"Sales comp accrual timing" is the sentence that ends careers

Picture the monthly close at a 90-person SaaS company. Gross margin dropped four points versus forecast. The AI-assisted variance packet renders a tidy line: "Margin variance driven by hosting cost increases and sales comp accrual timing." It reads beautifully. It goes into the board deck. And it is wrong — the real driver was a single enterprise deal that got booked with a one-time professional-services component nobody flagged in the model.

That is the trap with variance notes specifically. Unlike a marketing email or a meeting summary, a variance note is a causal claim presented to people who will allocate capital based on it. AI is genuinely good at the mechanical layer — diffing actuals against budget, forecast, and prior period across hundreds of GL accounts in seconds. What it cannot do is know that the hosting spike was a deliberate, board-approved migration, or that the comp "timing" was actually a structural plan change finance hasn't reflected yet. IBM's Institute for Business Value research on AI capabilities is blunt about the dependency: the output is only as good as the data model and operating context feeding it. A variance engine reading from a chart of accounts that has three different ways to book implementation revenue will confidently explain the wrong thing.

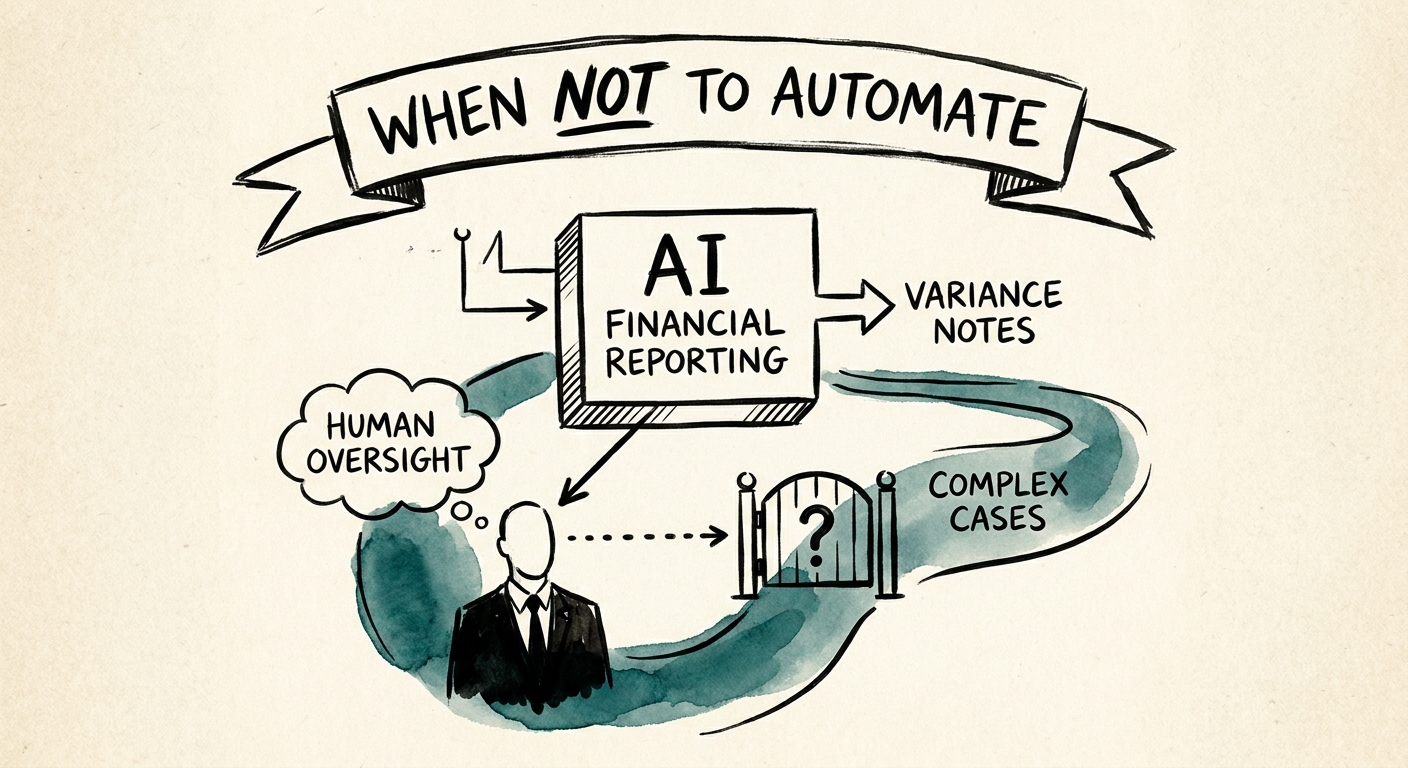

McKinsey's State of AI 2025 makes the point that value comes from redesigning the work, not bolting AI onto the existing step. For FP&A that redesign is precise: let AI build the evidence packet — the quantified bridge, the source-system references, the candidate drivers ranked by dollar impact, and an explicit list of variances it could not source. Then a human writes the sentence that goes to the board.

Draw the line at the dollar threshold and the audience, not at "does it read well"

The mistake most finance teams make is gating automation on quality of prose. If the paragraph is coherent, it ships. That is exactly backwards, because a fluent explanation of a $40K rounding variance and a fluent explanation of a $400K revenue-recognition miss look identical on the page. The gate has to be the size of the number and who reads the note.

The NIST AI Risk Management Framework gives you the sequence to do this cleanly — map, measure, manage, govern — and it translates directly into a variance policy you can write on one page. Map: which account ranges and variance bands exist. Measure: what dollar and percentage thresholds matter to your board. Manage: AI may auto-draft anything below, say, a $25K / 5% materiality floor; the controller reviews everything between the floor and a higher ceiling; the CFO personally signs anything that moves a board-tracked metric like gross margin, NRR-driven revenue, or runway months. Govern: every override gets logged with who changed what and why.

The audience axis matters as much as the dollar axis. A variance note for the internal forecast review can run on AI draft with light review. The same number headed for an audit committee or a lender covenant package cannot. PwC's Responsible AI survey keeps returning to the same finding: controls that exist during the pilot quietly evaporate once the tool is "working." For finance that decay is dangerous, because the first month the AI gets a covenant-relevant variance wrong is the month you learn your reviewer trail was theater. Write the threshold table, name the owner for each band, and require source links on every drafted driver — so a reviewer can click from "hosting cost increase" straight to the invoice line, not take it on faith.

The five numbers that tell you whether the AI is earning trust

You don't decide to expand automation by feel. Instrument it. Track these monthly: reviewer edit rate (what fraction of AI-drafted notes the controller rewrites — if it stays above a third, the model is guessing); unsupported-driver count (drivers the AI named but couldn't link to a source); source-citation coverage (the percent of variance dollars traced to an underlying transaction); board-packet corrections (variances restated after distribution — this should trend to zero before you trust anything above the materiality floor); and repeat-category drift (the same account explained differently month to month, which usually means the chart of accounts, not the AI, is the problem).

Run those five for one full quarterly cycle before you let AI draft anything that reaches the CFO's signature. If you can't trace the dollars yet, the honest first move isn't a better prompt — it's fixing the source systems the variance reads from. Walk the boundaries in the finance variance workflow guide, and if your chart of accounts is the real bottleneck, start with a QuickStart AI Audit to inspect what the model is actually reading before you automate a single note.