Your worst payer and your biggest renewal are often the same logo

Picture a 110-employee B2B SaaS company with a $180K ARR account sitting 58 days past due. The aging report flags it as delinquent. What the aging report doesn't show: that customer opened three SLA tickets last quarter, was promised a service credit nobody applied yet, and comes up for renewal in seven weeks. An AI dunning sequence reads "58 days, no payment" and fires a firmer-toned reminder. Now your VP of Customer Success is doing damage control on a deal that was going to close - over an invoice the customer was right to hold.

That's the trap specific to recurring-revenue businesses. In transactional sales, a late invoice is mostly a cash problem. In SaaS, accounts receivable and the renewal pipeline run through the same relationship, often the same buyer. The question isn't whether AI can write a payment reminder - any model does that in a sentence. It's whether the system knows the difference between "this customer forgot" and "this customer is withholding payment on purpose because we owe them something."

That distinction lives in data your collections automation usually can't see: the credit memo waiting in someone's inbox, the procurement portal that requires a re-issued PO, the executive sponsor who left in March, the dispute logged in the support tool but never reconciled against the ledger. Gartner's work on AI in customer service keeps landing on the same point: automation amplifies whatever judgment - or absence of judgment - sits behind it. Point it at clean, low-stakes accounts and it's a gift. Point it at a contested invoice on a strategic logo and you've just industrialized a mistake.

The four invoices a bot should never touch on its own

Most of your AR ledger is genuinely safe to automate - the customer simply forgot, and a templated nudge works. The danger concentrates in a small set of accounts. Sort your aging report against these four flags before any sequence goes out, and route anything that hits one to a human.

First, the disputed invoice. The customer has challenged scope, an overage charge, a usage true-up, or whether the SLA credit was applied. Here AI should do the unglamorous work - pull the contract clause, the ticket history, and the billing record into one summary - so a person can answer in minutes. It should not send a "friendly reminder" that tells the customer you weren't even reading your own dispute queue.

Second, the account that renews inside 90 days. A bot doesn't know it's negotiating in the shadow of a renewal. A finance leader does. McKinsey's research on how B2B winners grow ties expansion revenue directly to relationship quality - and nothing degrades it faster than a tone-deaf collections email two weeks before a renewal conversation. Cross-reference the AR queue against the renewal calendar; that overlap is your manual-review pile.

Third, anything that proposes terms. Payment plans, partial waivers, late fees, interest, conversion to annual prepay, or a pause on access. These change revenue recognition, touch the contract, and sometimes invite legal exposure. AI can draft the options and show the math. The decision to offer them belongs to finance leadership or the account owner - never to a send-on-schedule rule.

Fourth, the "we're escalating" message. Service suspension, hard deadlines, collections-agency language. The downside of getting tone wrong on a real customer is asymmetric, and an LLM has no instinct for which logo can absorb a sharp note and which one will screenshot it for their CFO. The EY Responsible AI Pulse survey and PwC's responsible-AI research both keep returning to the same boundary: keep the human in the loop precisely where the cost of an error is irreversible. A late payment is recoverable. A churned reference customer usually isn't.

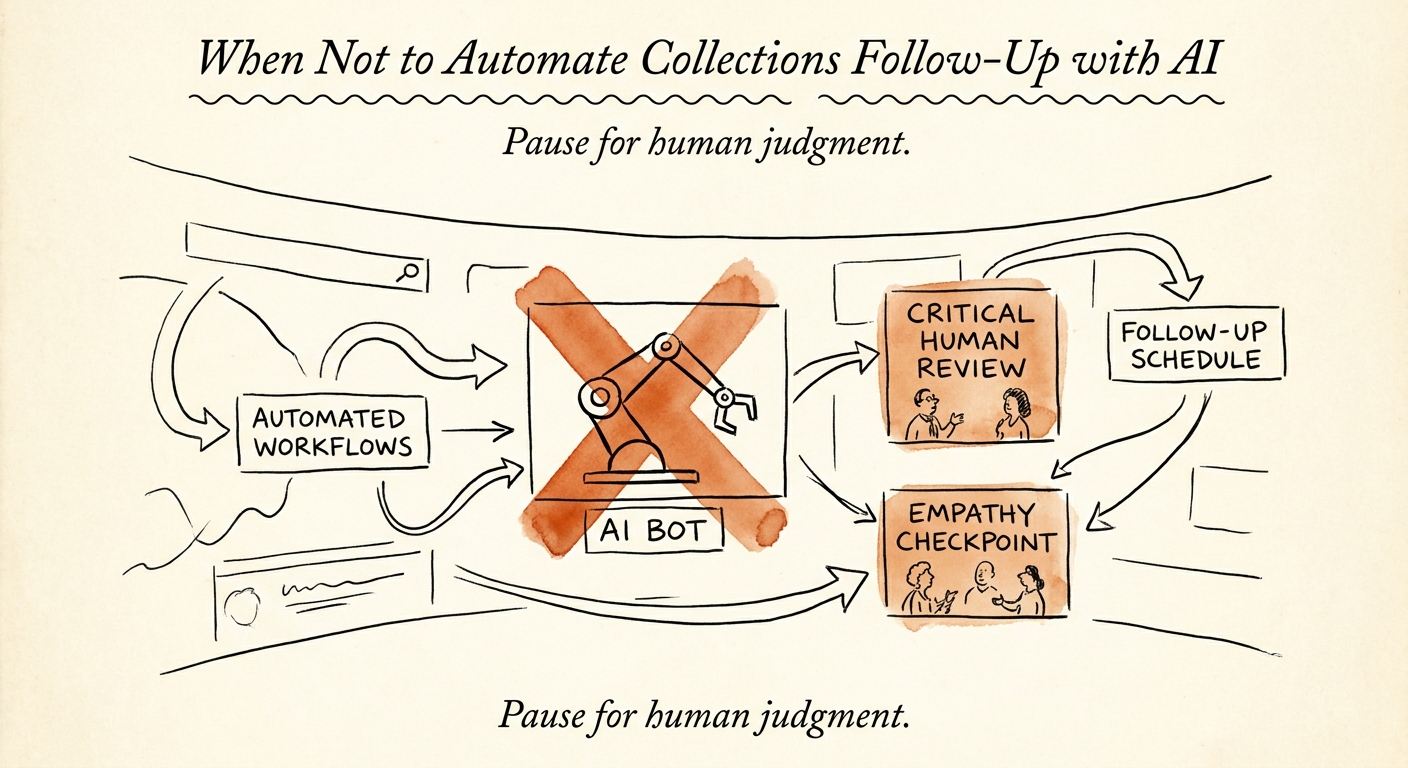

What to actually wire up Monday

Stop thinking about this as "should AI send the dunning email." Split the workflow into preparation and outreach, and automate the preparation aggressively. For every overdue account, have AI assemble one reviewable card: invoice and amount, days past due, payment history, open support tickets, the relevant contract clause, renewal date, and current account owner. A controller who used to spend twenty minutes digging across four systems per account now reads a card in two and decides what happens next.

Then classify, don't just remind. Tag each account as routine, exception, or executive-review. Routine - small balance, no disputes, no near-term renewal - gets the approved reminder template on schedule. Exception routes to finance or CS with the context already attached. Executive-review accounts get no external message at all until a human picks the relationship path. The reason a $3K logo and a $180K renewing logo should not share a dunning cadence is that they don't share a downside.

For the routine tier, AI workflow automation for collections follow-up is where DSO actually moves - disciplined nudges and clean routing, no judgment required. Use the AI assistant governance framework to set who can approve what, what gets logged, and where the review gate sits. And if you haven't picked a first AI workflow yet, run the AI Opportunity Score before you point anything at a customer's inbox. As MIT Sloan Management Review's AI coverage argues, the teams that win with this stuff aren't the ones who automate the most steps - they're the ones who automate the right steps and keep a person on the ones that touch a relationship. In SaaS, collections is one of those.