The email finance sends you every month

It's the fourth business day of the month. Finance has closed the books, your support cost line came in over plan — say 14% over — and there it is in your inbox: the email every CS leader knows by heart. "Can you explain the variance by end of day?" Now you're reverse-engineering last month — pulling ticket exports, scrolling Teams threads, asking your team lead whether that staffing gap was the contractor backfill or the holiday coverage, hunting for the credit batch that hit a big account. Two hours later you've written four sentences that finance will paraphrase into the board deck.

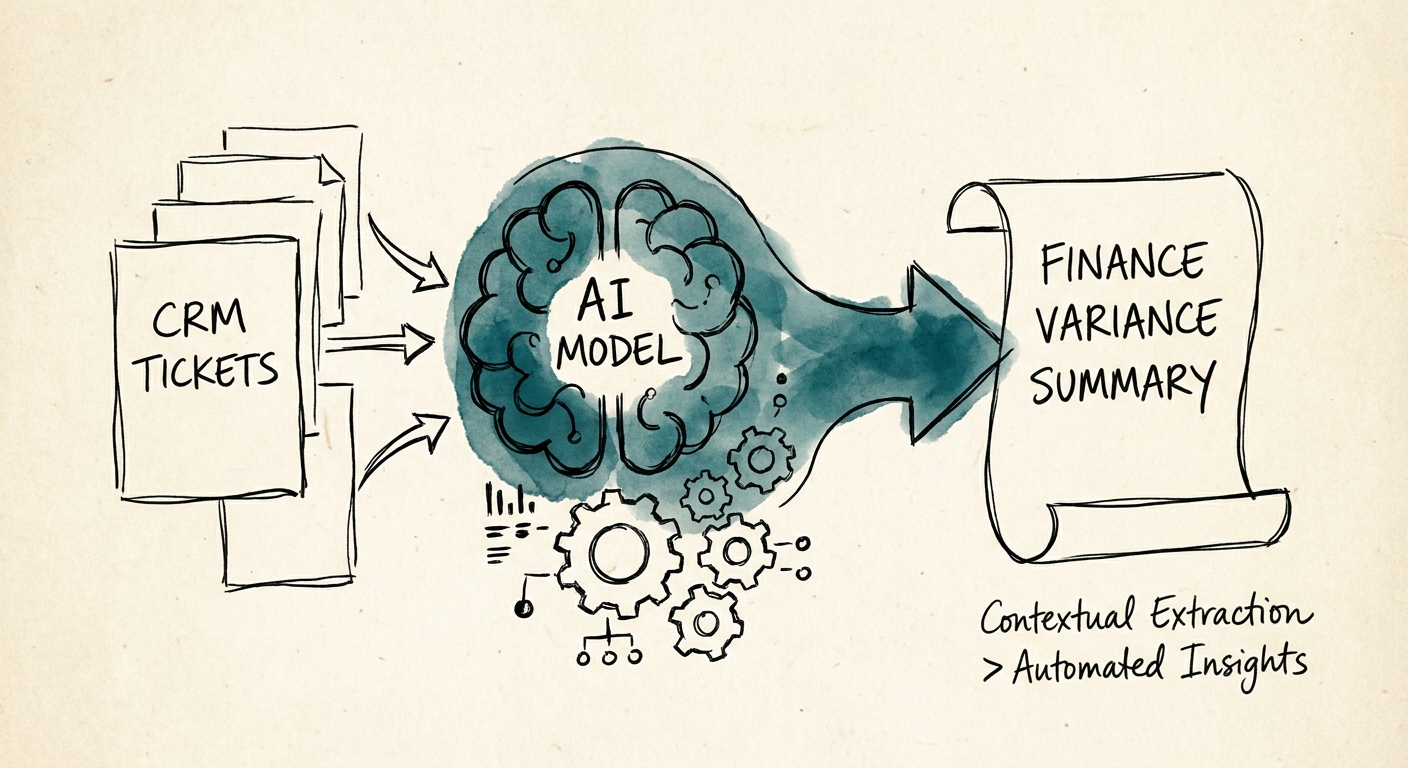

That two-hour archaeology dig is exactly the kind of work a service team should hand to AI first. The reasons it's a good candidate aren't glamorous — they're the same boring fundamentals that separate AI projects that stick from the ones that quietly die. The IBM Institute for Business Value AI capabilities research lays out what those fundamentals are: reliable data, clear process ownership, real adoption, and measurement. A variance note hits all four because the source records already exist — you're not asking the model to invent anything, just to assemble what's scattered across systems into the explanation finance needs.

The catch: the model is only as good as your category mapping. If "credits" means something different in your ticketing tool than it does in the finance ledger, the draft will confidently explain the wrong number, and you'll spend your saved two hours untangling it. That's why the PwC Responsible AI survey keeps landing on the same point — outputs that feed management reporting need practical controls, not enthusiasm.

Draft the story. Never own the number.

Here's the line, and it's the whole game: the AI prepares the explanation, finance owns the explanation. Those are different jobs.

Concretely, a good variance-note workflow does three things. It drafts the narrative — say, "support hours ran over plan, driven primarily by a coverage gap during the contractor transition and a large credit batch issued to one enterprise account after a migration incident." It cites the source records behind each claim, so a finance analyst can click through to the ticket batch or the staffing log instead of taking it on faith. And — this is the part teams skip — it flags where the evidence runs out: "the remaining portion over plan is not explained by available records." That last sentence is worth more than the polished prose, because it tells finance exactly where a human still needs to dig.

What it must not do: create or suggest a financial adjustment, smooth over a gap with a plausible-sounding guess, or present an inference as a fact. The NIST AI Risk Management Framework is the right mental model here — the higher the decision impact, the tighter the controls, and a number that lands in management reporting is high impact. A draft that says "likely seasonal" when no record supports seasonality isn't helping; it's manufacturing a story finance might repeat to the board.

And because the raw evidence for a service variance lives everywhere — ticket exports, a finance spreadsheet, a Teams thread where someone explained the outage, a shared doc with the staffing plan — permission-aware retrieval isn't optional. The Microsoft 365 Copilot data protection architecture shows what that needs to look like: the system only surfaces what the requester is already allowed to see, and every retrieval is auditable. Before a draft touches a management report, you want to be able to answer "where did this sentence come from?" for every sentence.

The one number that tells you if it's working

You can track time-to-prepare, source coverage, and recurring unexplained causes — all useful. But the metric that actually matters is the finance correction rate: how often does finance have to rewrite the draft before it goes into reporting? Start it high and watch it fall. If after a quarter finance is still rewriting half your notes, the problem isn't the model — it's your category mapping or your evidence trail, and no amount of better prompting fixes that.

The honest test of success isn't "we automated variance notes." It's whether a sharper, better-sourced explanation actually shortens the close conversation and points an owner at something to fix — a coverage model that keeps blowing up, a credit pattern that signals a product problem. That's the difference between a faster narrative and an automated judgment you didn't mean to delegate.

Monday move: pick last month's ugliest variance, write down every source you'd need to explain it, and check whether those sources are even reachable and consistently labeled. That inventory tells you in an afternoon whether you're ready to automate. When you are, draw the human-owns-the-number boundary explicitly — see when not to automate finance variance notes — and put guardrails around it via AI governance and training.