The Monday before the forecast call

Picture the call most revenue teams dread: the number slipped $340K from last week, the CFO wants to know why, and the answer is twelve minutes of "let me pull that up." A rep says a deal pushed. The manager half-remembers a discount conversation. Finance writes "slip - timing" in the pack and everyone moves on, having explained nothing. Two weeks later the same deal pushes again, and nobody connects the two because the first note was a guess dressed as a fact.

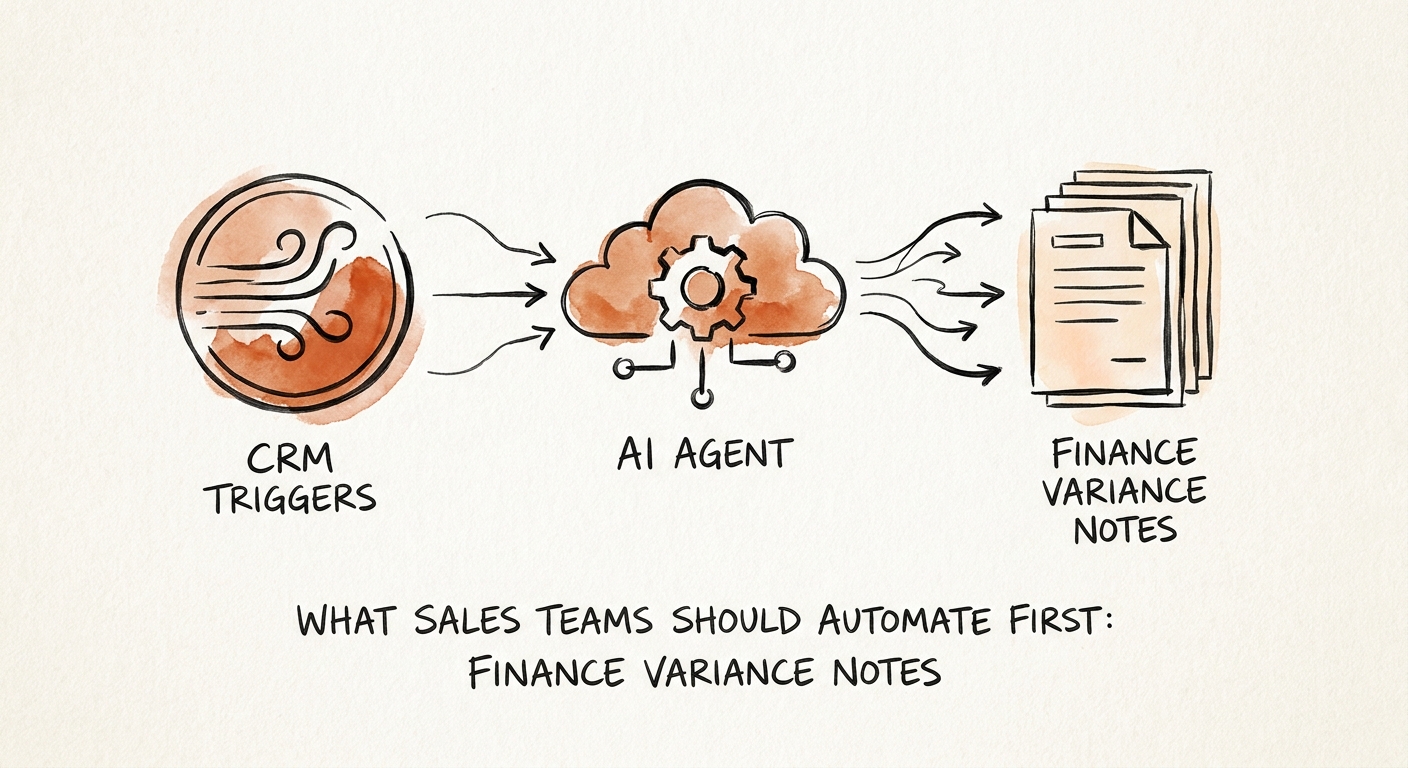

That gap — between a forecast number changing and anyone being able to say why, with receipts — is the single best place for sales operations to point its first AI workflow. Not lead scoring, not email drafting. Variance notes. The reason is unglamorous: the evidence already exists, scattered across stage changes, close-date edits, call summaries, email threads, and deal-risk fields. A human assembling that by hand burns an hour per deal and still misses half of it. AI assembling it turns an hour into ninety seconds, leaving the manager and the finance partner to do the one thing software cannot — decide whether the explanation is actually true.

That split matters. Salesforce's State of Sales research keeps surfacing the same complaint — reps lose hours to admin and reporting that should be automated — and Deloitte's State of AI in the Enterprise 2026 shows the projects that stick are the narrow, evidence-heavy ones, not the open-ended copilots. A variance note is exactly that shape: bounded input, defensible output, a human signing the bottom.

Pick one variance class, and make AI show its work

Do not try to explain the whole pipeline in week one. Pick a single variance class and pilot it cold: deals that slipped a close date this week. Just slips. The AI's job is narrow — for each slipped opportunity, pull the stage at last forecast versus now, the prior and current amount, the close-date edit and who made it, the most recent call or email note, the current deal-risk field, and the owner's last logged next step. Then it drafts one paragraph: what changed, the evidence behind it, and a confidence flag.

The non-negotiable design rule is that the note separates evidence from interpretation on the page. "Close date moved from Q2 to Q3; last call note (May 14) cites legal review pending; no next step logged since" is evidence. "Deal is at risk" is interpretation — and interpretation is the human's call, not the model's. When AI is allowed to blur those, a plausible sentence becomes forecast truth, and the forecast quietly fills with confident fiction. Say a 60-person SaaS company runs this on a Tuesday: the slip note that says "no next step logged in 19 days" is worth more than any narrative, because it tells the manager exactly what to fix on the call.

This is also why governance belongs in version one, not version three. Forecast commentary steers spending, hiring, and board guidance, so it sits squarely in the territory the NIST AI Risk Management Framework was built for — measure the thing before you trust it. Track five numbers from day one: how often finance accepts the note unedited, how often it corrects causality, how many notes get flagged because the source CRM field was stale, time-to-draft per variance class, and how many flagged accounts actually get a follow-up. If a note can't cite the CRM record or conversation behind a change, it ships as low-confidence — never as fact.

The low-confidence pile is the real prize

Here is the counterintuitive part that separates a useful pilot from theater: the notes the AI can't confidently explain are more valuable than the ones it can. When a slip note comes back tagged low-confidence "no source," that is rarely an AI failure — it's a rep who edited a close date with no logged reason, or a stage that's been stuck at "Negotiation" for six weeks with zero activity. Surface that pile to the manager every week instead of hiding it. You'll find that a quarter of your variance is unexplainable because the underlying CRM hygiene is rotten, and no amount of additional reporting fixes a field nobody fills in.

Two guardrails before this touches anything sensitive. First, variance notes drip with confidential signal — pricing concessions, renewal risk, a rep's private read that a champion just left. Set access, retention, and reviewer permissions per the CISA AI data-security best practices before account evidence ever flows into the workflow; not every seller note belongs in a finance pack. Second, keep the human gate explicit — the manager approves the note, then finance uses it. One review loop, no exceptions.

Run it for one quarter on slips alone, then compare the forecast call before and after: minutes spent hunting evidence, finance edits per note, follow-ups actually closed. If the only thing that improved is that reps sound more articulate, you built the wrong thing. If the call now opens with "three slips, all missing next steps, here's the fix" — you built the right thing, and you've earned the right to add the next variance class. To put a dollar figure on the management hours you're reclaiming, run the numbers in the AI ROI Calculator, and use the AI Opportunity Score to check whether variance notes really beat your other candidate workflows before you commit a quarter to them.