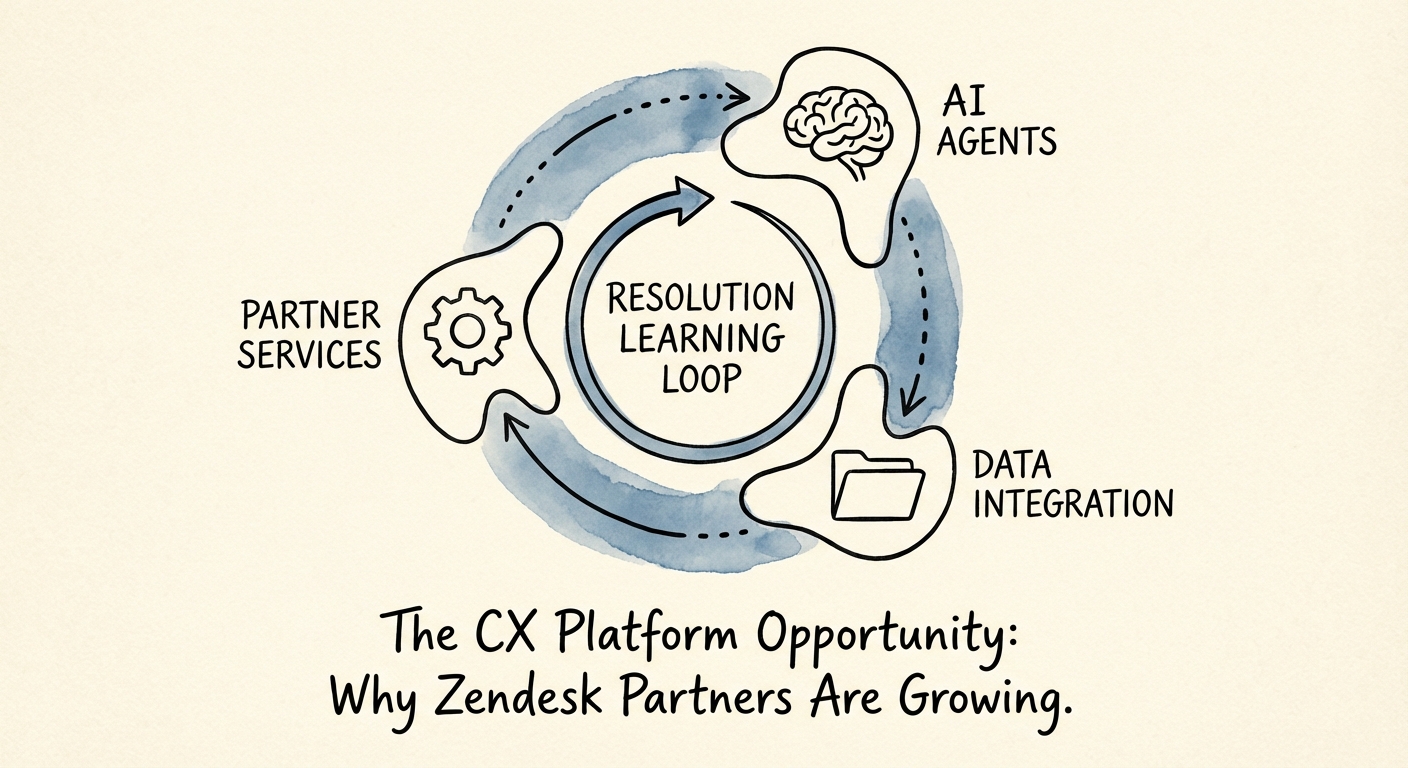

The partners commanding premium multiples are those building Managed CX Intelligence practices. They don't just set up the tool; they run the "Resolution Learning Loop." They charge monthly retainers to:

- Analyze conversation data to identify friction points.

- Tune AI agents to increase deflection rates from 20% to 60%.

- Integrate Zendesk with downstream systems like Snowflake or Salesforce Data Cloud to personalize the experience.

Investors pay for this model because it is sticky. Once a partner is embedding themselves in the logic of how a company interacts with its customers, they become irremovable. This shifts the revenue quality from "one-off project" to "recurring strategic advisory," a critical factor in valuation expansion.

The Playbook: Pivoting to AI Containment

To capture this opportunity, partners must fundamentally change their engagement model. The days of billing for "seat licenses" and "admin hours" are ending. The future is billing for outcomes.

1. Sell 'Containment,' Not 'Support'

Stop pitching a better ticketing system. Pitch a reduction in cost-per-contact. Advanced partners are going to market with a promise: "We will deploy AI agents that resolve 40% of your tier-1 inquiries without human intervention within 90 days." This is a CFO-level value proposition that commoditized implementers cannot match.

2. The Data Integration Wedge

Zendesk wins against Salesforce Service Cloud on TCO and agility, but it often loses on the perception of "enterprise data connection." Partners bridge this gap. By building specialized connectors to ERPs and CDPs, you turn Zendesk into the "action layer" of the tech stack. This requires technical talent that understands APIs and data schemas, not just support workflows.

3. Verticalize Your AI Models

A generic AI agent is helpful; a vertical-specific one is transformative. Partners who build pre-trained intent models for specific industries—like FinTech compliance checks or E-commerce returns logic—create defensible IP. This moves you from a services firm to a tech-enabled platform, the holy grail of exit valuations.