BRIEF · MIGRATION & INTEGRATION

The "Elite" Trap: Why HubSpot Partner Roll-Ups Die in Integration (And How to Fix It)

Don't let your HubSpot partner roll-up fail in integration. A diagnostic playbook for PE investors on valuing, merging, and scaling Elite HubSpot agencies.

38% Deal Value Erosion

BRIEF · EXIT READINESS

How PE Firms Evaluate HubSpot Partner Acquisitions: The RevOps Premium vs. The Agency Discount

A private equity guide to valuing HubSpot partners. Learn why RevOps firms trade at 12x while agencies stall at 5x, and how to spot the 'Elite' tier trap.

12x RevOps Multiple

BRIEF · COMPLIANCE & SECURITY

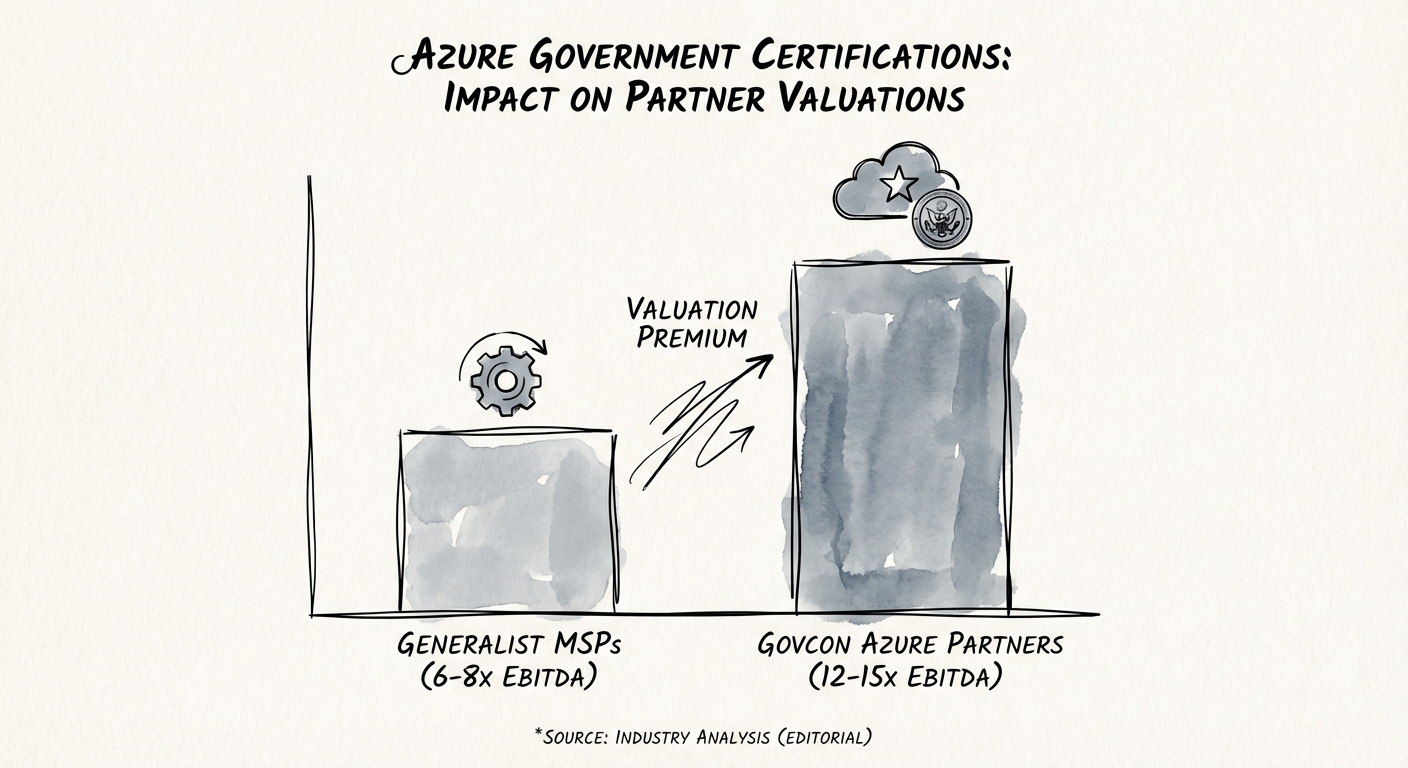

The Sovereign Premium: Why Azure Government Partners Trade at 15x EBITDA

Why Azure Government (IL4/IL5) and FedRAMP authorized partners trade at 15x EBITDA vs. 8x for generalists. A diagnostic guide for PE investors.

15.0x Median GovCon EBITDA Multiple

BRIEF · EXIT READINESS

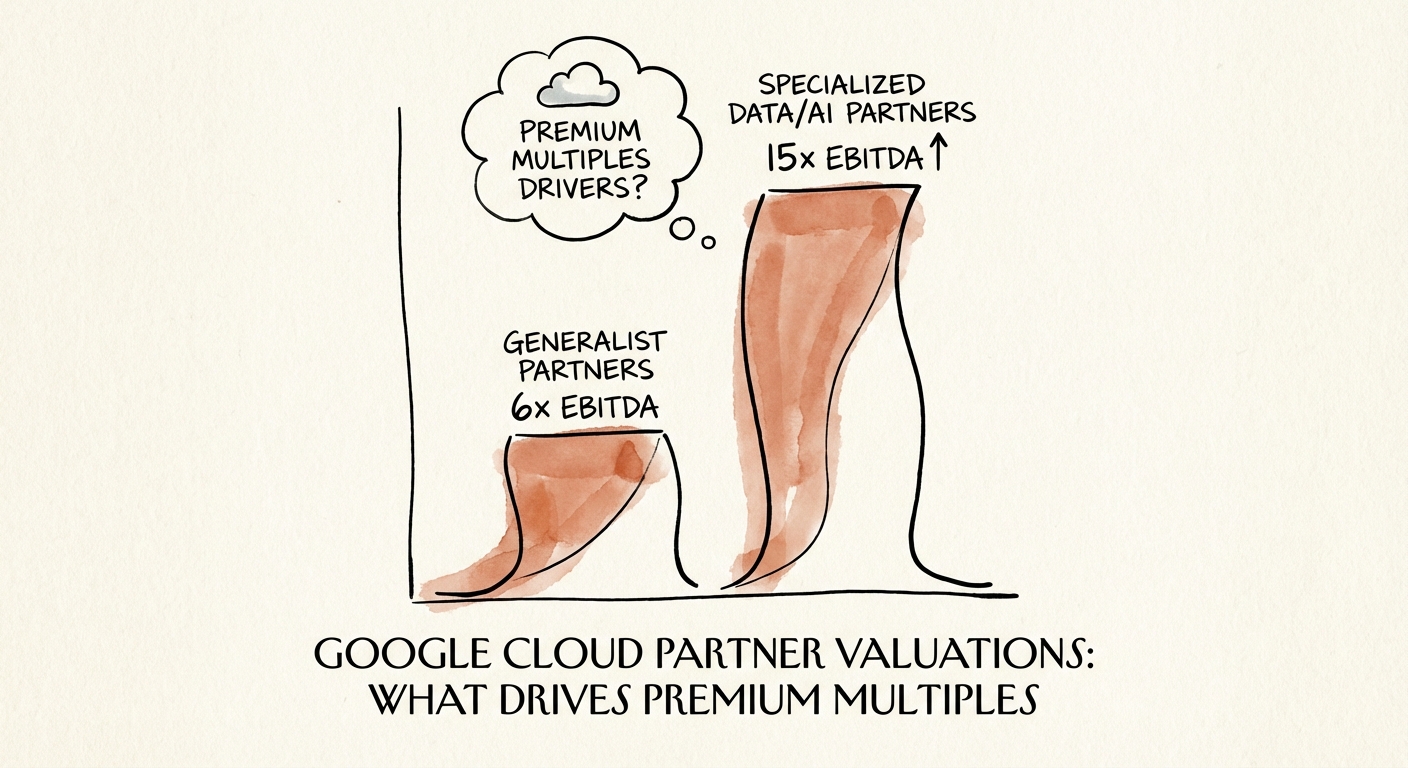

Google Cloud Partner Valuations: The Gap Between 6x and 15x

New data on Google Cloud Partner valuations. Why specialized Data & GenAI firms trade at 12x-15x EBITDA while infrastructure generalists stall at 6x. M&A benchmarks for 2026.

12x-15x Premium EBITDA Multiple

BRIEF · REVENUE ARCHITECTURE

The "Go-Live" Lie: Why HubSpot Practices Leak Value Post-Implementation

Stop optimizing for HubSpot tiers and start optimizing for EBITDA. Learn why 'Sold MRR' is a vanity metric and how to fix the 90-day churn cliff in your implementation practice.

105% Managed Services NRR Target

BRIEF · UNIT ECONOMICS

The HubSpot Tier Trap: Why 'Elite' Status Might Be Killing Your EBITDA

Is reaching HubSpot Elite status worth the cost? We analyze the unit economics, 2025 program changes, and the hidden 'Badge Tax' that erodes agency EBITDA.

26% Average Profit Margin Erosion for Generalist Agencies

BRIEF · EXIT READINESS

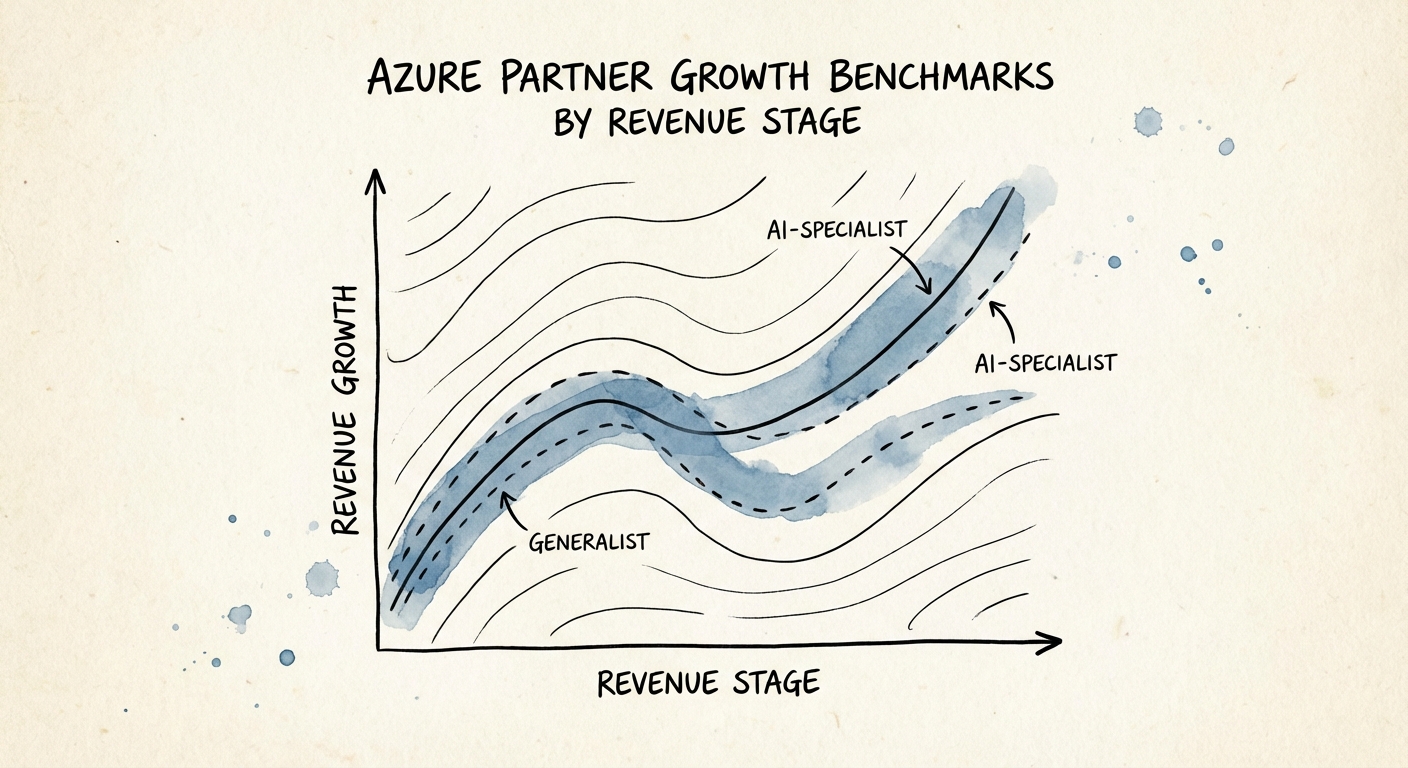

Azure Partner Growth Benchmarks: Why Microsoft Partners Stall at $10M

Azure grew ~33% last year. If your Microsoft practice grew 20%, you lost share. Growth, margin, and valuation benchmarks for partners at $5M, $15M, and $50M.

46% Revenue Growth for AI-Enabled Partners

BRIEF · EXIT READINESS

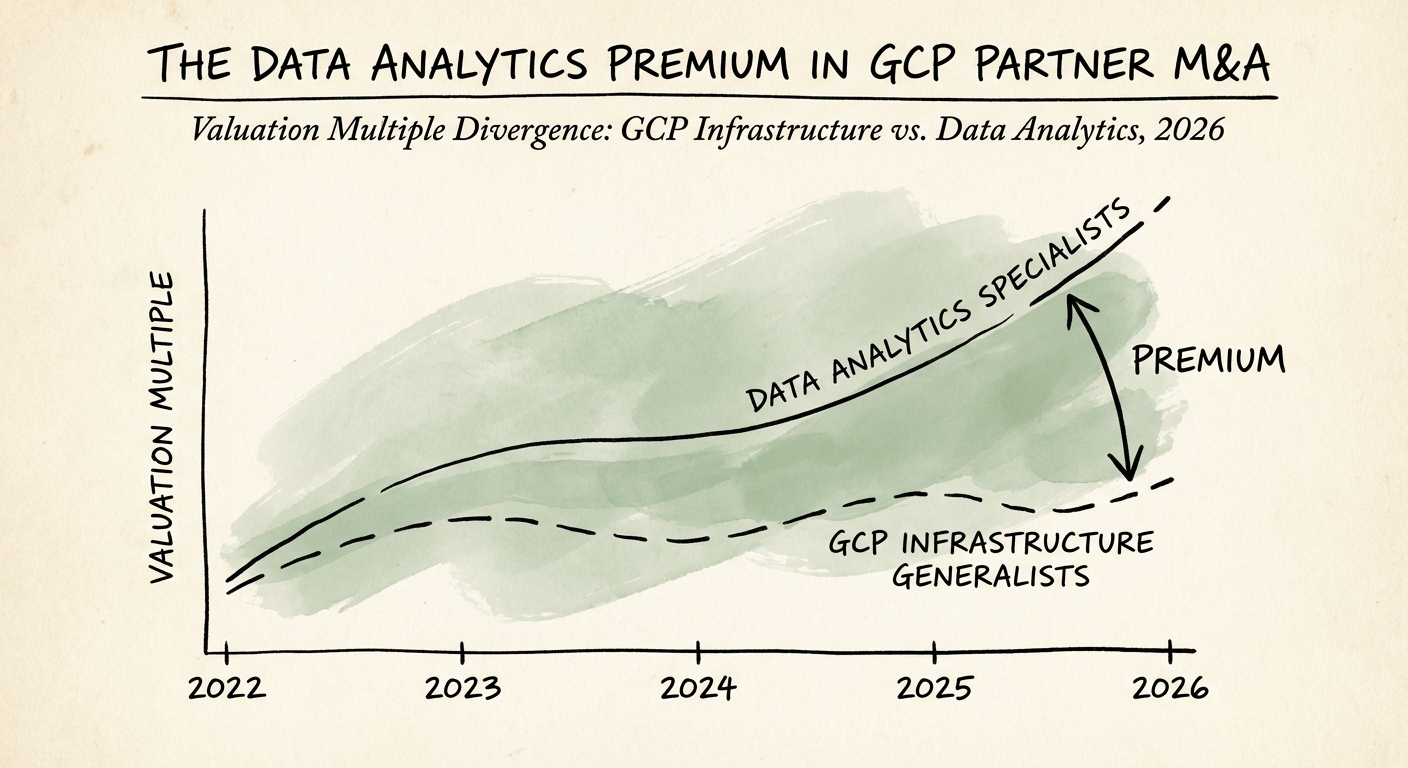

The Data Analytics Premium: Why GCP Partners Trade at 14x (And Generalists Stall at 8x)

Why GCP partners with Data Analytics & BigQuery specializations trade at 14x EBITDA while infrastructure generalists stall at 8x. A diagnostic guide for PE investors.

13.6x Avg. EBITDA Multiple (Data Spec.)

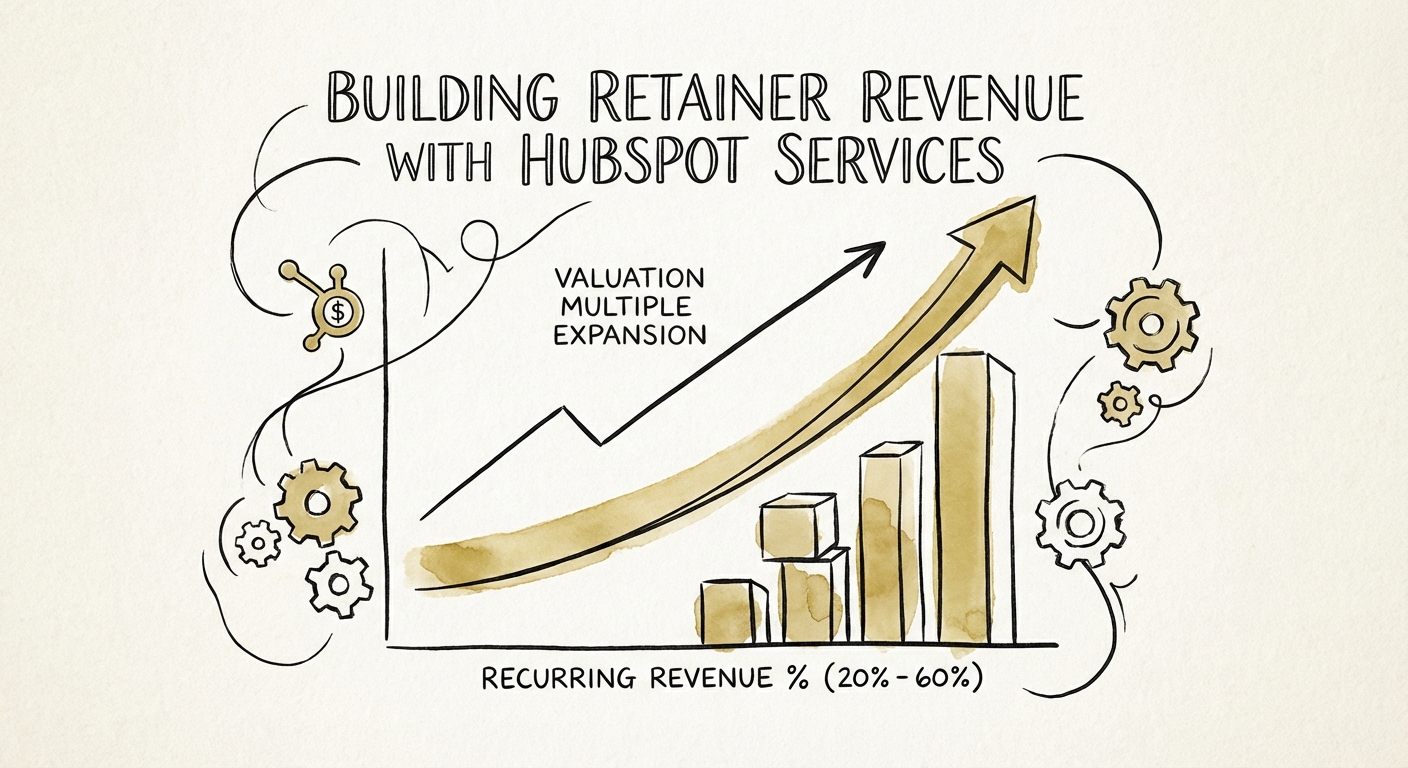

BRIEF · REVENUE ARCHITECTURE

How to Build Retainer Revenue with HubSpot Services: The "ROaaS" Playbook

Stop the implementation hamster wheel. A guide for HubSpot partners to pivot from project revenue to high-margin RevOps retainers. Benchmarks, pricing, and valuation impact.

3x Valuation Multiple Lift

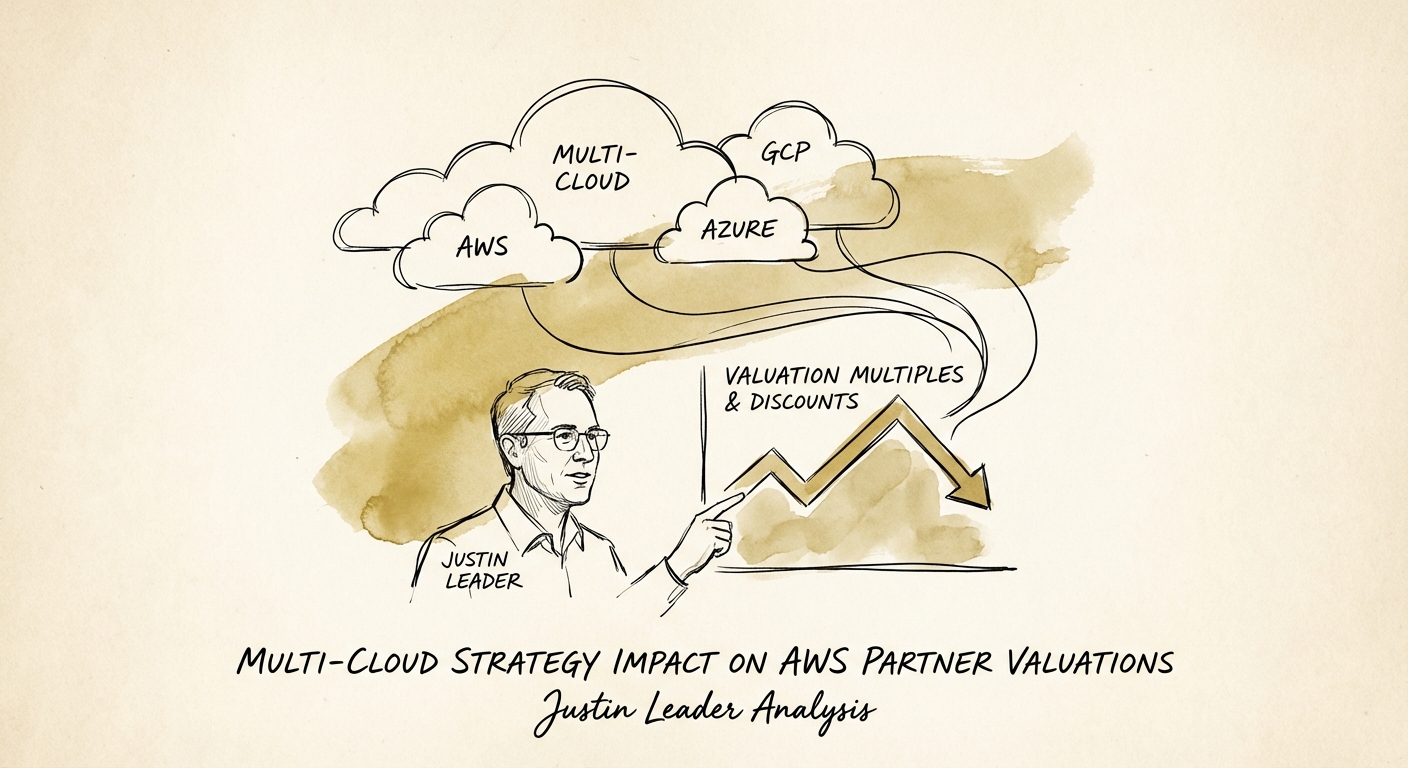

BRIEF · EXIT READINESS

Multi-Cloud Strategy Impact on AWS Partner Valuations: The 'Generalist Discount' vs. The Specialist Premium

Why adding Azure and GCP might reduce your exit value multiple. Benchmarks on the 'Generalist Discount' vs. the 'Specialist Premium' for AWS Partners in 2026.

4.2x Valuation Turn Gap

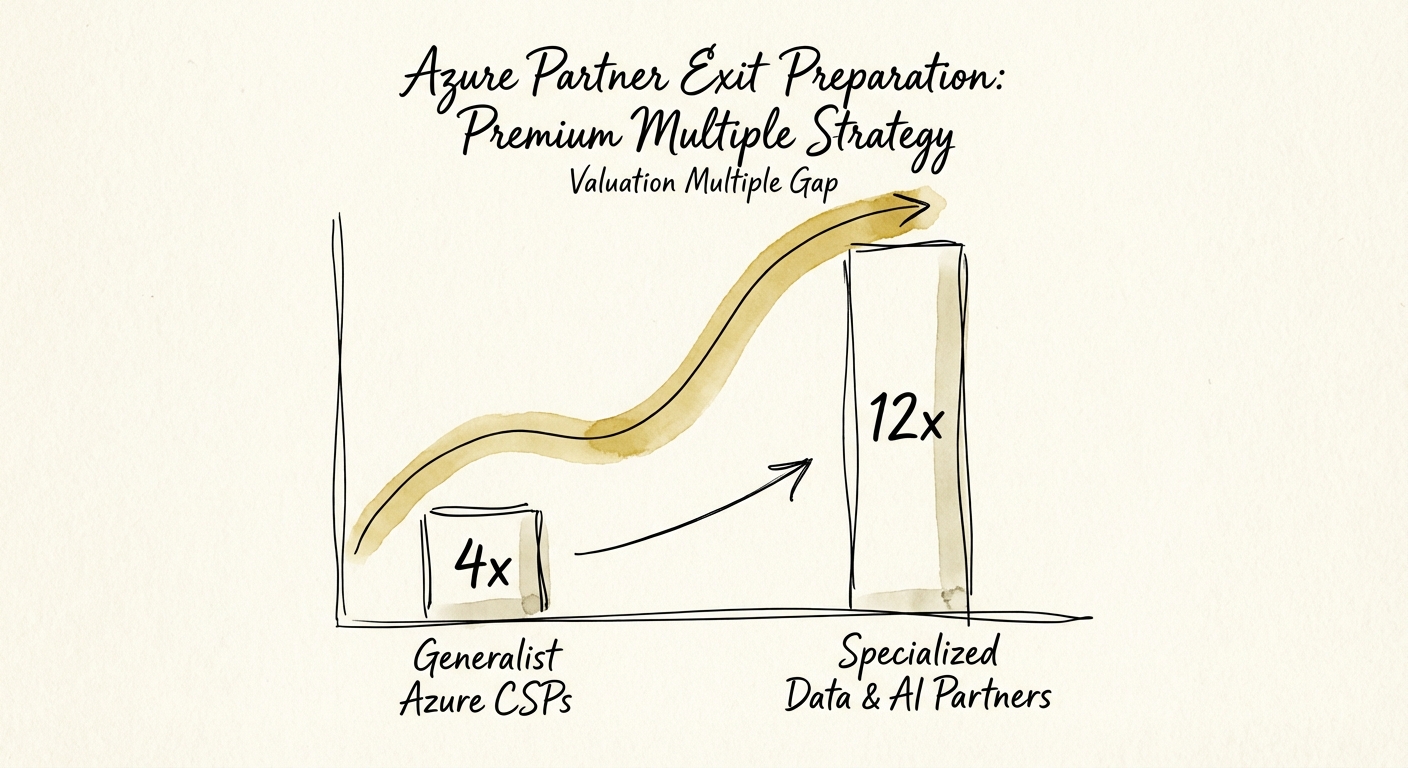

BRIEF · EXIT READINESS

Azure Partner Exit Preparation: The Gap Between 4x and 12x Multiples in 2026

Azure partner valuation multiples have bifurcated in 2026. Generalist CSPs trade at 4x EBITDA while Data & AI specialists command 12x+. Here is the exit roadmap.

12x EBITDA Multiple

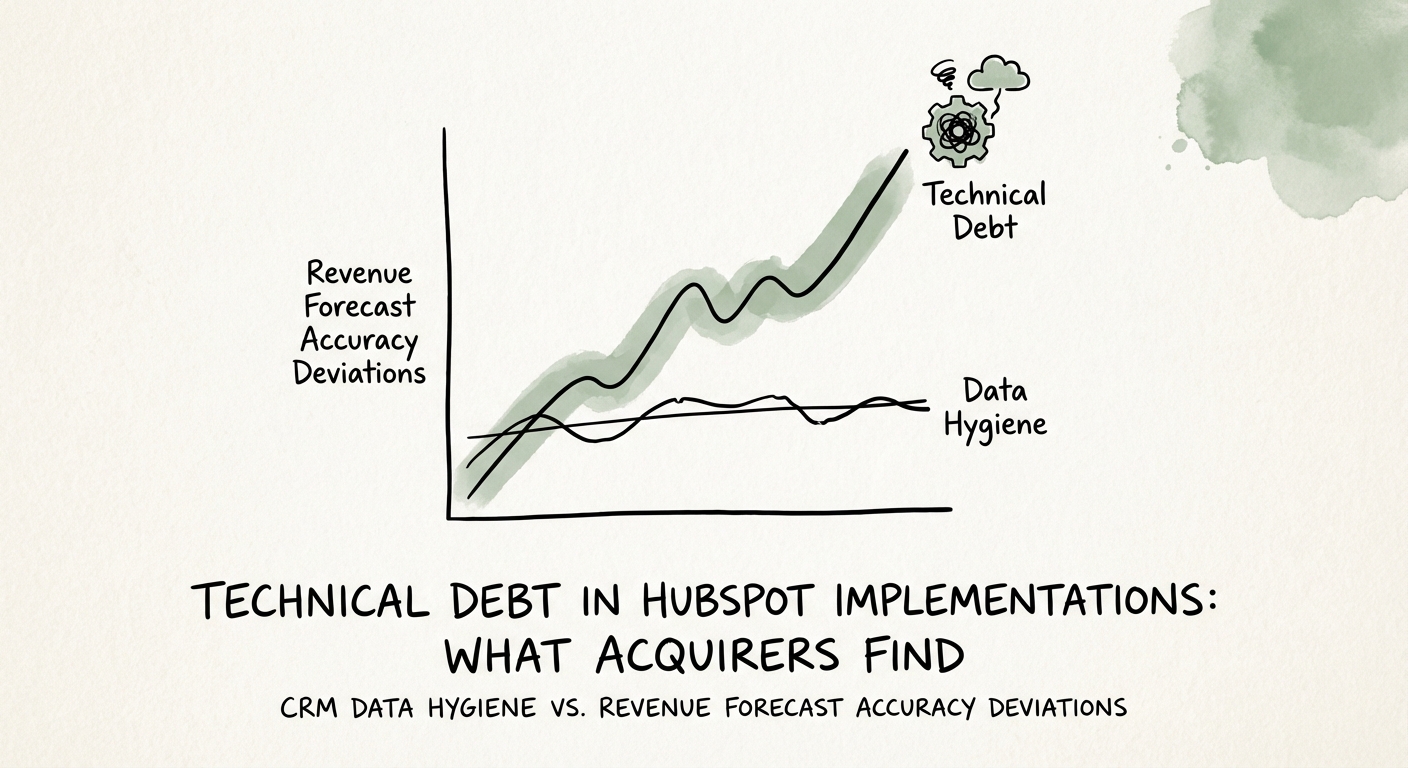

BRIEF · TECHNICAL DEBT

Technical Debt in HubSpot Implementations: The $2M 'Ghost Pipeline' Hidden in Due Diligence

HubSpot technical debt kills post-acquisition value. Learn why 43% of forecasts fail and how to spot 'Franken-Spot' implementations in due diligence.

43% of sales orgs miss forecast targets due to bad data

BRIEF · EXIT READINESS

How PE Firms Evaluate Workday Partner Acquisitions: The 2026 Diagnostic

A private equity guide to valuing Workday partners in 2026. Analysis of 14.5x EBITDA multiples, AMS revenue mix benchmarks, and the specific due diligence risks that kill deals.

14.5x EBITDA Multiple (Elite AMS Partners)

BRIEF · REVENUE ARCHITECTURE

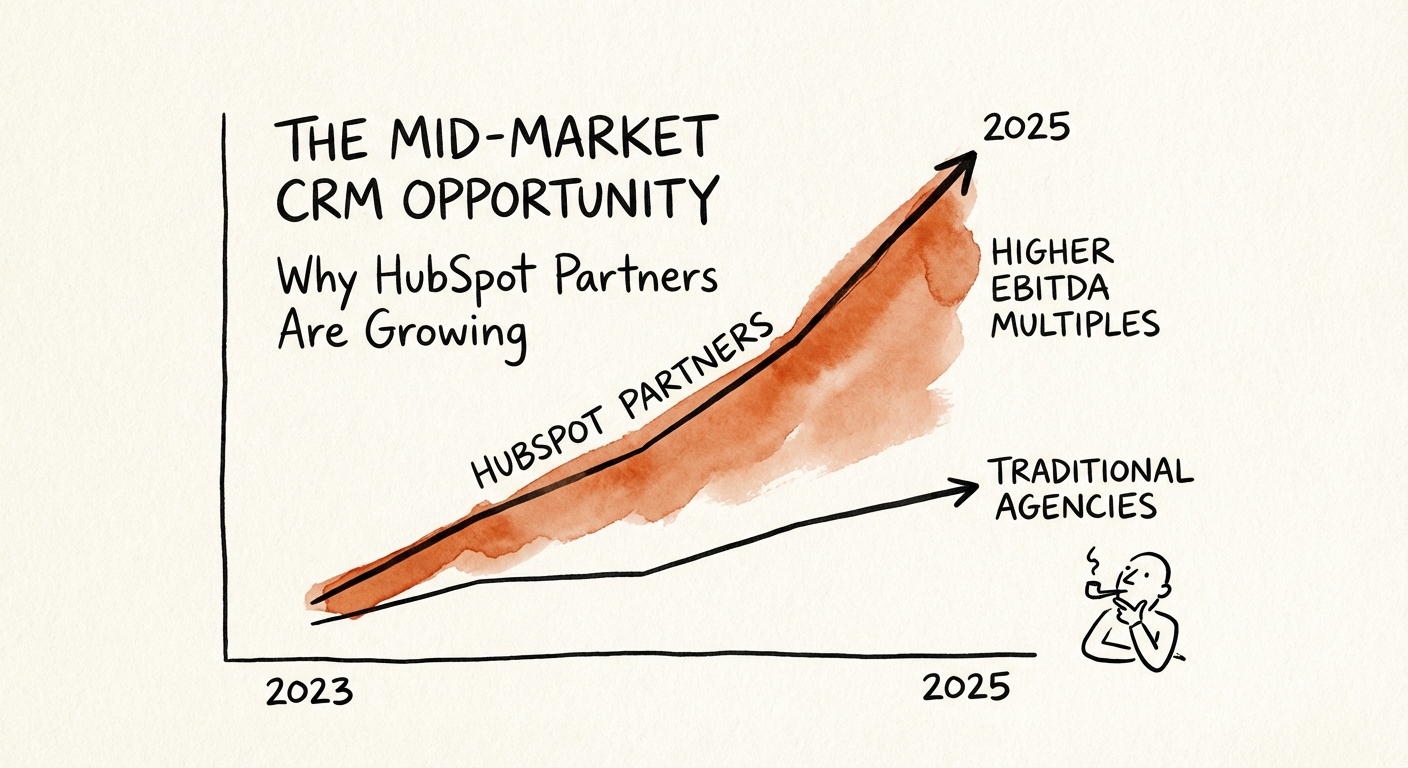

The "Teal" market opening: Why HubSpot Partners Are Commanding 12x Multiples

Mid-market CRM migration is driving a valuation surge for HubSpot partners. Discover why PE firms are paying 12x EBITDA for RevOps consultancies.

12.1x EBITDA Multiple

BRIEF · GTM EXECUTION

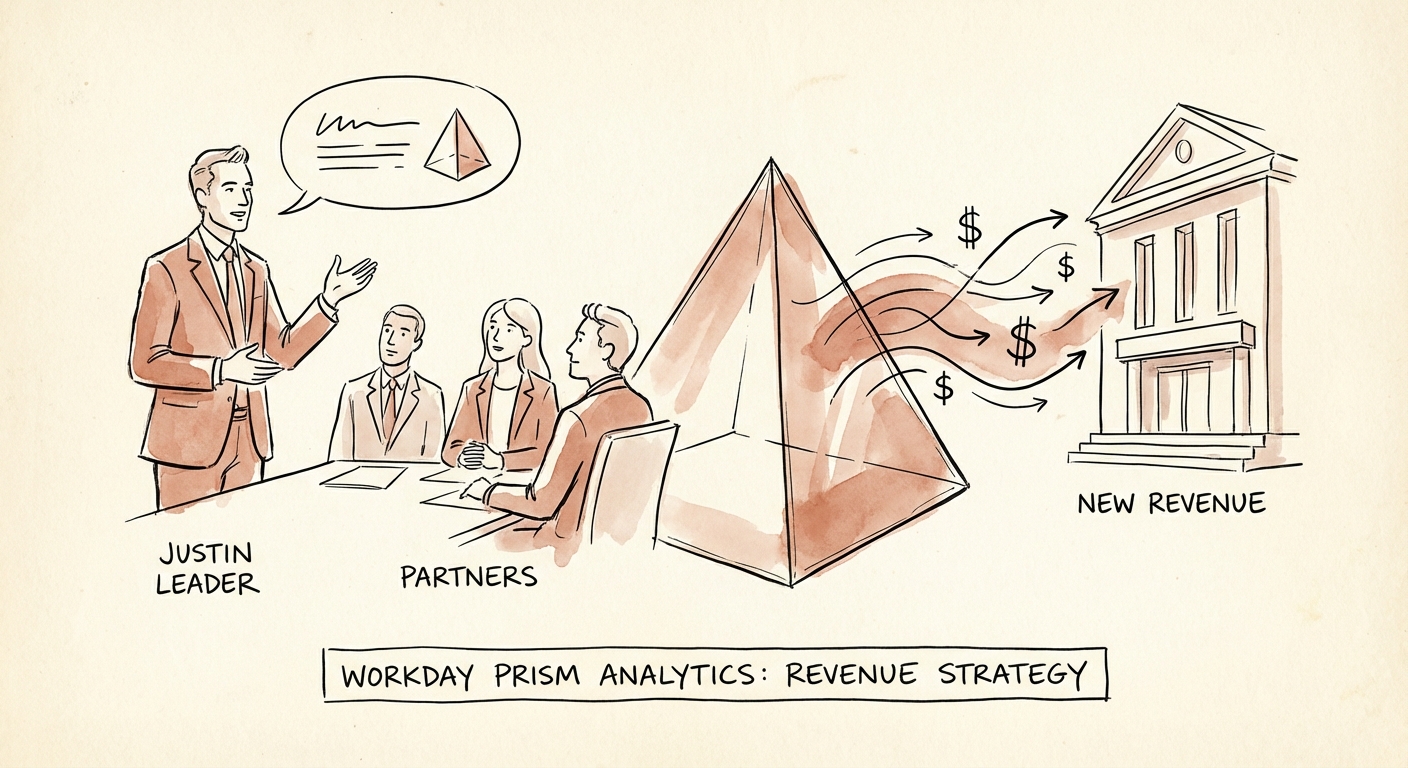

Workday Prism Analytics: The 'Data Wedge' Strategy to Break the $20M Ceiling

Why Workday partners building Prism Analytics practices command 35% higher bill rates and 12x exit multiples. A diagnostic for scaling CEOs.

12x EBITDA Multiple for Data-First Partners

BRIEF · GTM EXECUTION

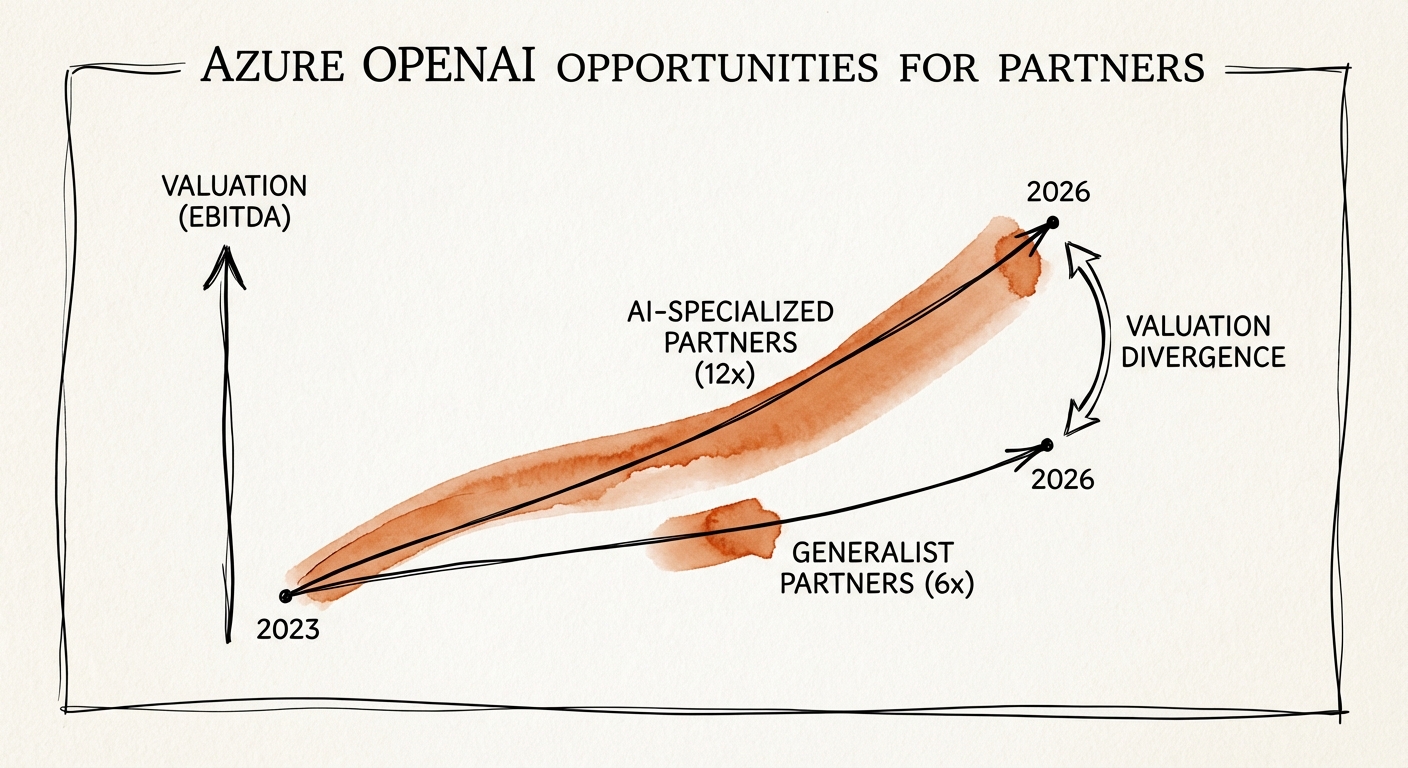

The Azure OpenAI Valuation Gap: Why 'Copilot Deployments' Are Worth 6x and Custom IP Is Worth 12x

The Copilot sugar rush is over. Discover why Azure OpenAI partners building custom IP are trading at 12x EBITDA while resellers stall at 6x. 2026 Benchmarks.

12x EBITDA Multiple for AI-IP Partners

BRIEF · EXIT READINESS

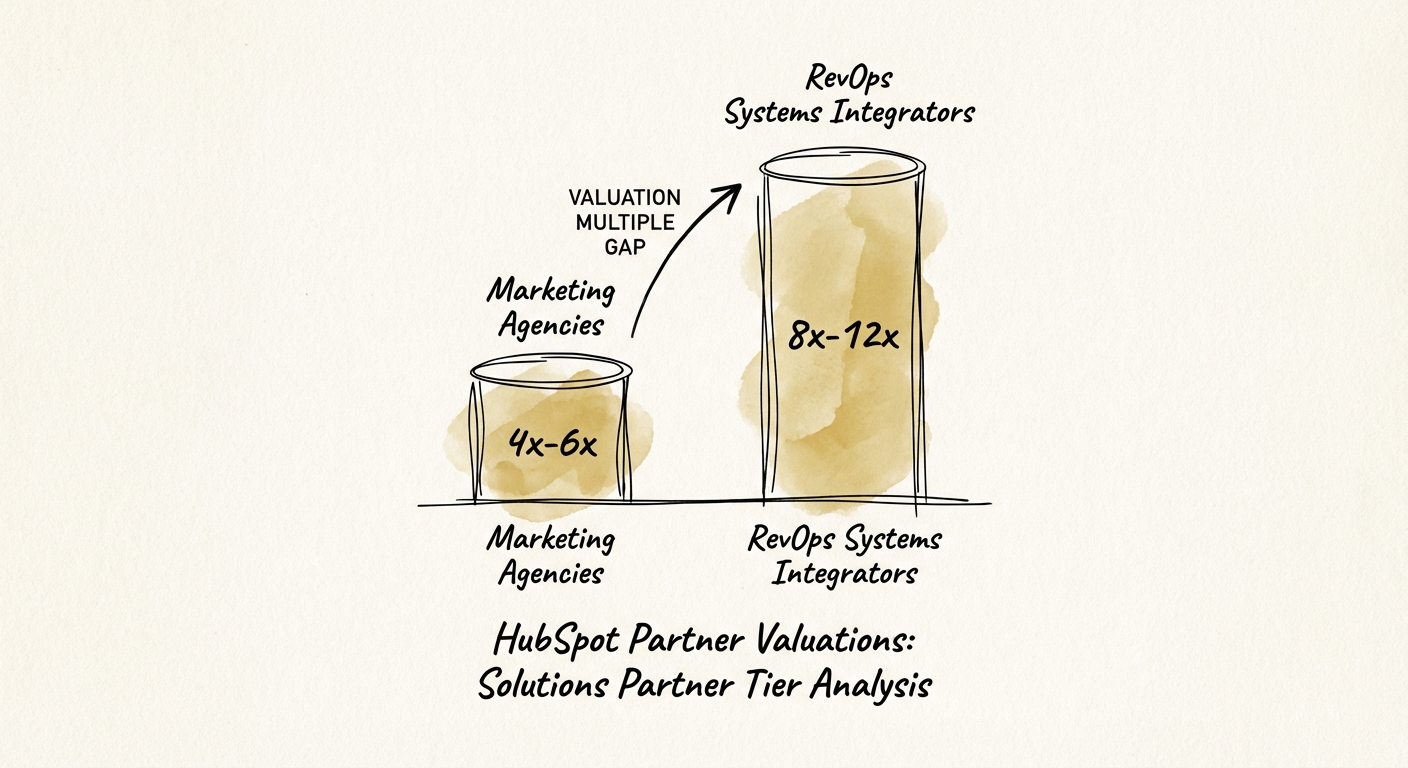

HubSpot Partner Valuations: The Gap Between "Elite" Status and Elite Multiples

HubSpot Elite status doesn't guarantee a premium exit. Learn the 2026 valuation gap between marketing agencies (4x) and RevOps SIs (10x+).

8x-12x SI Valuation Multiple

BRIEF · FINANCIAL INFRASTRUCTURE

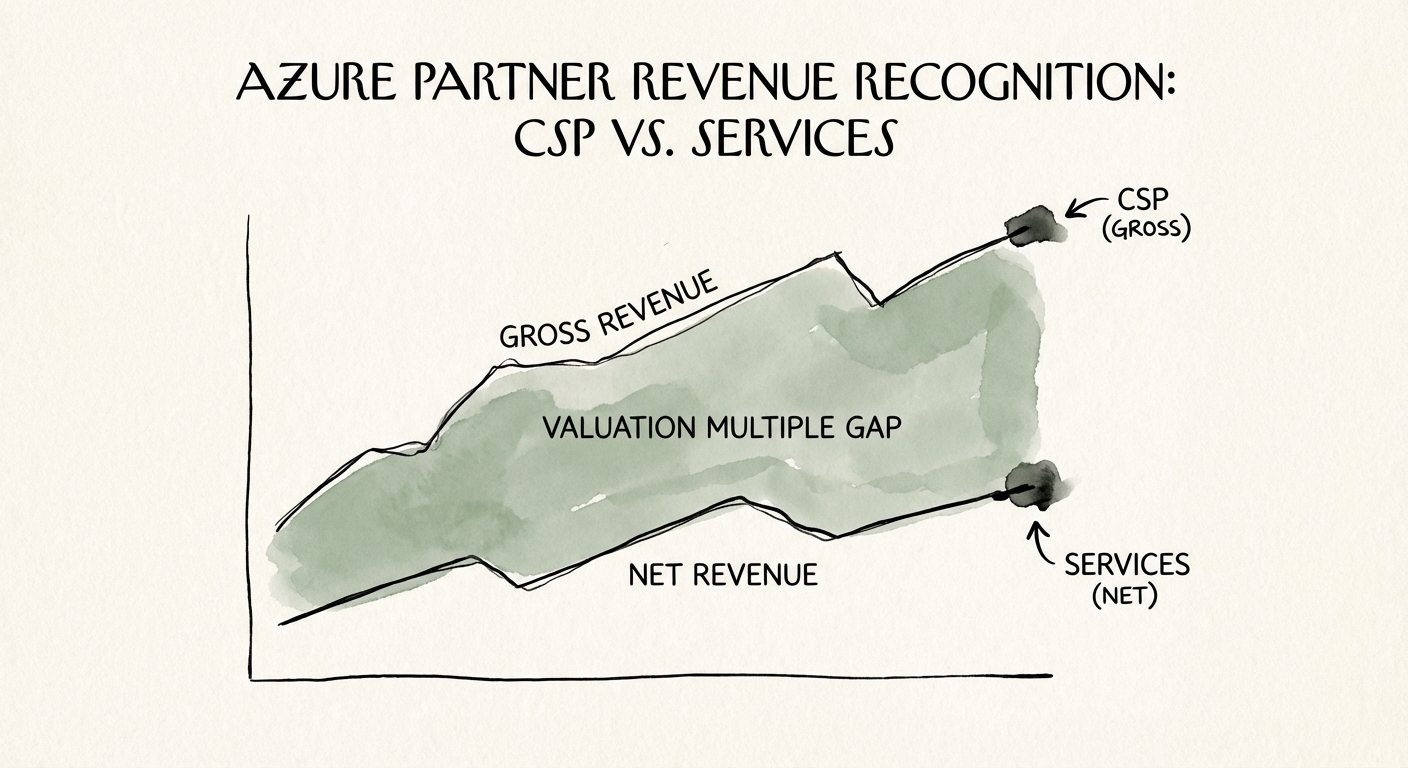

The 'Azure Revenue Illusion': Why Your CSP 'Growth' is Destroying Your EBITDA Multiple

Stop blending Azure resale with professional services. Learn why Gross vs. Net revenue recognition impacts your valuation and how to fix your books before Due Diligence.

4x-6x Valuation Drop

BRIEF · REVENUE ARCHITECTURE

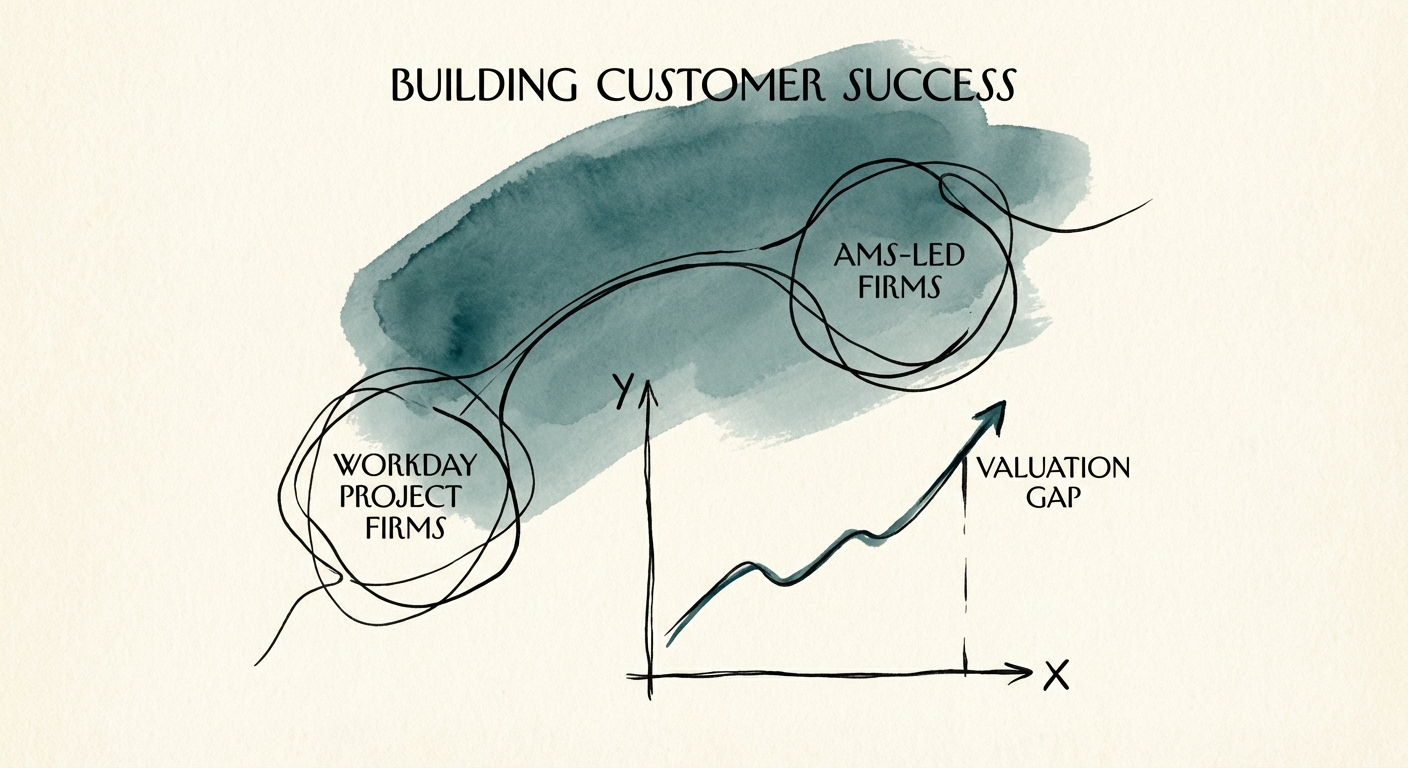

The 'Go-Live Cliff': Why Workday Partners Bleed 50% of Exit Value (And How to Build a True CS Practice)

Workday implementation firms with strong Customer Success practices trade at 12x EBITDA. Those without trade at 5x. Here is the diagnostic playbook to fix your revenue mix.

12x EBITDA Multiple for AMS-Led Firms

BRIEF · GTM EXECUTION

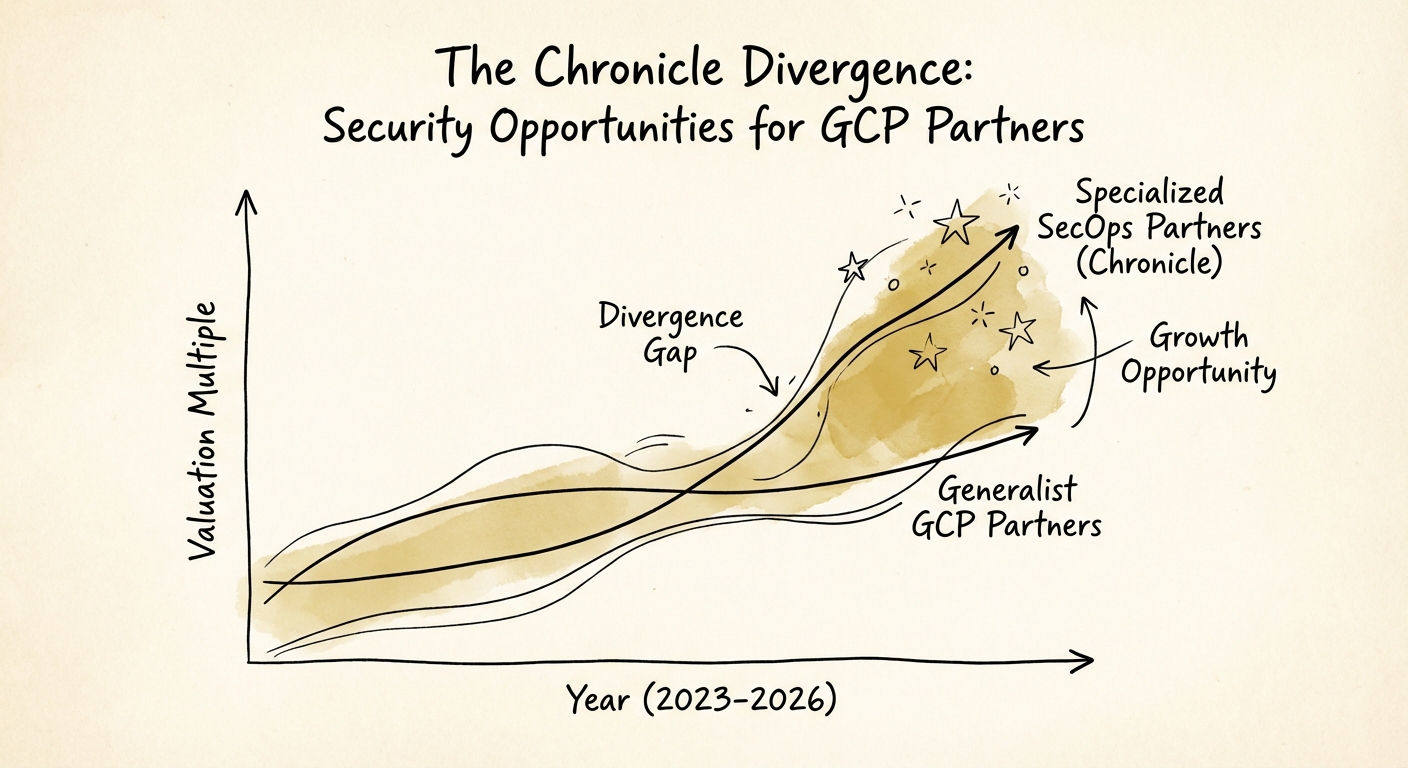

The Chronicle Arbitrage: Why Smart GCP Partners Are Pivoting to SecOps

For GCP partners, Chronicle (Google SecOps) offers a path from low-margin resell to high-margin MSSP revenue. Analysis of valuation multiples, service margins, and execution strategy.

14x Potential EBITDA Multiple for SecOps-Specialized Partners

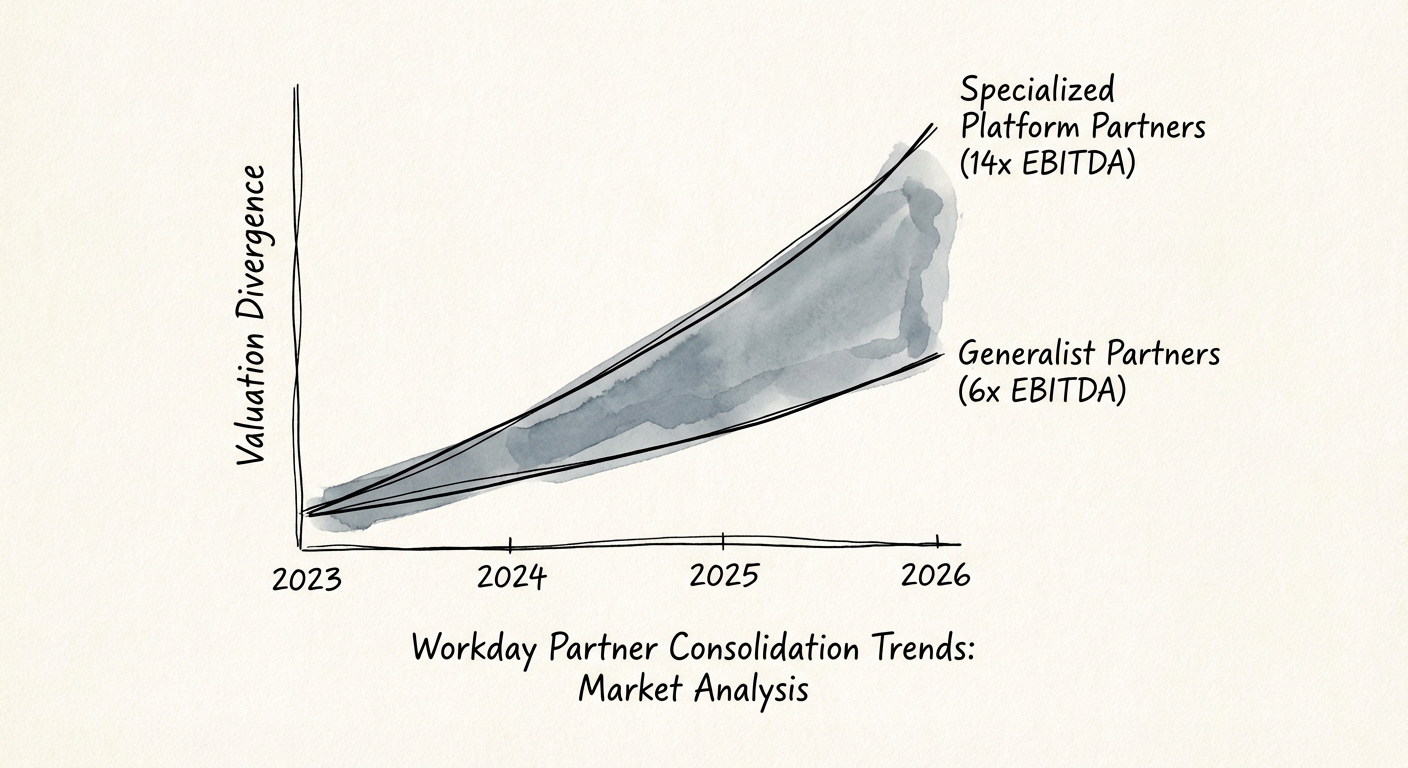

BRIEF · EXIT READINESS

Workday Partner Consolidation: Why Niche Firms Are Trading at 14x While Generalists Stall

Analysis of 2026 Workday partner M&A trends. Why niche firms with Financials & AI expertise trade at 14x EBITDA while generalist HCM shops stall at 6x.

14x EBITDA Multiple for 'Platform' Partners

BRIEF · FOUNDER EXTRACTION

The Azure Founder Trap: Why Your 'Genius' Is Costing You a 50% Valuation Haircut

Learn how to scale your Azure practice beyond $10M revenue by eliminating founder dependencies. A diagnostic guide for MSP CEOs on process, packaging, and valuation.

50% Valuation Haircut for Founder Dependency

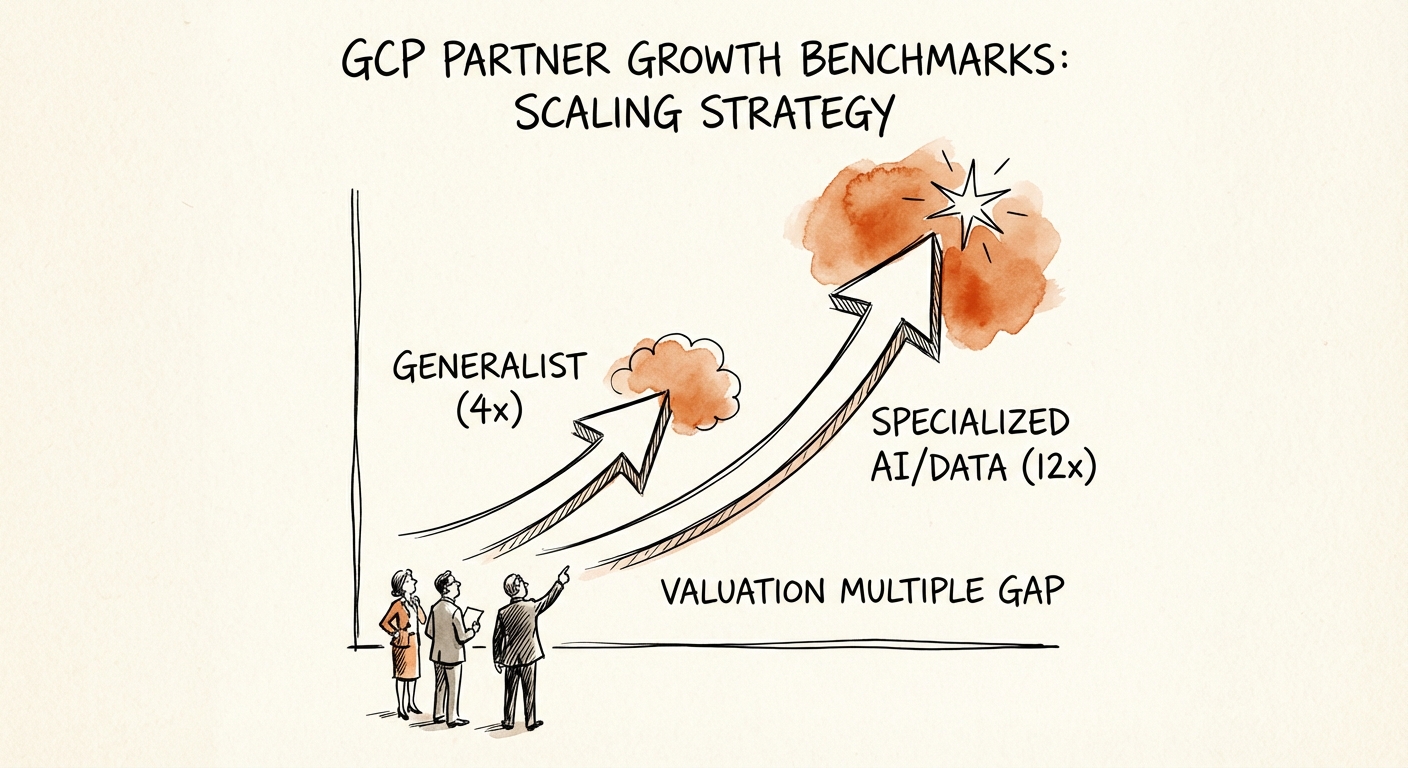

BRIEF · EXIT READINESS

GCP Partner Growth Benchmarks: The $10M to $50M Scaling Strategy

2026 growth benchmarks for GCP partners. How to scale from $10M to $50M, unlock the $7.54 multiplier, and escape the 'generalist' valuation trap.

$7.54 Partner Revenue per $1 GCP Sold

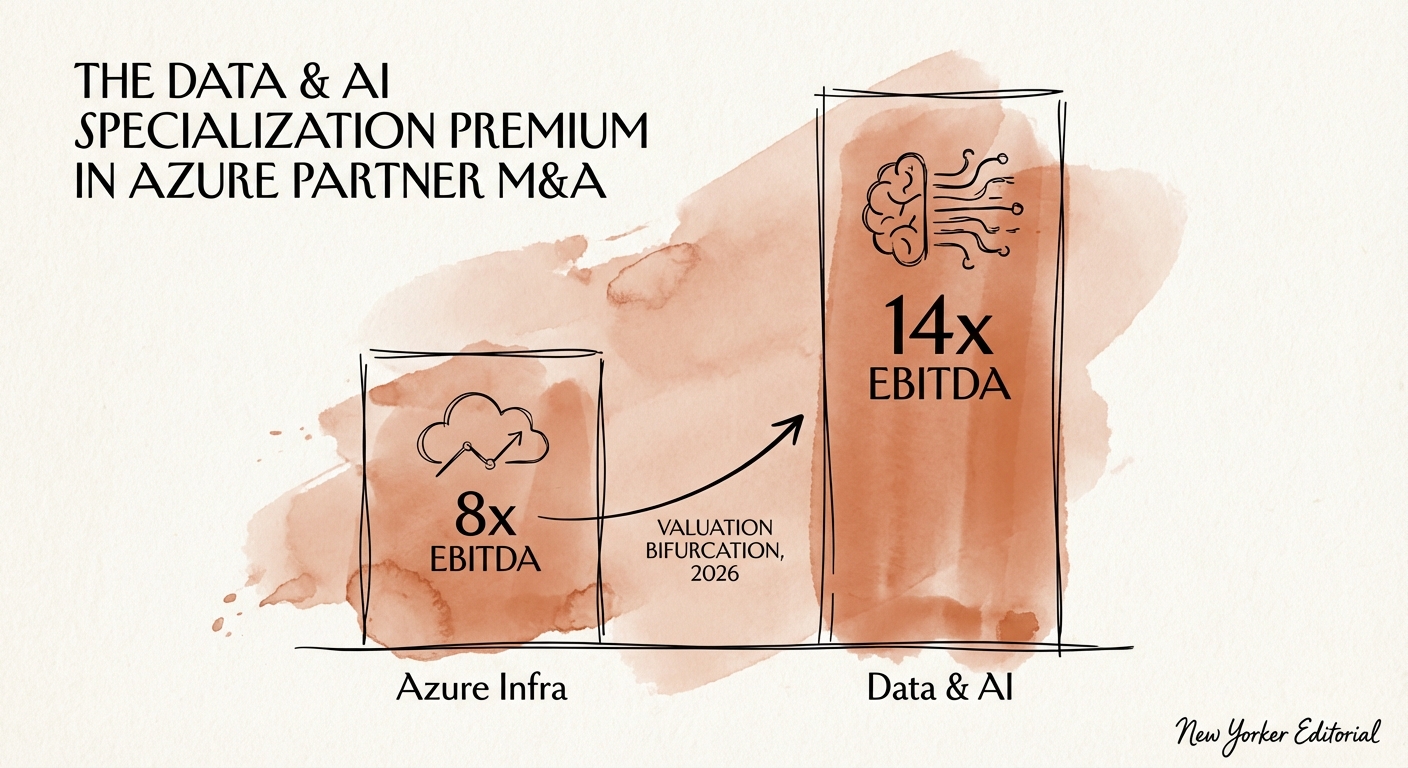

BRIEF · EXIT READINESS

The Data and AI Specialization Premium: Why Azure Specialists Trade at 14x While Generalists Stall at 8x

Azure partners with deep Data & AI capabilities (Fabric, OpenAI) command a 6-turn EBITDA premium over infrastructure generalists. Here is the 2026 M&A diagnostic.

Premium Median EBITDA Multiple (Data & AI Specialists)