The practical answer

- Short answer

- Two services firms, same AI pitch, wildly different worth. How PE sponsors tell a software multiple from a body-shop multiple in 2026 diligence.

- Best fit

- Industry: Technology Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 40% Predicted cancellation rate for enterprise agentic AI projects by 2027, exposing implementation risks.

Two firms, the same deck, a five-turn gap

Last year a sponsor handed me two CIMs in the same week. Both pitched "AI-native" delivery. Both showed the same hockey-stick revenue. One deserved a software multiple. The other was a staffing firm that had bolted a model onto an intake form — and was asking to be paid like the first. Telling them apart took about forty minutes inside the data room and saved a buyer from overpaying by roughly five turns of revenue. That gap is not unusual right now; it is the defining mispricing of the moment.

The mispricing has a source. McKinsey's 2025 State of AI Report found that while roughly 80% of companies are deploying generative AI, about the same share report no significant lift to their bottom line. So the buy-side is awash in firms that use AI and starved for firms whose AI actually changes the economics. The deck never tells you which one you're looking at. The cost-of-revenue line does.

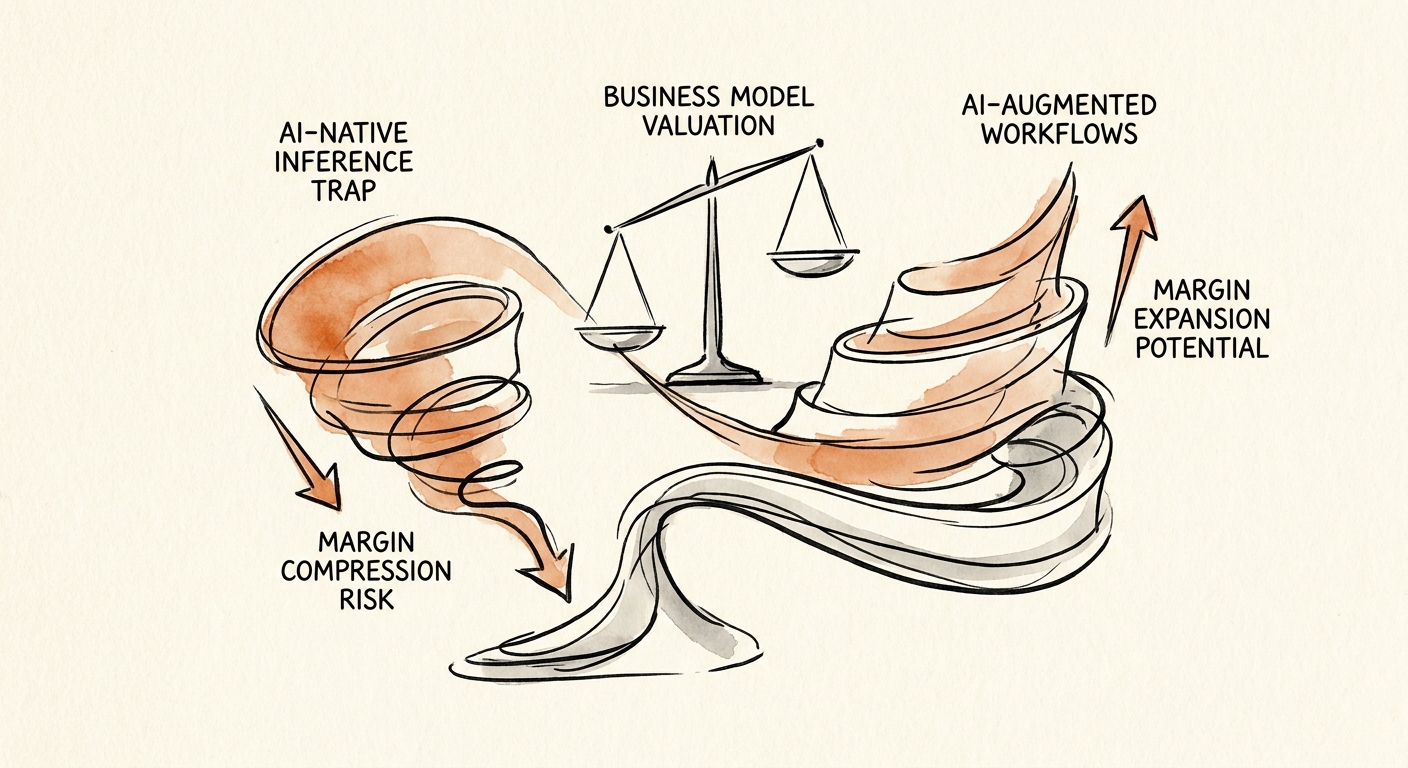

Strip away the labels and there are only two engines under the hood. In an AI-augmented firm — the consultancy, the agency, the managed-service shop — the delivery engine is still humans, and AI makes those humans faster. Revenue still scales with headcount; the model just bends the slope and fattens the margin. In an AI-native firm, a proprietary model or agent is the delivery mechanism, so revenue and headcount come unglued. Both can be good businesses. They are not the same business, and a buyer who pays one price for either is the buyer who gets carried out.

Run the gross margin line down the page. If it falls as usage climbs, you are not buying software at any price — you are buying a body shop with a chatbot, and the multiple has to come back to earth.

The trap hides on the line that goes the wrong direction

The seductive number is the headline. TechConstant's 2026 AI Valuation Analysis pegs AI startups at median revenue multiples of 25x to 30x — four or five times what mature public SaaS trades at. That number is doing enormous work in pitch decks, and almost none of it survives contact with the unit economics.

Here is the part the multiple ignores. A true AI-native firm has traded a payroll for a compute bill. Classic B2B SaaS lives at 80% to 90% gross margin because serving the next customer costs almost nothing. AI-native delivery runs closer to 50% to 60%, because every query burns inference, hardware, and third-party API spend — and that spend climbs with usage. So the line you watch in diligence is gross margin plotted against customer activity. In real software it's flat. In the inference trap it bows downward: the more the product works, the thinner each dollar gets. A buyer who models flat compute and discovers escalating compute after close watches post-close cash flow evaporate exactly when the cohort is supposed to be paying off. This is why an AI-enabled target demands a different build of adjusted EBITDA in a services acquisition — you are normalizing a cost that grows with the very revenue you're underwriting.

Now flip it. The AI-augmented firm is the quieter, sturdier story, and it's the one most middle-market services owners actually have. By pushing AI into onboarding, first-draft work product, and data prep, these firms strip out layers of junior cost while keeping the low-capital, high-margin shape of a services business. Bain's 2025 Tech Services Report finds that leaders who genuinely reshape delivery this way can lift revenue multiples by 3.0x to 3.5x while holding or expanding EBITDA margins. Note what that firm is not doing: it isn't paying a compute bill that grows with revenue, and it isn't claiming software economics it can't defend. It's a better services business, priced as one — and that's frequently the more reliable place to put capital.

Three things to demand from the data room

You cannot underwrite this off top-line growth or booked pipeline. BCG's 2025 Global AI Study found only 5% of companies are "future-built" to generate value at scale, while about 60% see minimal returns despite heavy spend. If a target wants the AI-native premium, make it prove non-linear scale on paper. Three asks settle most arguments.

First, ask what's under the wrapper. If the entire moat is a thin API layer over a commoditized foundation model, you're not buying a company — you're buying a feature that the underlying model's next release can absorb. Push past the interface to the proprietary data: the highest-value AI services own specific, ring-fenced data that feeds a reinforcement loop a hyperscaler can't replicate. No loop, no defensibility. That single distinction is the spine of any serious technology due-diligence red-flag review before a binding LOI.

Second, plot gross margin against usage for the top cohorts — the trap from the section above shows up here or it doesn't. Third, stress the delivery floor. Gartner's 2026 Agentic AI Forecast predicts over 40% of enterprise agentic AI projects get canceled by 2027. For an augmented firm, that means scrutinizing churn, customer-success metrics, and consultant utilization: if the tools quietly underdeliver, the firm re-hires humans to honor fixed-fee contracts and the cost structure balloons overnight. The discipline is the same in every case — price the asset on the hard EBITDA it produces today, treat tomorrow's AI margins as upside you didn't pay for, and let the seller earn them in the earnout.