BRIEF · EXIT READINESS

Two Atlassian Partners, Same Logo, Triple the Multiple: What Buyers Pay For in 2026

Two Atlassian partners can look identical and trade three multiple-turns apart. The 2026 diagnostic PE buyers run on service mix, Jira Align, and migration proof.

14x Top-Decile EBITDA Multiple

BRIEF · EXIT READINESS

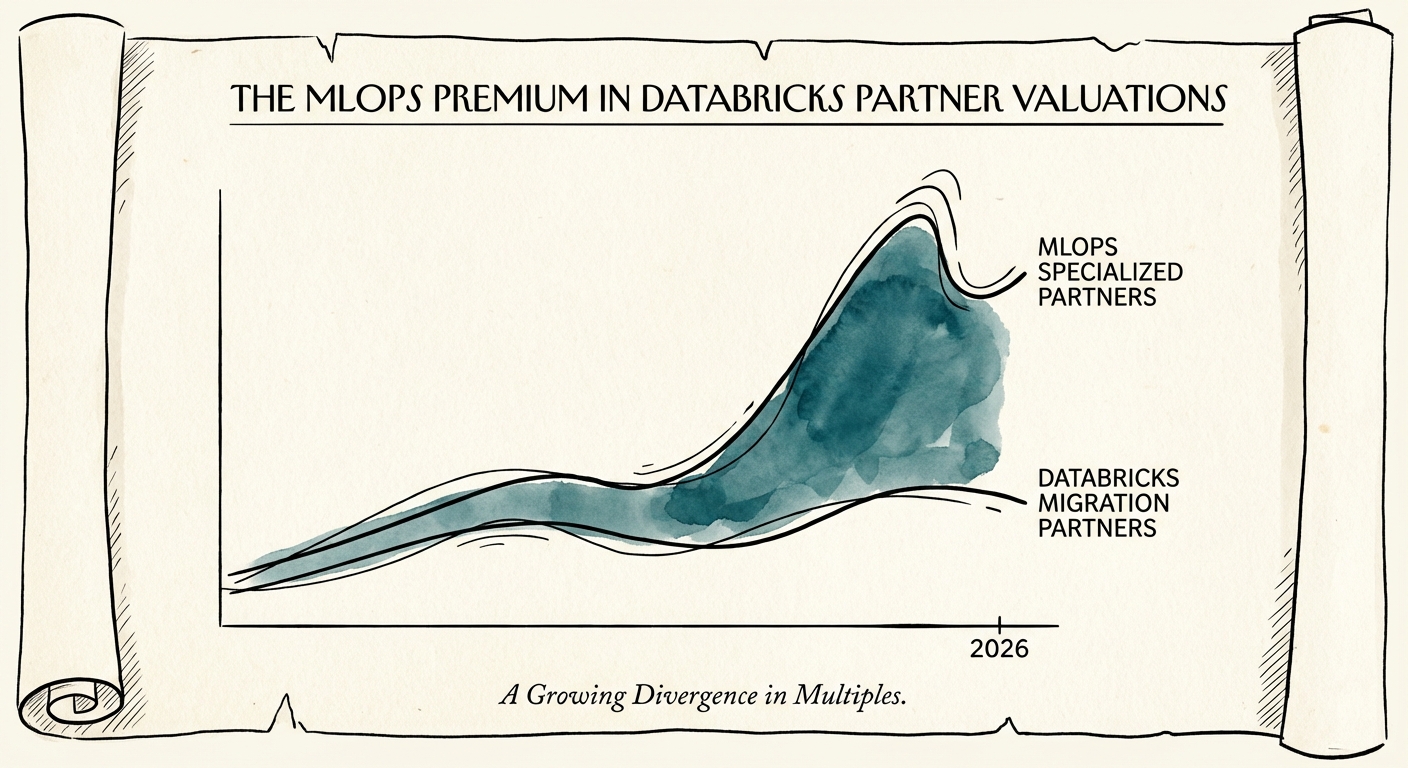

The MLOps Premium: Why Databricks Partners with Model Ops DNA Trade at 14x

Why Databricks partners with MLOps and GenAI capabilities trade at 14x EBITDA while generalist migration shops stall at 8x. A 2026 valuation diagnostic for PE sponsors.

14x EBITDA Multiple for MLOps Specialists

BRIEF · EXIT READINESS

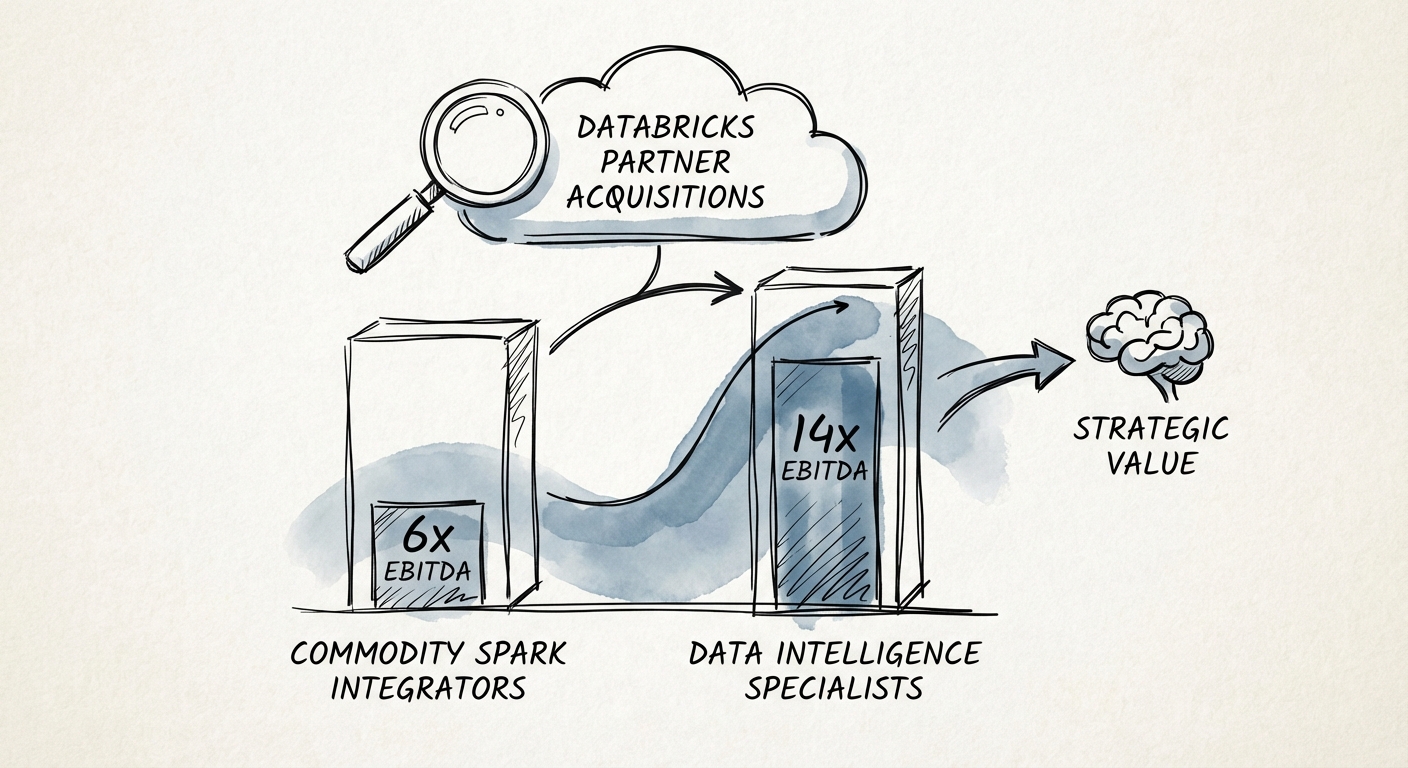

How PE Firms Evaluate Databricks Partner Acquisitions: The 2026 Diagnostic

A private equity due diligence framework for valuing Databricks partners. Analysis of the 14x premium for 'Data Intelligence' firms vs. the 6x commodity multiple for Spark integrators.

Premium EBITDA Multiple for 'AI-Native' Databricks Partners

BRIEF · EXIT READINESS

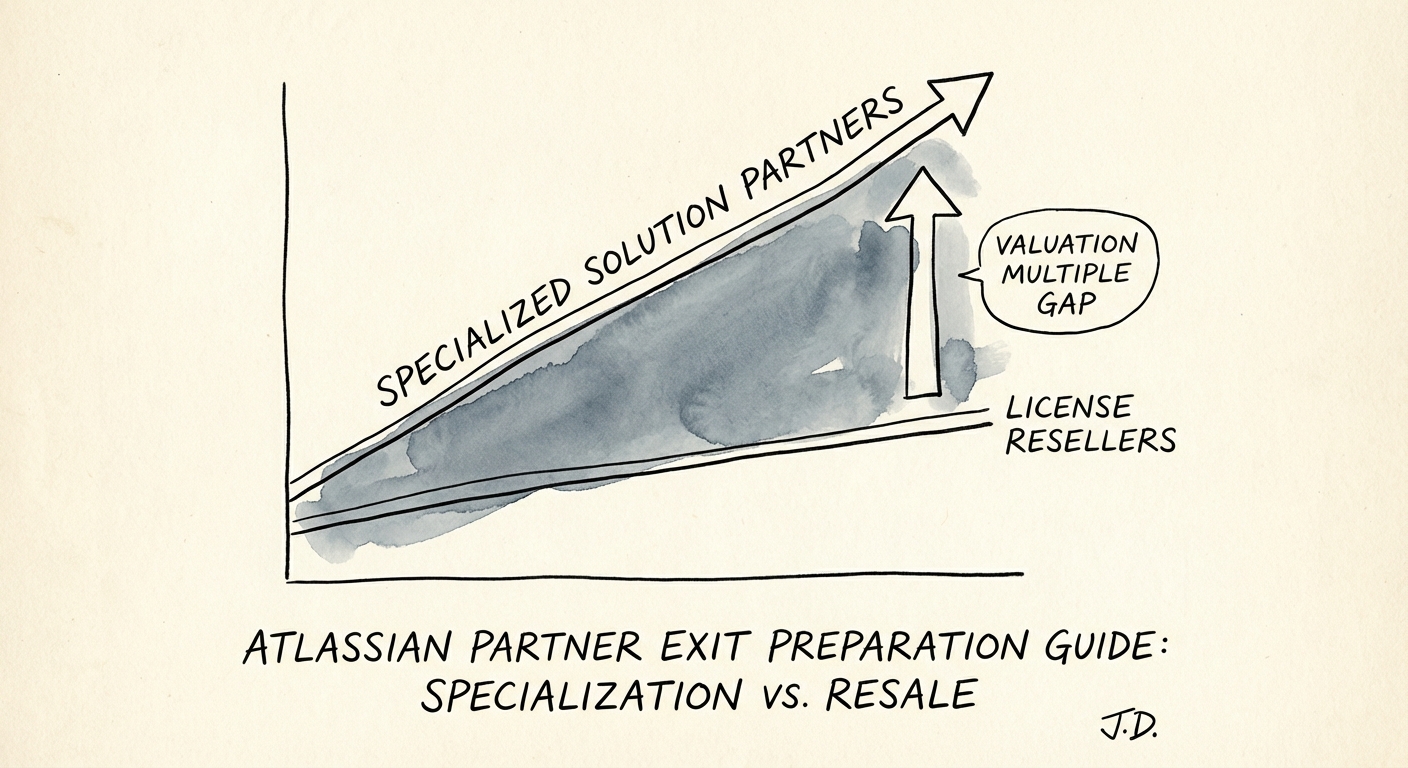

Selling an Atlassian Partner in 2026: Why Two Firms With the Same Revenue Sell for 6x and 12x

Two Atlassian partners, same revenue, double the multiple. What buyers pay for in 2026: services mix, Marketplace IP, and a clean Cloud migration story.

12x Target EBITDA Multiple

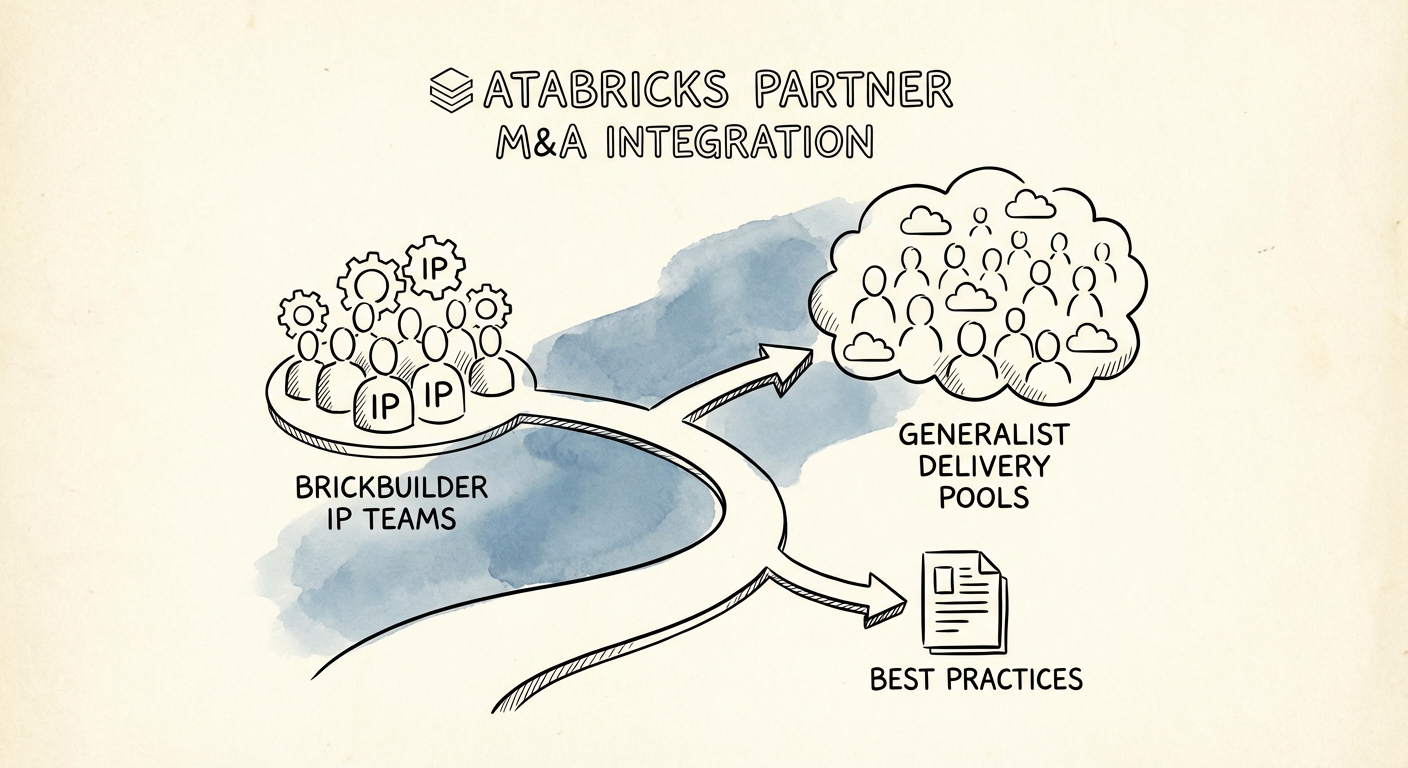

BRIEF · MIGRATION & INTEGRATION

The Databricks Partner Integration Playbook: Preventing the 'Brain Drain' That Kills Deal Value

A post-merger integration playbook for Private Equity firms acquiring Databricks partners. How to preserve 'Brickbuilder' IP, retain data talent, and maintain Elite status.

35% Year 1 Talent Attrition Rate (Unmanaged)

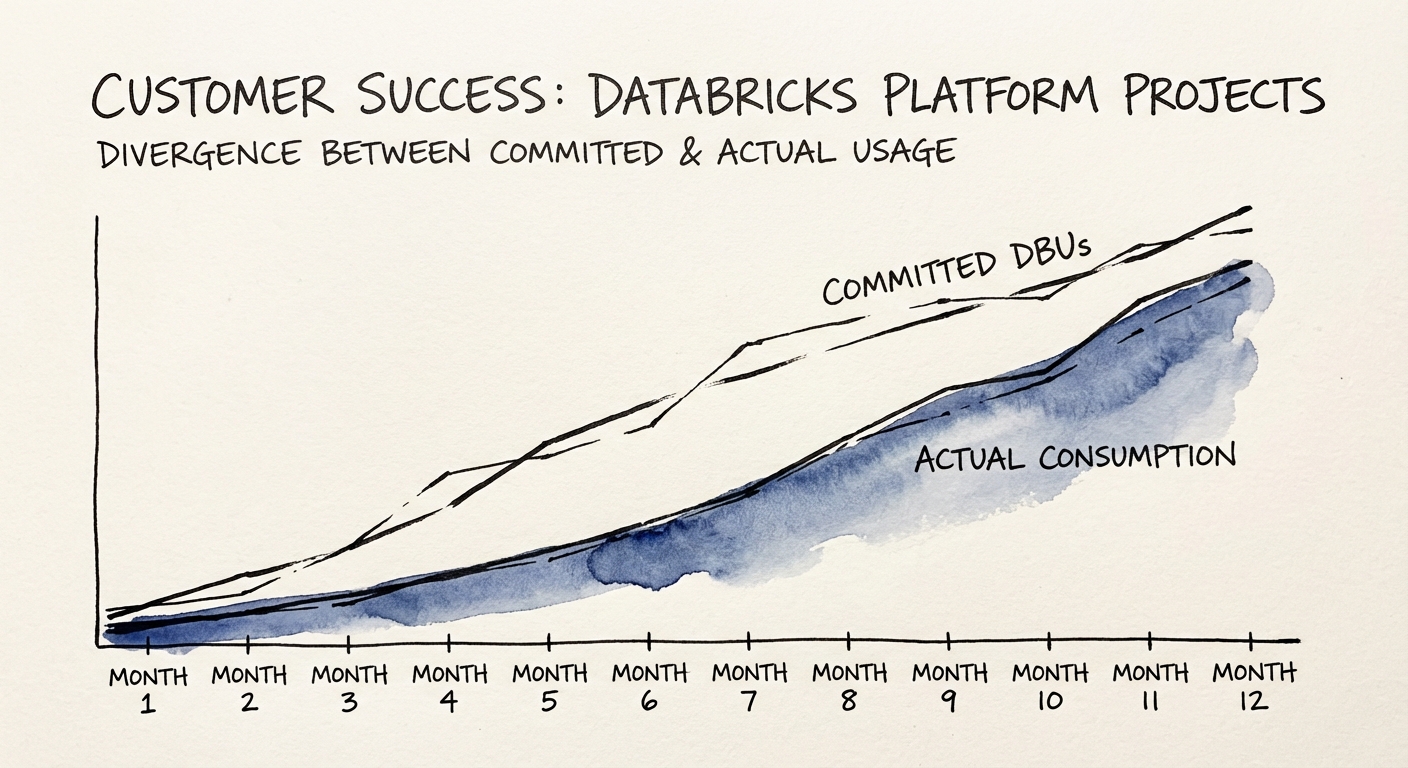

BRIEF · PROCESS DOCUMENTATION

The Databricks Consumption Gap: Why Your 'Live' Platform Is a Business Failure

Is your Databricks platform technically live but commercially dead? Learn why 58% of DBU commitments go unused and how to fix the 'Consumption Gap' with process engineering.

58% Average Year 1 DBU Consumption Gap

BRIEF · GTM EXECUTION

The Atlassian AI Premium: Why 'Rovo Ready' Partners Trade at 12x (And Generalists Stall at 6x)

Why Atlassian Partners specialized in Rovo and AI governance trade at 12x EBITDA while generalists stall at 6x. A diagnostic guide for pivoting to AI services.

12x EBITDA Valuation

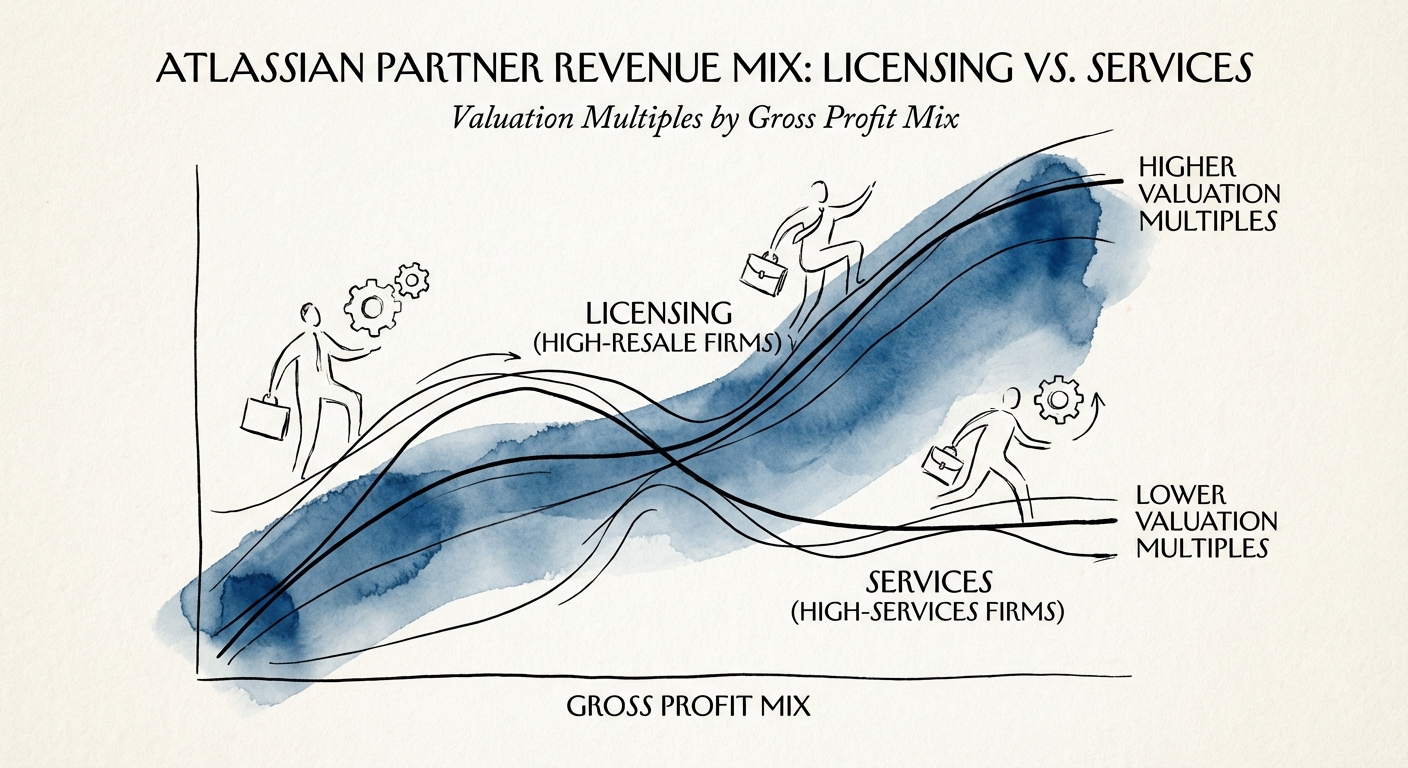

BRIEF · UNIT ECONOMICS

The Atlassian Partner "Margin Mirage": Why High-Revenue Resellers Trade at a Discount

Are you a 'Reseller' or a 'Strategic Partner'? Why Atlassian partners with >50% Services Gross Profit trade at 12x multiples while resale-heavy firms stall at 5x.

50/50 Ideal Gross Profit Mix (Services vs. License)

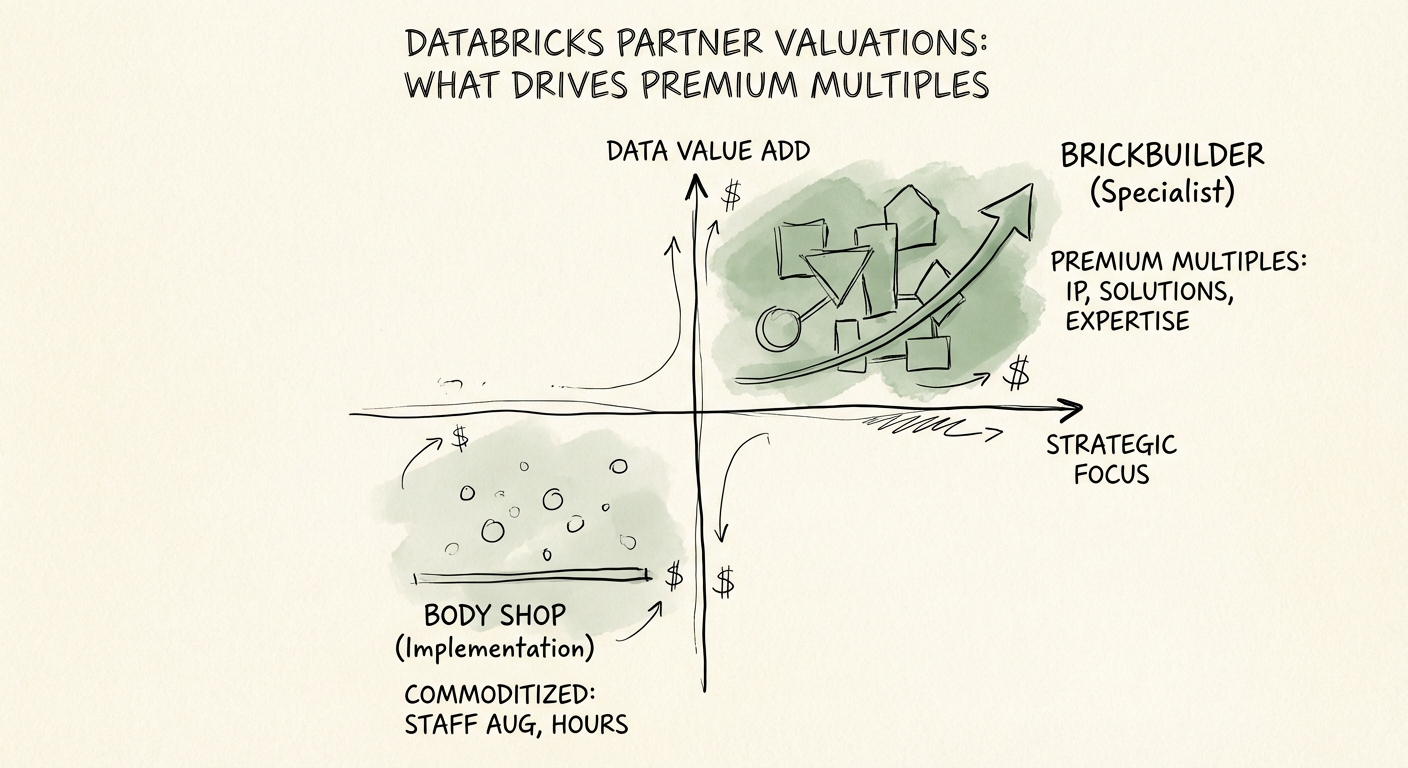

BRIEF · UNIT ECONOMICS

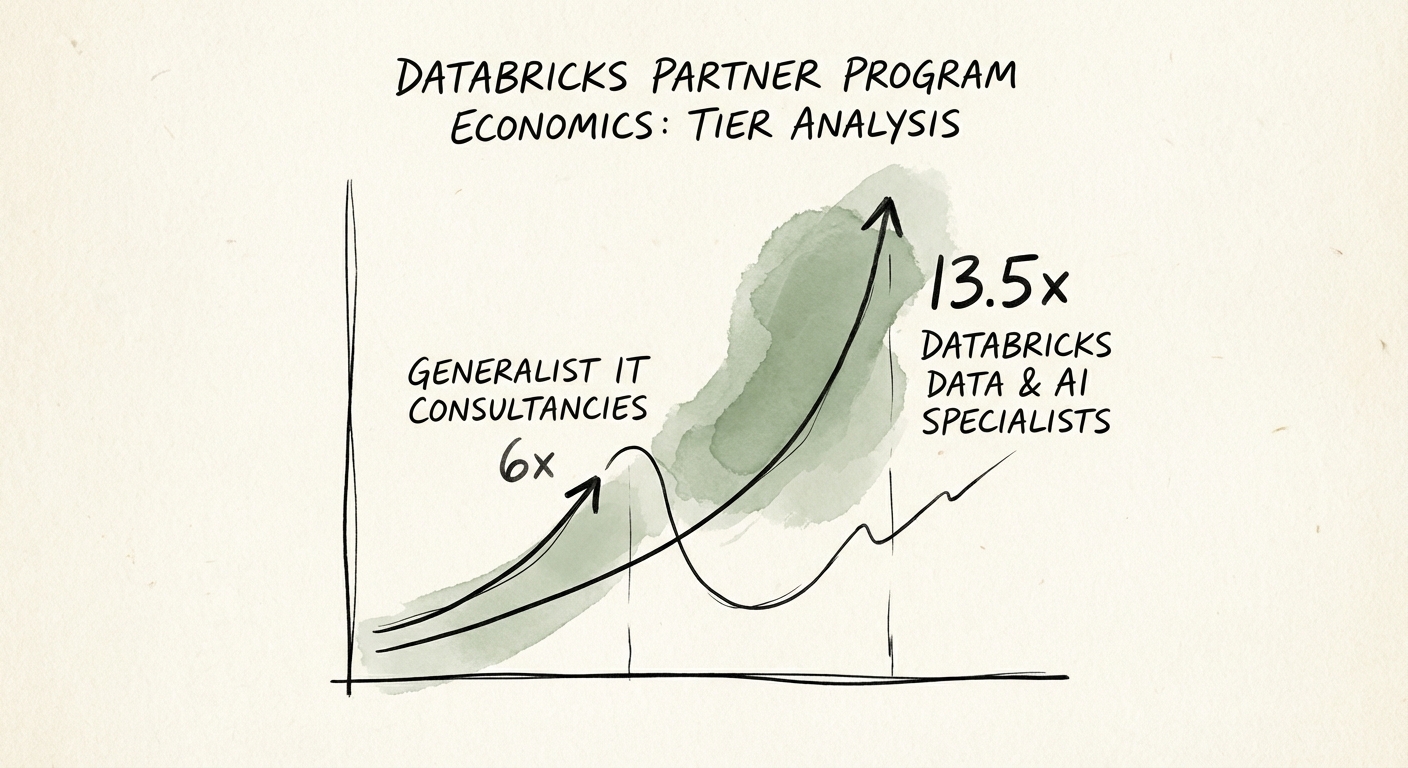

Databricks Partner Economics: The ROI of 'Elite' Status

Analysis of Databricks partner program economics for 2026. Why 'Elite' status costs $400k+ in soft costs and how specialized Data & AI firms trade at 13.5x EBITDA.

13.5x Specialist EBITDA Multiple

BRIEF · FOUNDER EXTRACTION

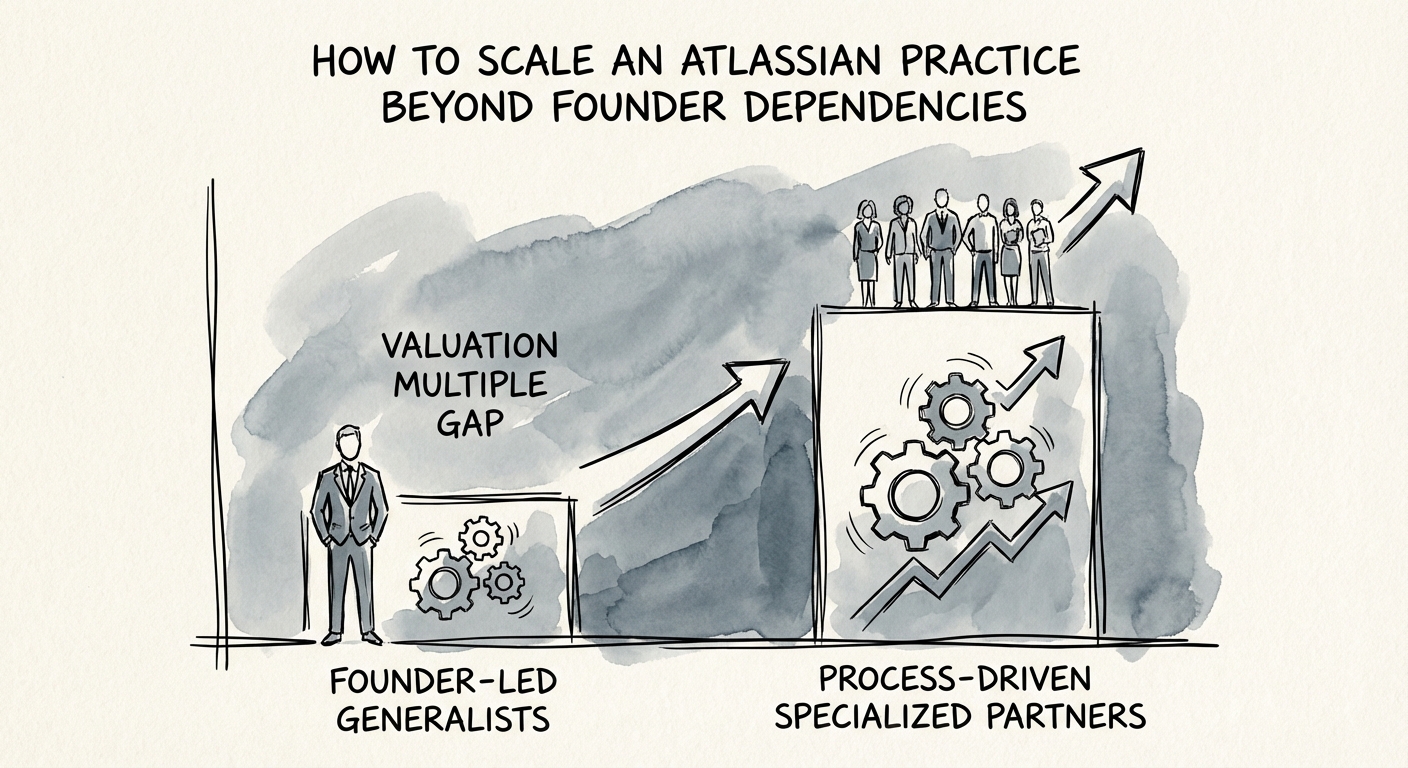

The $10M Wall: How to Scale Your Atlassian Practice Beyond Founder 'Heroics'

Founders of Atlassian practices often hit a revenue ceiling at $5M-$10M. Learn how to extract yourself from sales and delivery to avoid the 30% valuation haircut and scale to a premium exit.

30% Valuation Haircut for Founder Dependency

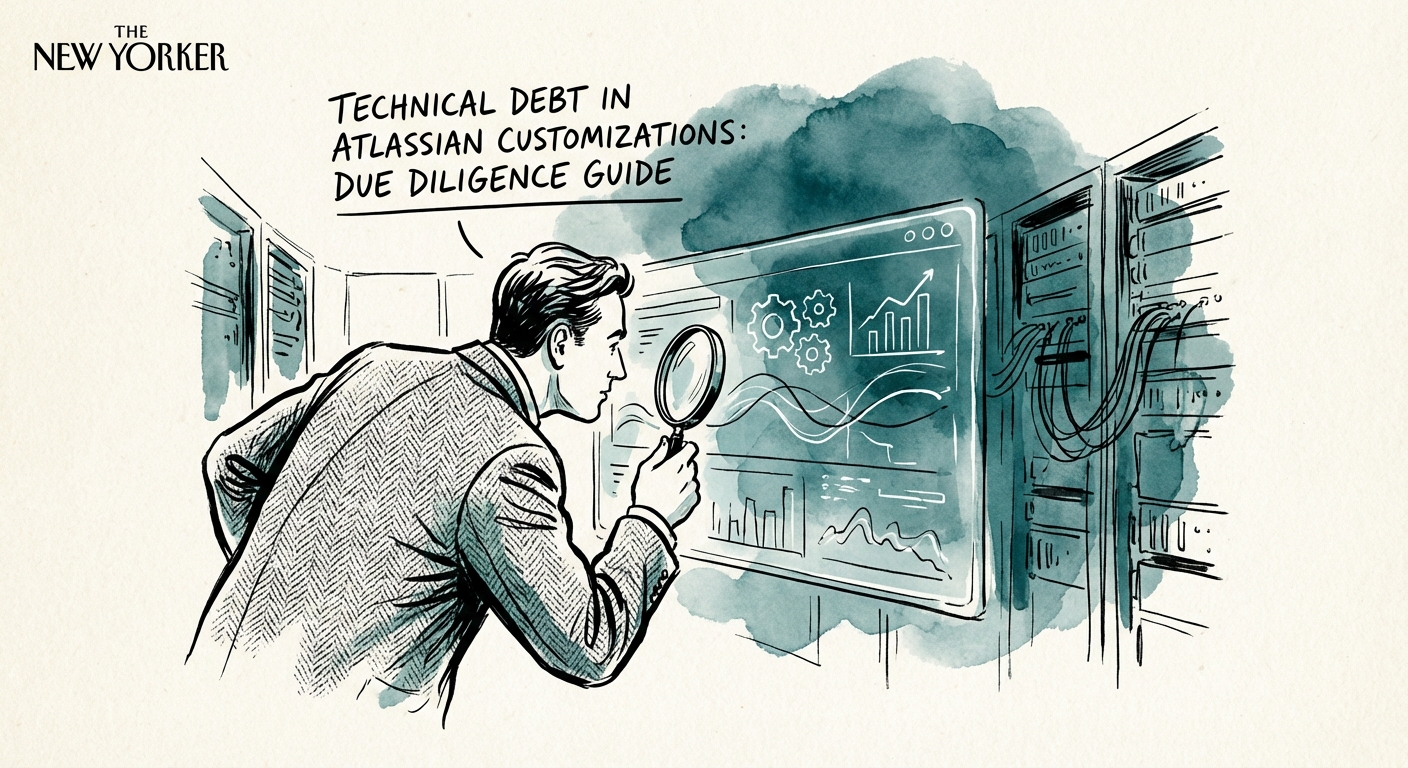

BRIEF · TECHNICAL DEBT

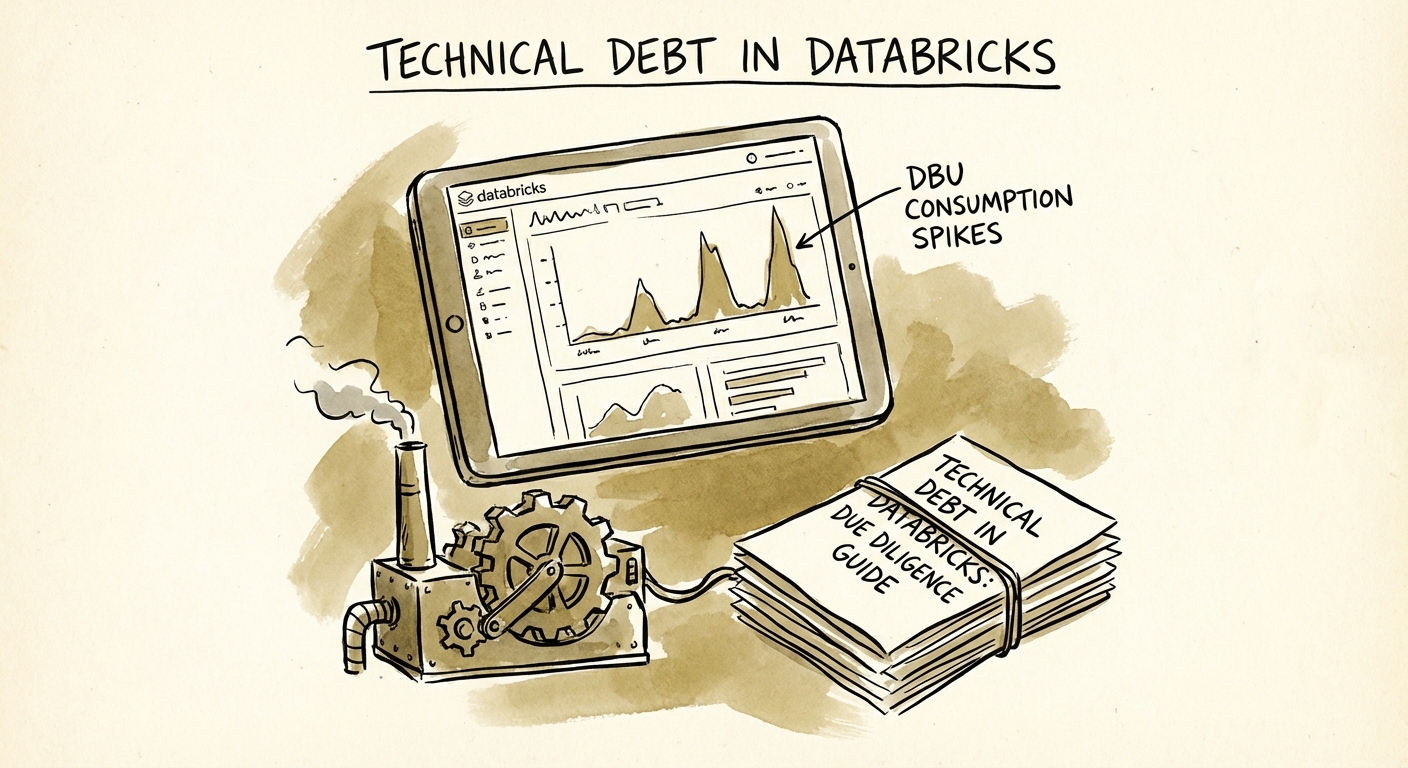

Technical Debt in Databricks Implementations: Due Diligence Guide

Why 15-20% of your target's Databricks bill can be waste. A due diligence guide for Private Equity sponsors to identify technical debt, legacy metastores, and DBU bleed.

15-20% Idle Cluster Waste

BRIEF · EXIT READINESS

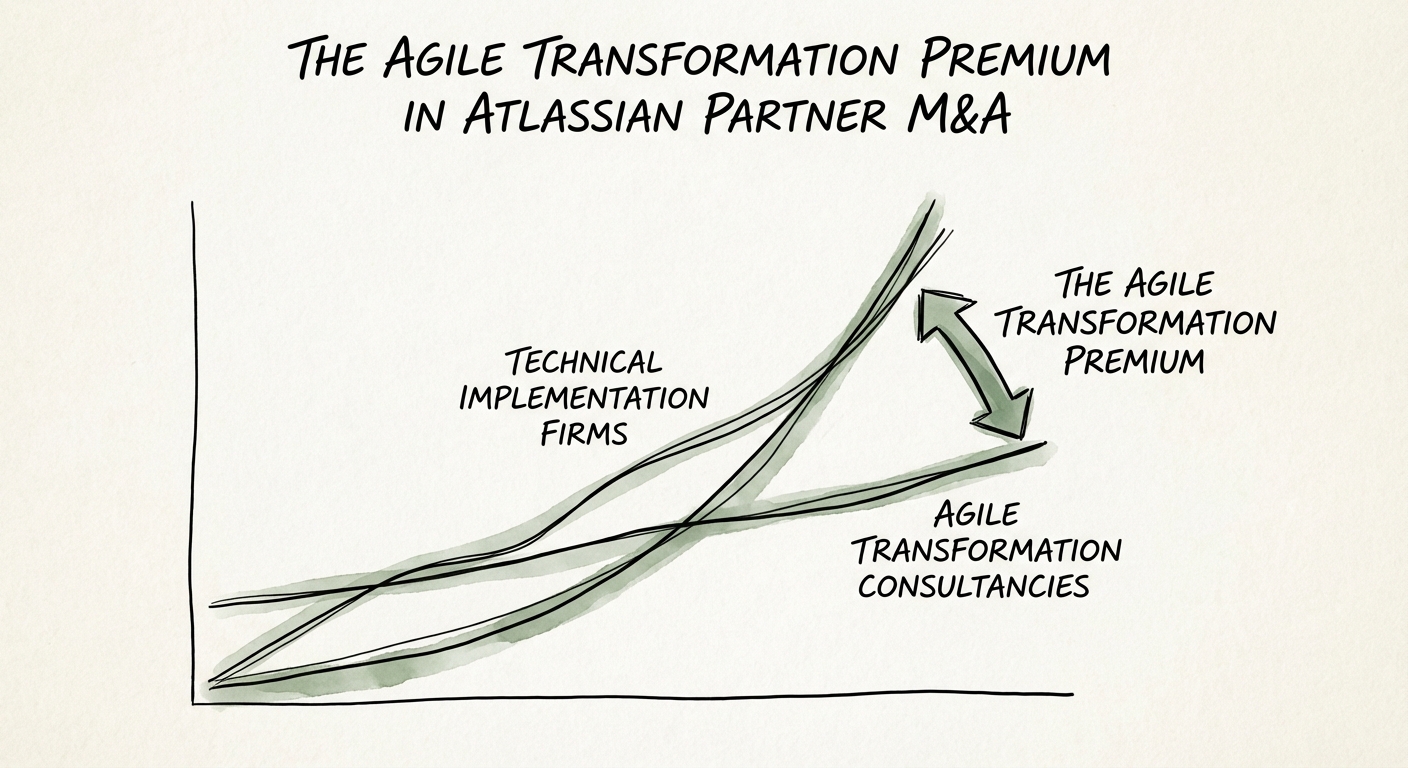

The Agile Transformation Premium: Why Atlassian Partners Trade at 12x (And Tool Shops Stall at 6x)

Why Atlassian partners focused on Agile transformation trade at 12x EBITDA while 'tool shops' stall at 6x. A diagnostic for founders and PE sponsors.

12x Target EBITDA Multiple

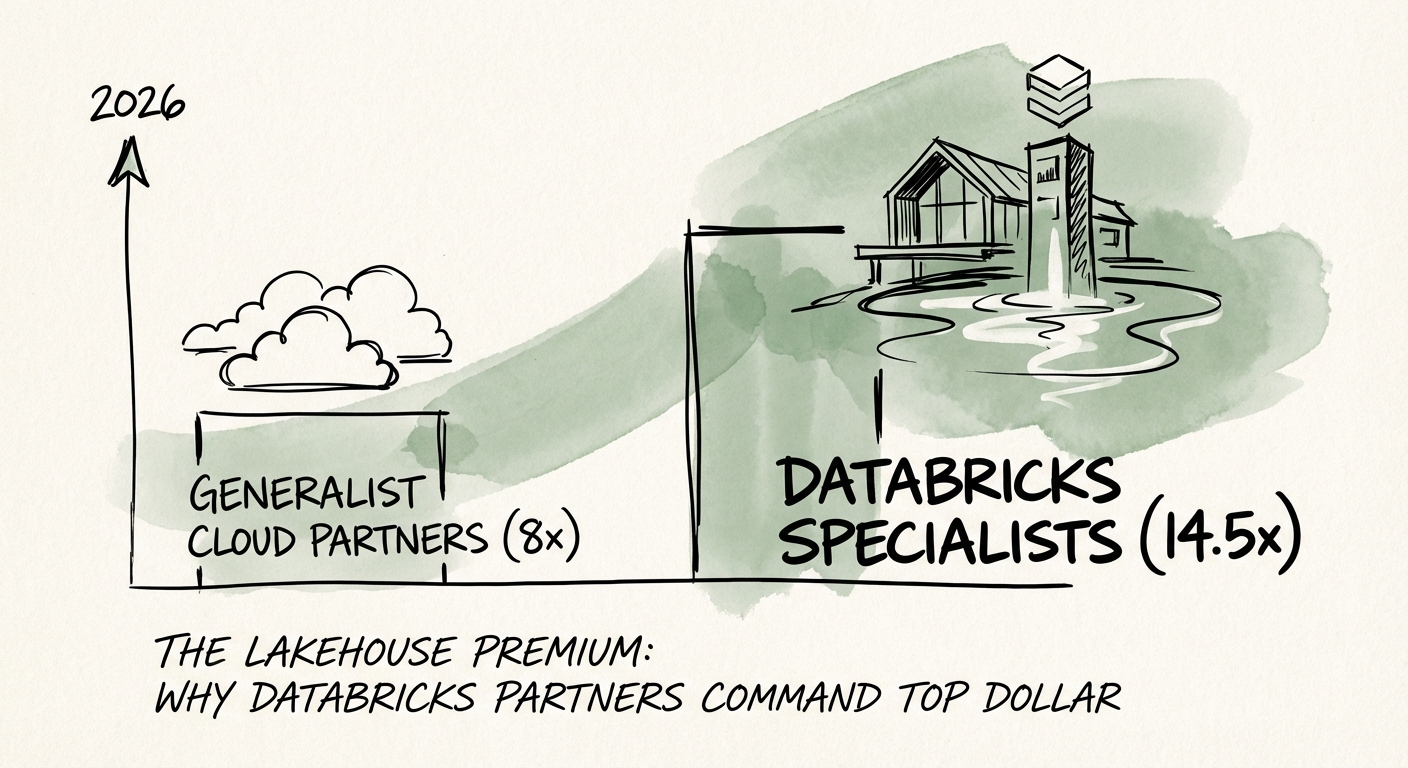

BRIEF · EXIT READINESS

The Lakehouse Premium: Why Databricks Specialists Trade at 14.5x While Generalists Stall at 8x

Why specialized Databricks partners trade at 14.5x EBITDA while generalist cloud firms stall at 8x. A guide for PE sponsors and founders on the Lakehouse Premium.

14.5x EBITDA Multiple

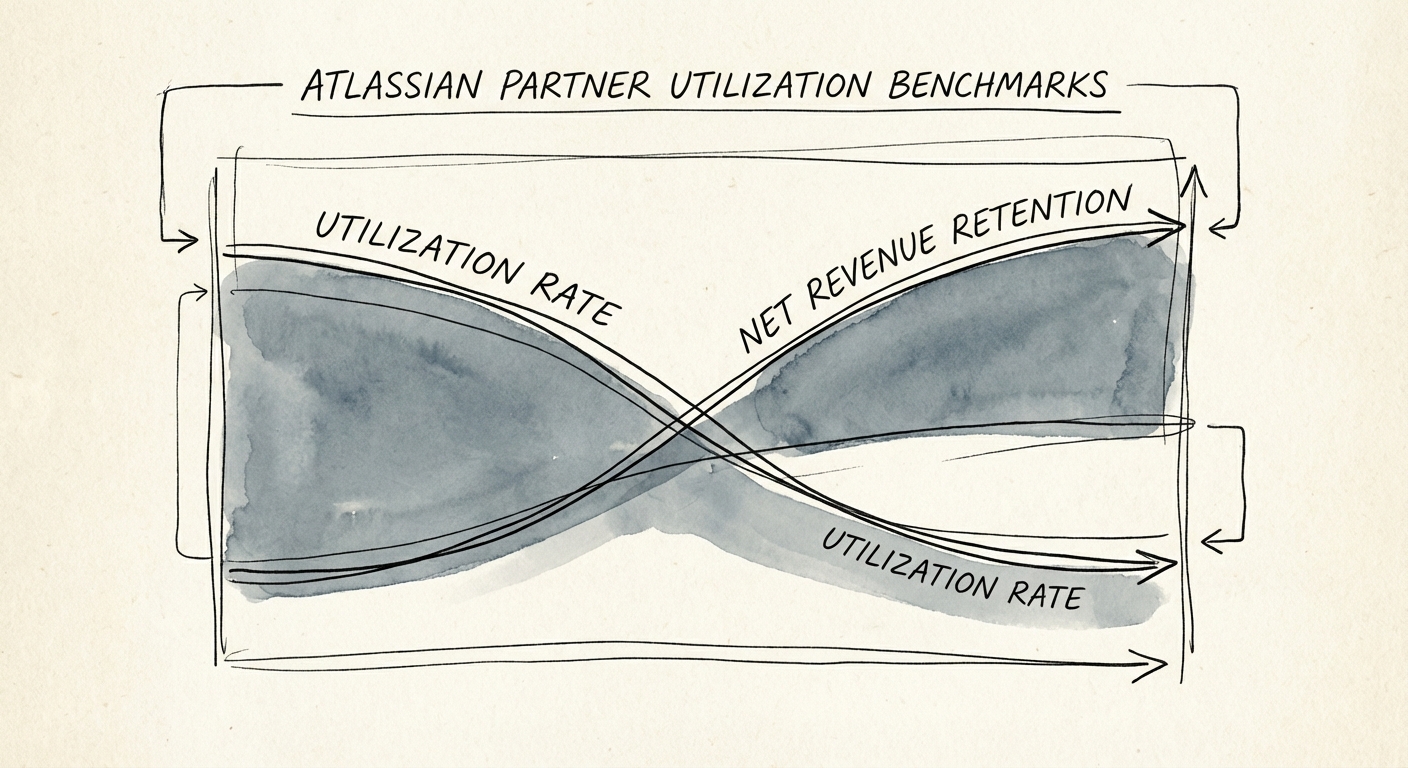

BRIEF · UNIT ECONOMICS

Atlassian Partner Utilization Benchmarks: Why 85% Is a Valuation Trap in the 'Cloud First' Era

Why 85% utilization is killing your Atlassian practice valuation. 2026 benchmarks for Gold and Platinum Solution Partners navigating the Cloud Specialization era.

72% Max Sustainable Utilization

BRIEF · EXIT READINESS

Databricks Partner Valuations: Why Two Identical-Looking Firms Sell at 8x and 14x

Two Databricks partners with the same revenue can sell at 8x and 14x EBITDA. The gap is DBU pull-through, Brickbuilder IP, and Agent Bricks proof. Here's the diligence test.

14x Top-Decile EBITDA Multiple

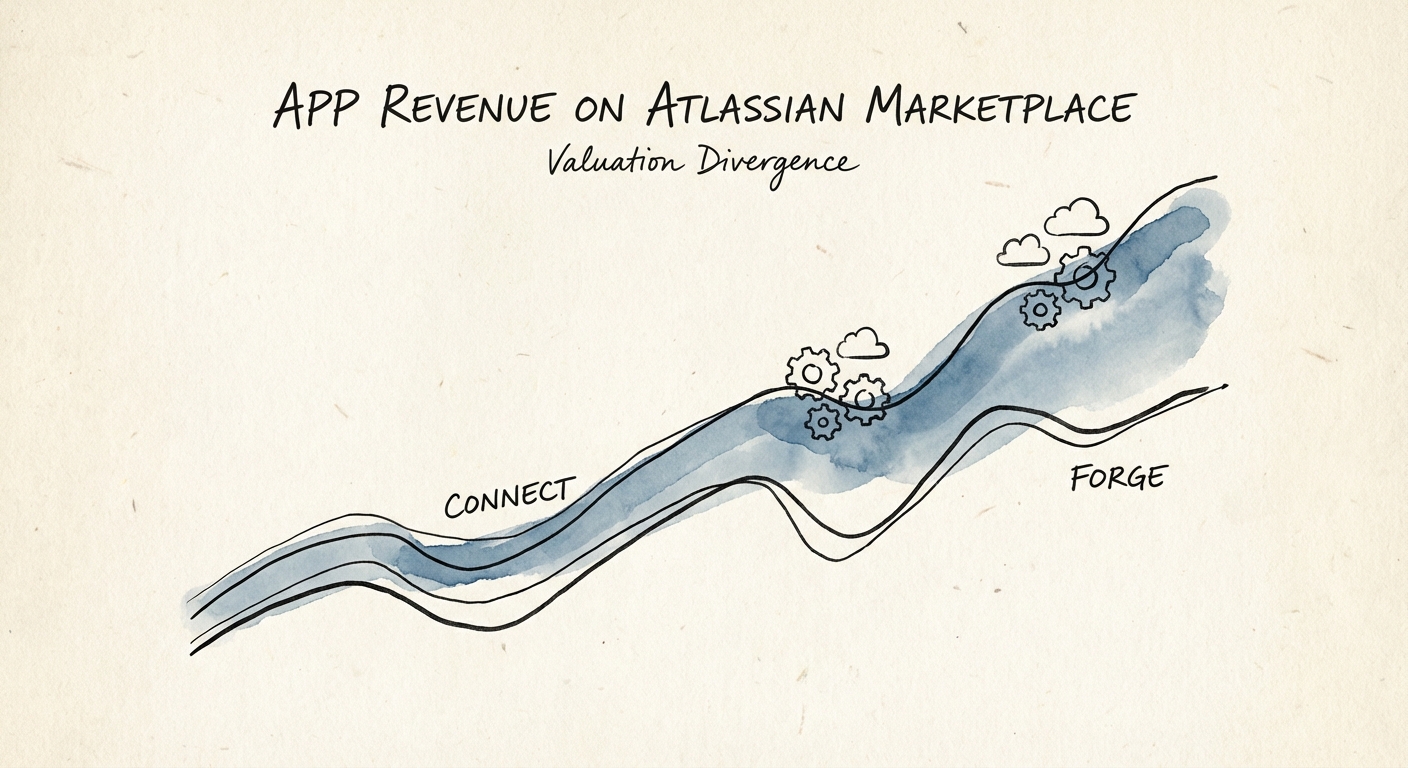

BRIEF · EXIT READINESS

The Atlassian Marketplace Multiplier: Why 'Cloud Fortified' Apps Trade at 12x (And Legacy Connect Apps Stall at 6x)

New 2026 revenue share rules are splitting Atlassian ISV valuations. Learn why 'Cloud Fortified' Forge apps trade at 12x while legacy Connect apps face a 10% margin cliff.

10% Margin Compression

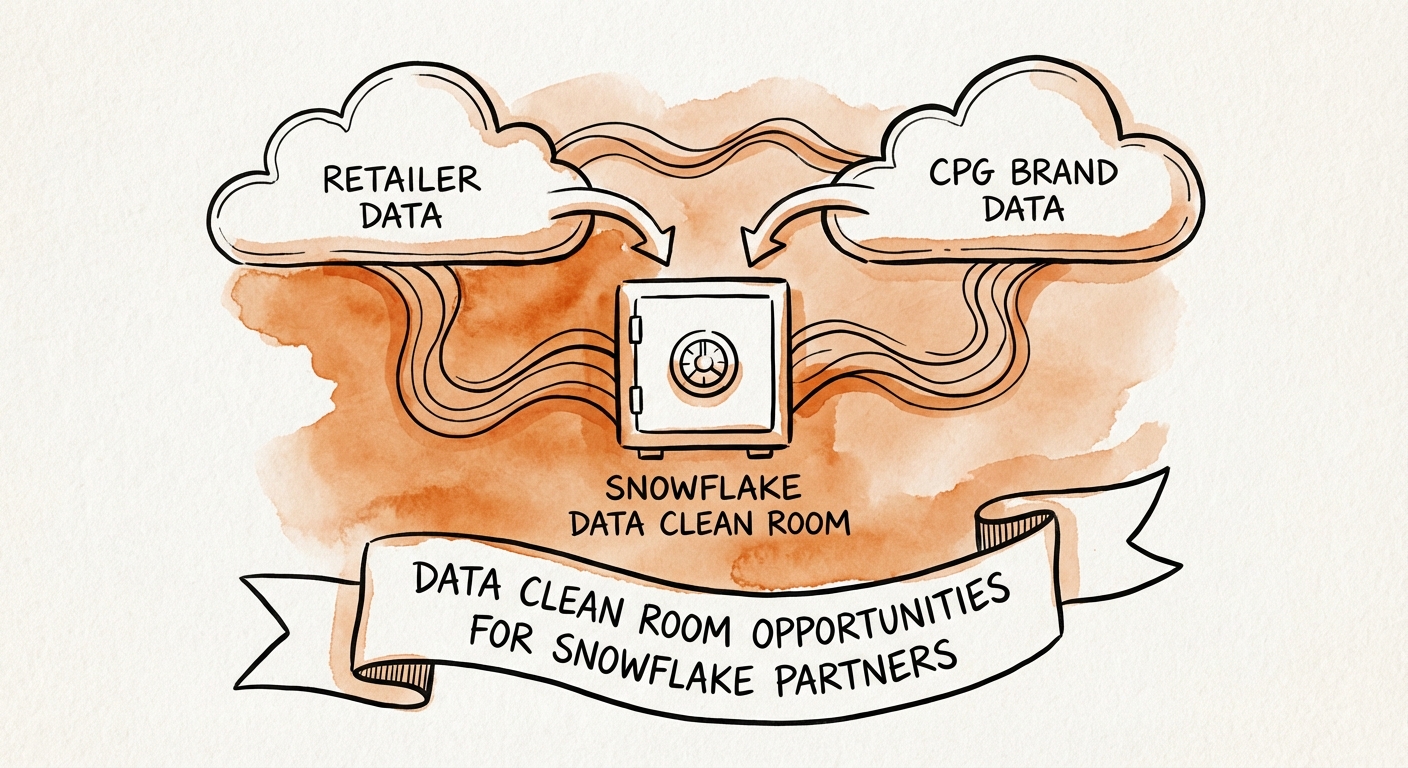

BRIEF · GTM EXECUTION

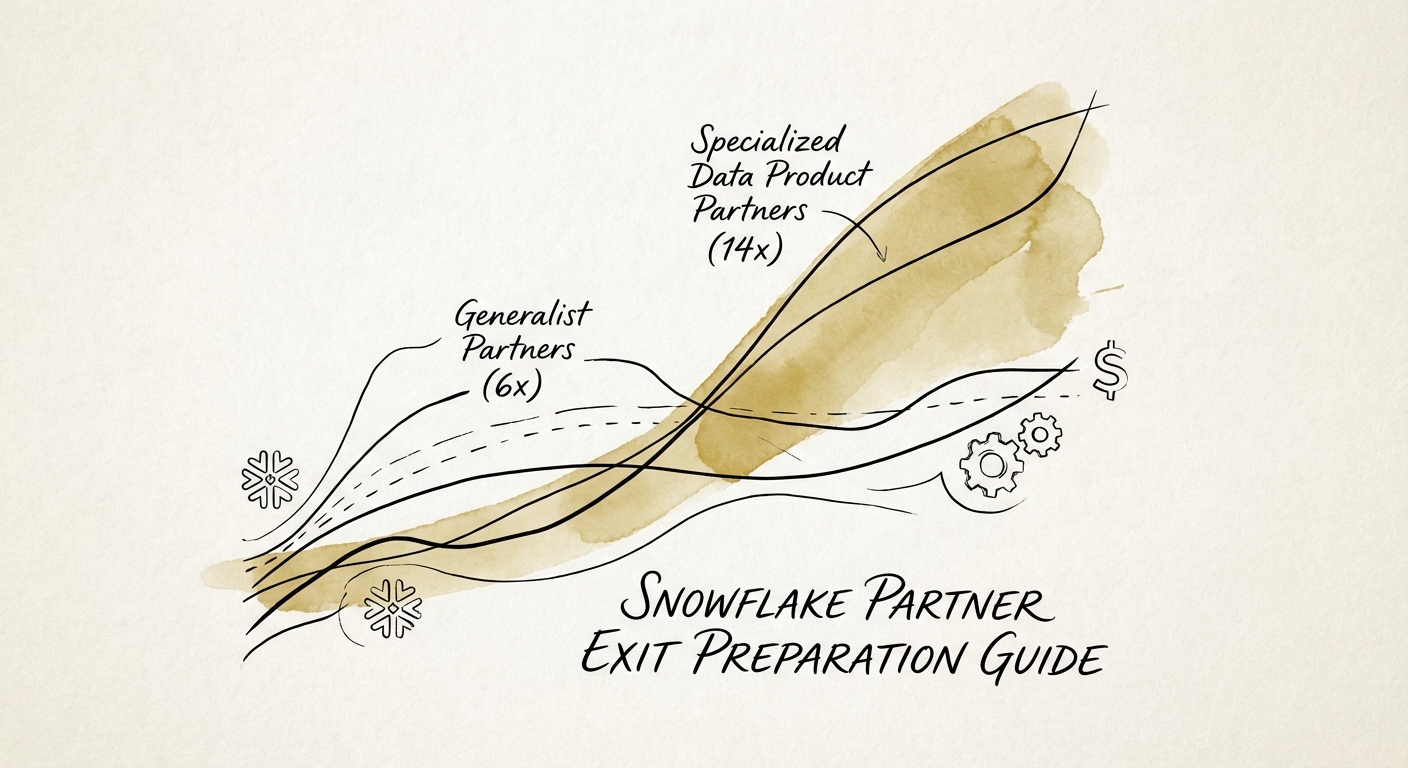

The Data Clean Room Premium: Why Snowflake Partners Are Trading "Body Shop" Rates for IP Multiples

Generalist Snowflake partners are stalling at 6x EBITDA while Data Clean Room specialists command 14x. Here is the diagnostic guide to pivoting your practice toward the $266B privacy economy.

24% Projected CAGR for Data Clean Room Software (2026-2032)

BRIEF · TEAM & HIRING

Atlassian Partner Talent Strategy: The 'Paper Tiger' Trap in Your Certification Roster

Stop hiring 'paper tigers.' A diagnostic guide for Atlassian Partners on building teams with valid ACP-120 expertise, avoiding badge inflation, and scaling high-margin cloud practices.

50% Valuation Haircut for 'Body Shop' Models

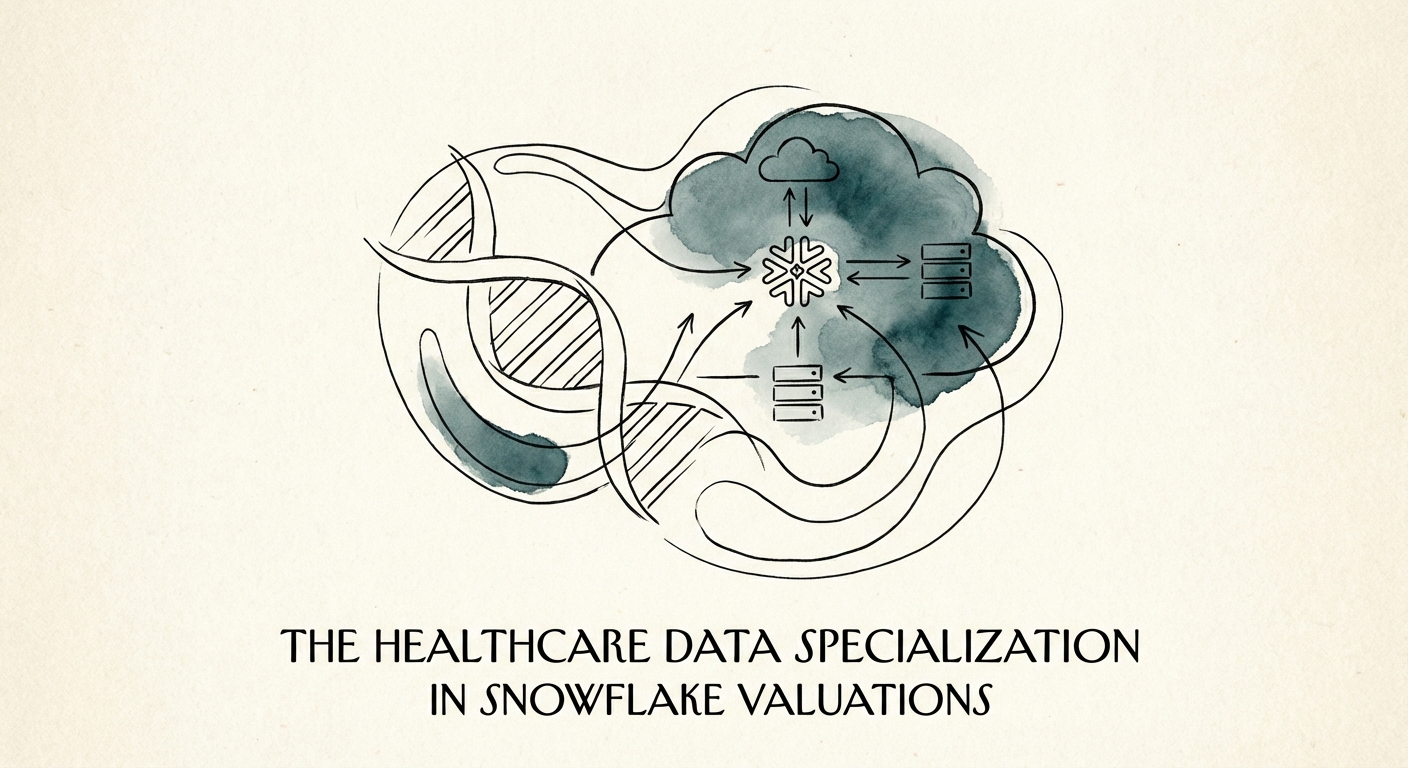

BRIEF · EXIT READINESS

Snowflake Healthcare Data Specialization and Partner Valuation

Healthcare and Life Sciences Snowflake partners can defend a premium when they prove interoperability, compliance, repeatable IP, and vertical delivery depth.

HCLS IP Specialist Valuation Driver

BRIEF · TECHNICAL DEBT

The Atlassian Customization Trap: Why Your Target's "Unique" Jira Workflow Is a $2M Liability

Heavily customized Jira instances are killing M&A deal value. Learn how to quantify technical debt in Atlassian environments (ScriptRunner, Custom Workflows) before signing the LOI.

3.4x Remediation Cost Multiplier

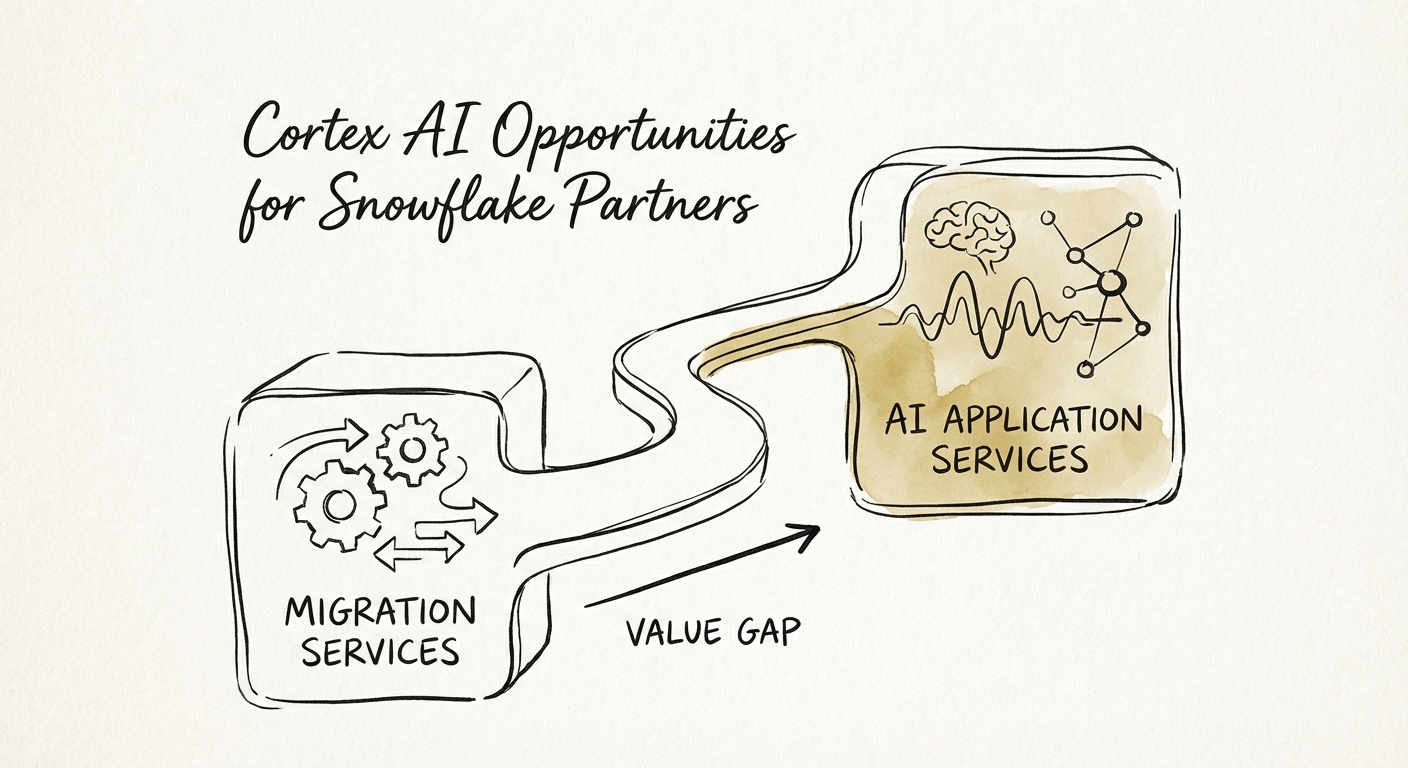

BRIEF · GTM EXECUTION

Snowflake Cortex AI Opportunities for Partners

Snowflake Cortex creates opportunities for partners that can turn governed data into search, analytics, and AI workflows with repeatable vertical IP.

Vertical IP Valuation Driver

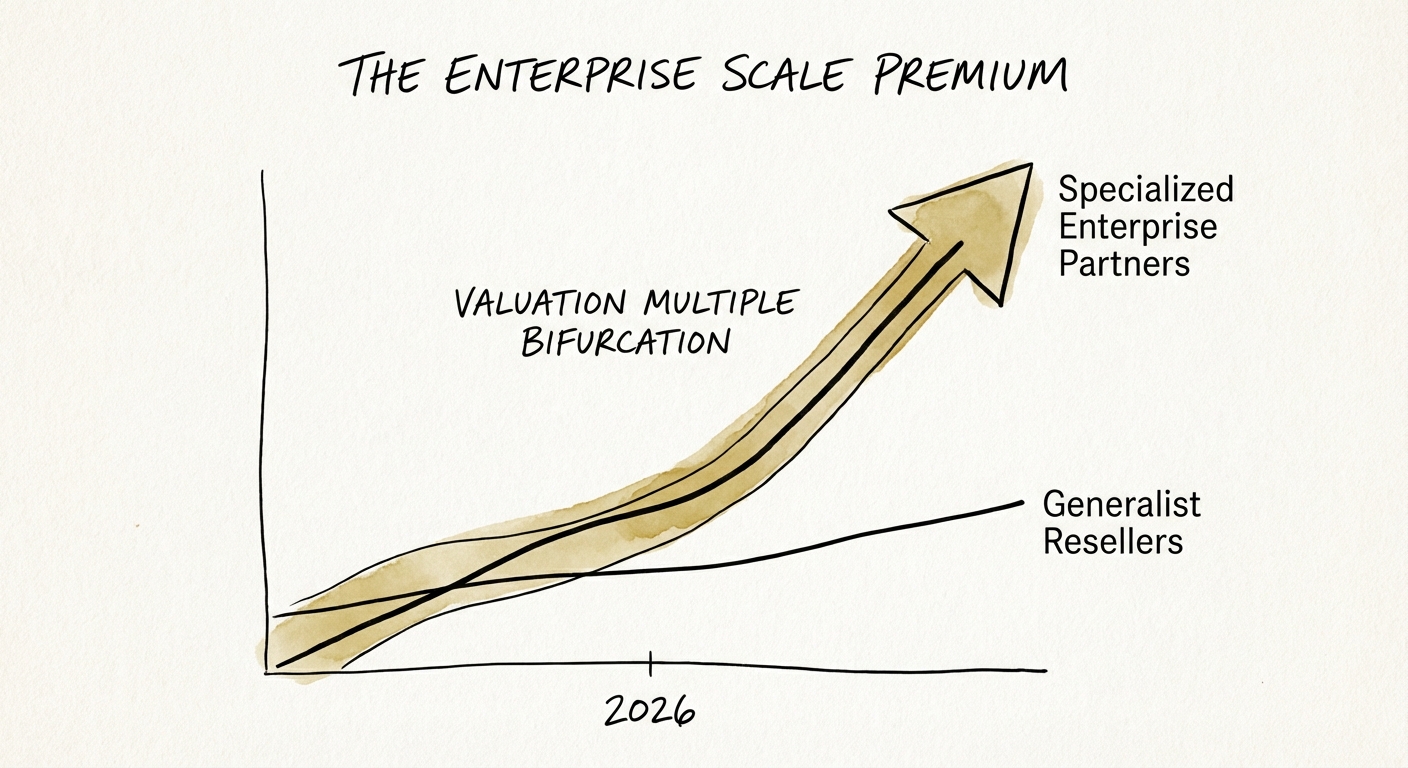

BRIEF · EXIT READINESS

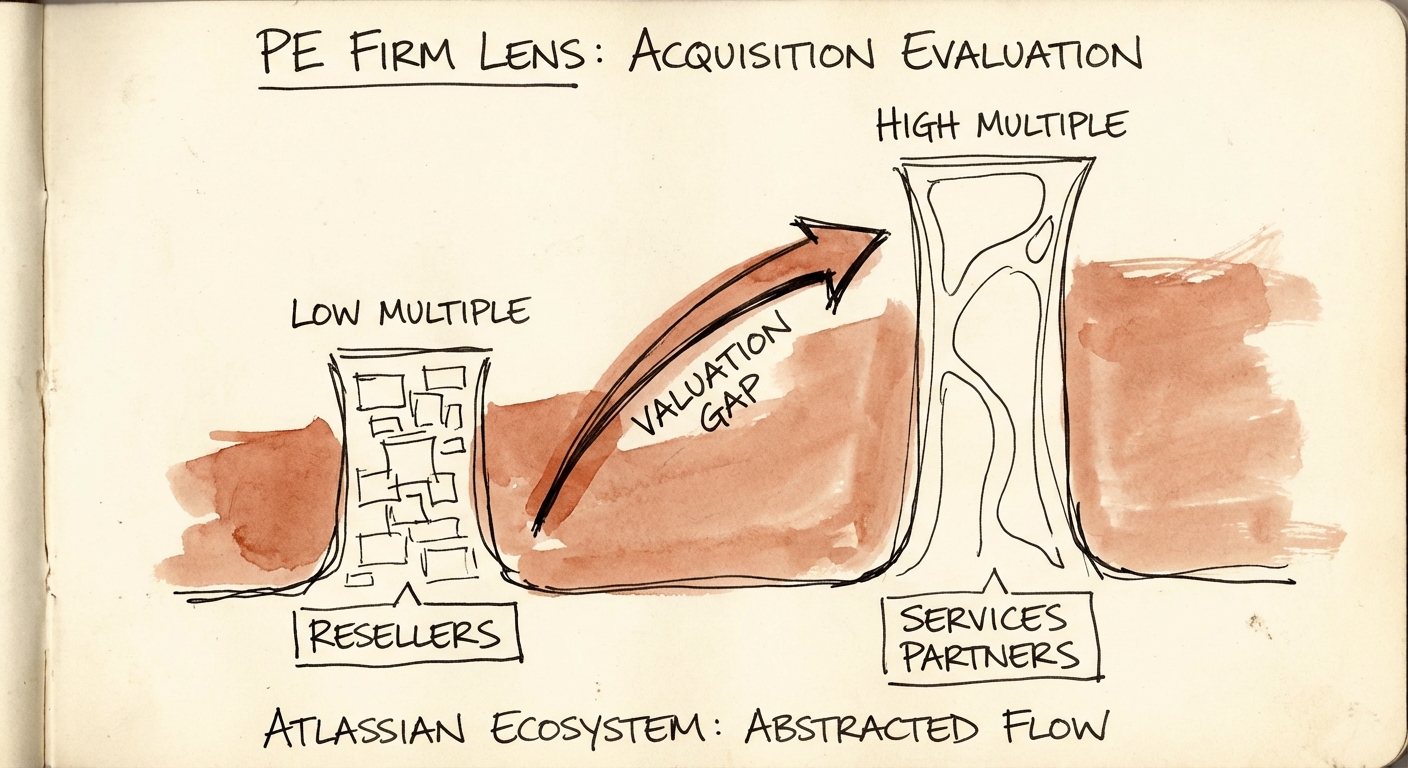

How PE Firms Evaluate Atlassian Partner Acquisitions: The 2026 Diagnostic

Private Equity buyers are scrutinizing Atlassian partners. Learn why resale revenue is valued at 0x, why JSM specialization drives 12x multiples, and how to survive the 2026 due diligence process.

12x vs 4x Valuation Multiple Gap (Services vs. Resale)

BRIEF · EXIT READINESS

Selling a Snowflake Partner Firm: Why "If We Fire You, Does Consumption Drop?" Decides Your Multiple

A PE buyer's first question for a Snowflake partner isn't revenue — it's whether client consumption survives you leaving. Here's how that one test moves you from 6x to 14x.

14x Target EBITDA Multiple

BRIEF · TEAM & HIRING

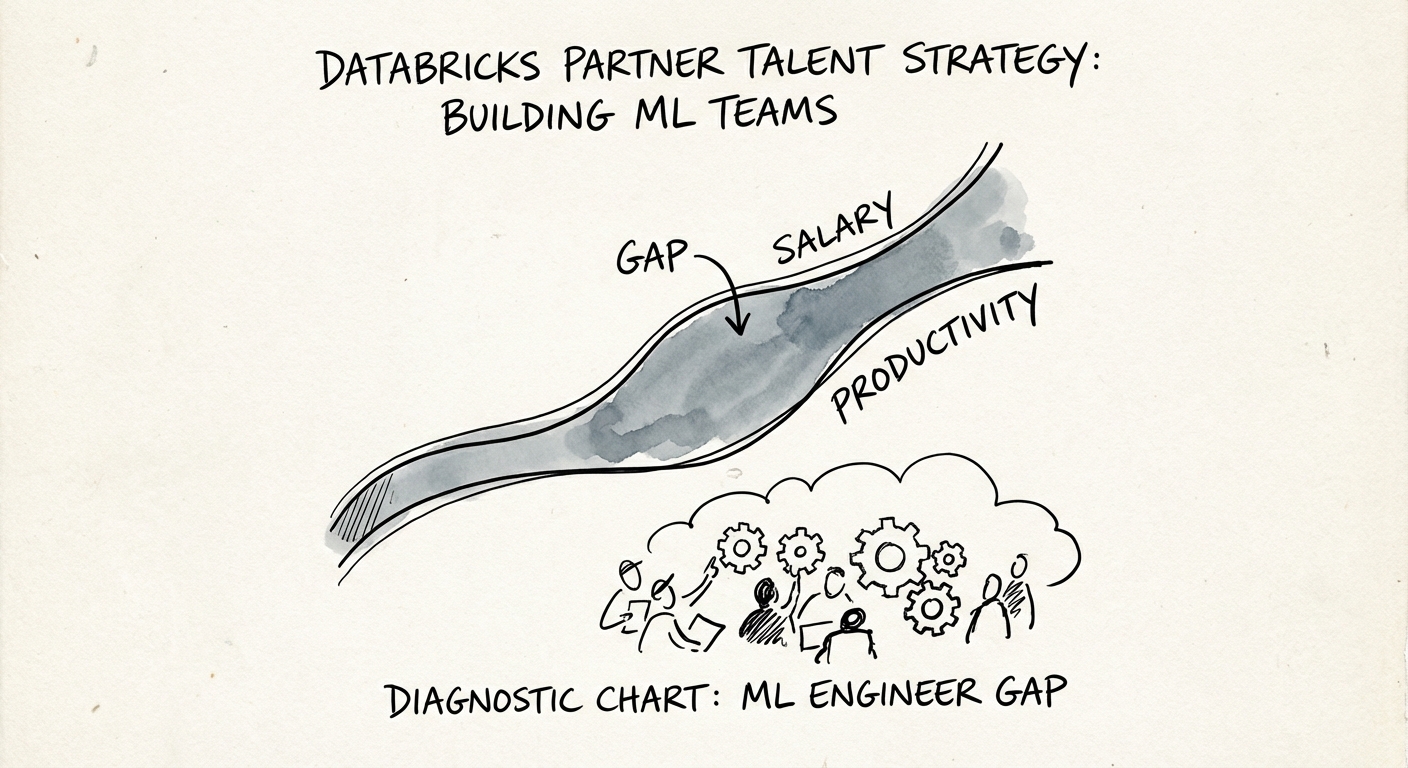

Databricks Partner Talent Strategy: The $250k 'Notebook Engineer' Trap

Benchmarks for Databricks partner talent strategy. Why 'Certified' ML engineers fail in production, salary benchmarks for 2025, and how to fix your hiring funnel.

28% Annual Attrition Rate for AI/ML Talent (2025)