The screenshot that costs you the multiple

Picture the diligence room. A private equity associate has your revenue export open and is highlighting one line: "AI Platform — $1.4M." You've spent two years telling the market that line is software. Then they pull the engineering time records, and they find your two best solution architects logged 1,900 hours last year deploying, patching, and babysitting that platform for eleven clients. The associate doesn't argue with you. She just drags that $1.4M out of the software column and drops it into services, where it gets a fraction of the multiple. In one keystroke, the asset you built to escape the billable hour gets repriced as the billable hour.

This is the specific trap for IT services and technology consulting firms, and it's almost never a product-quality problem — it's a structural one. Bain & Company's 2025 Technology Report on AI Monetization describes the pattern bluntly: consultancies fold software R&D into the same P&L that books delivery hours, so they never see that the "product" is carrying delivery costs that no real software company would tolerate. Gartner's 2026 AI Services Market Guide puts numbers on the gap that's hiding underneath: custom AI development runs around a 45% gross margin, packaged AI software around 85%. Firms that try to live in the middle build a "productized service" — a thing too hand-built to scale like software and too cheap to price like senior strategy work. You end up with a low-margin product that needs a high-cost human to run, which is the worst cell on the grid.

And the damage compounds at exit, not in the moment. A buyer who spots bloated deployment cost doesn't just discount the AI line — they start asking what else in your "recurring" revenue is actually disguised labor. If you want to see how sophisticated acquirers separate genuine software economics from dressed-up services on a single P&L, that re-classification mechanic is the same one walked through in The Services Valuation Matrix.

Your moat isn't the model — it's the 200 implementations behind it

Here's the version of this I see most often. A roughly $40M digital-transformation firm builds a clever generative agent — say, for supply-chain exception handling — and then prices it as a one-time deliverable inside a larger integration engagement. The logic feels reasonable in the moment: bundle the tool, win the $500K project. But you've just handed away the only thing that could have carried a software multiple in exchange for one more services invoice. You taught the market that your IP is a sweetener, not a product. That's the fastest way to cap your own exit value, and most firms do it without noticing.

The deeper mistake is what they choose to build. Thin wrappers around a foundation model feel like product because they demo well. They aren't. McKinsey's 2025 State of AI in Enterprise tracks how quickly those abstraction layers get commoditized as open-source equivalents catch up — a moat with a very short half-life. You cannot underwrite an enterprise valuation on something a competitor can replicate from a public repo in a quarter.

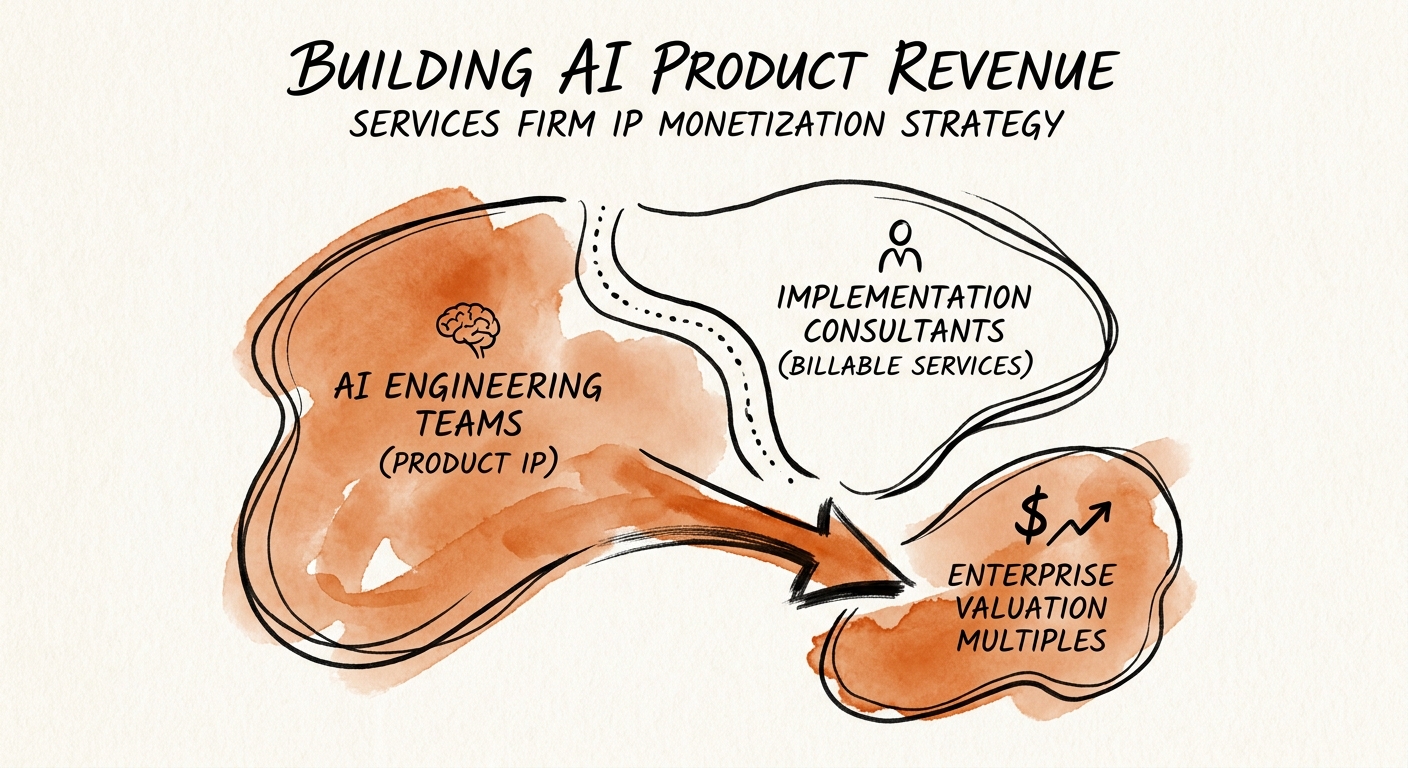

What you actually own — the thing no one else can copy — is sitting in your delivery history. If your team has run two hundred complex ERP migrations in manufacturing, the asset isn't a chat interface. It's the schema-mapping logic, the library of error resolutions you've hit and fixed, the migration sequencing that keeps a plant running through cutover. That's proprietary data gravity, and it's defensible precisely because it's specific to work you've already shipped. The job is to extract that repeatable logic out of your engineers' heads and codify it into product — and then enforce one brutal test. If an independent integrator can't deploy your product without your architects on the line, it isn't a product yet. It's an internal tool with a price tag. The operational divide that makes the difference — product engineers who never log a billable hour, separated cleanly from delivery staff — is the same separation that drives the valuation gap dissected in the SAP managed-services valuation breakdown.

What to fix before the next raise or sale

The reward for getting this right is not marginal. PitchBook's Q1 2026 Enterprise Software Valuations shows pure AI software streams — scalable architecture, a real ARR motion, no hidden labor — clearing well into double-digit forward-revenue multiples on that tranche. The penalty for getting it wrong is just as sharp: PwC's 2026 Tech M&A Outlook describes buyers applying a steep discount to product revenue that needs heavy human intervention to deploy or maintain. The spread between those two outcomes, on the same underlying technology, is almost entirely a function of how you've structured the business — not how good the code is.

So treat the AI line as its own company, starting now, while you still have time to make the records clean before anyone audits them. Concretely, four moves matter.

Give the product its own P&L. A standalone entity is ideal; at minimum, a distinctly tracked unit with its own cost of goods sold. When the Quality of Earnings team arrives, you want them reading a pristine software P&L, not reconstructing one.

Get senior architects off product maintenance. Every non-billable hour your best people spend running the product for a client is a data point the buyer uses to reclassify the revenue. Build a product engineering function that doesn't touch delivery.

Stop customizing the core. Hold a firm API boundary and make clients adapt to your architecture. Per-client forks are how a "platform" silently becomes eleven bespoke projects.

Rebuild sales comp. Quota-carrying services reps don't sell consumption-based licenses on instinct. Move that motion to ARR and usage quotas, or accept that you're selling software with a services incentive plan.

The honest framing: scale on the top line means nothing if the margin structure underneath is services wearing a software costume. That's the same point made in why Rule of 40 misleads services firms — growth without structural margin integrity is vanity, and buyers see through it in an afternoon. Build the product so it can stand without you, fence off the financials, and let the market value you as a software creator instead of a busy agency with an interesting side project.