BRIEF · AI GOVERNANCE AND TRAINING

The Recap Email Is Where AI Quietly Commits Your Firm to Things You Never Agreed To

An AI recap email turned "we'll explore it" into "we'll deliver it." Here's the line between AI you let send and AI you keep on a leash.

4 meeting controls before automation

BRIEF · AI MEASUREMENT AND ROI

The AI Wrote 200 Training Docs. Your Ramp Time Didn't Move. Now What?

AI can generate hundreds of training docs in a weekend. Here's how to measure whether any of it shortened new-hire ramp, cut escalations, or just made a bigger pile.

4 training ROI outcomes to measure

BRIEF · AI GOVERNANCE AND TRAINING

When AI-Generated Training Docs Quietly Become Company Policy

Training documentation is the one place a new hire treats AI output as gospel. Here are the three red flags that mean you fix the source before you automate.

3 red flags before automation

BRIEF · AI MEASUREMENT AND ROI

The AI Status Report That Reads Green While the Project Burns

An AI status draft will smooth over a slipped dependency unless you measure for it. Here's how to prove project-status ROI without buying prettier lies.

5 measures needed for project status reporting ROI

BRIEF · AI MEASUREMENT AND ROI

AI Scheduling ROI for Services Firms: The Utilization Math That Actually Counts

A booked calendar slot isn't ROI. Here's how professional services leaders tie AI scheduling to billable utilization, fewer reschedules, and clean handoffs.

4 ROI signals for scheduling coordination

BRIEF · AI TRANSFORMATION STRATEGY

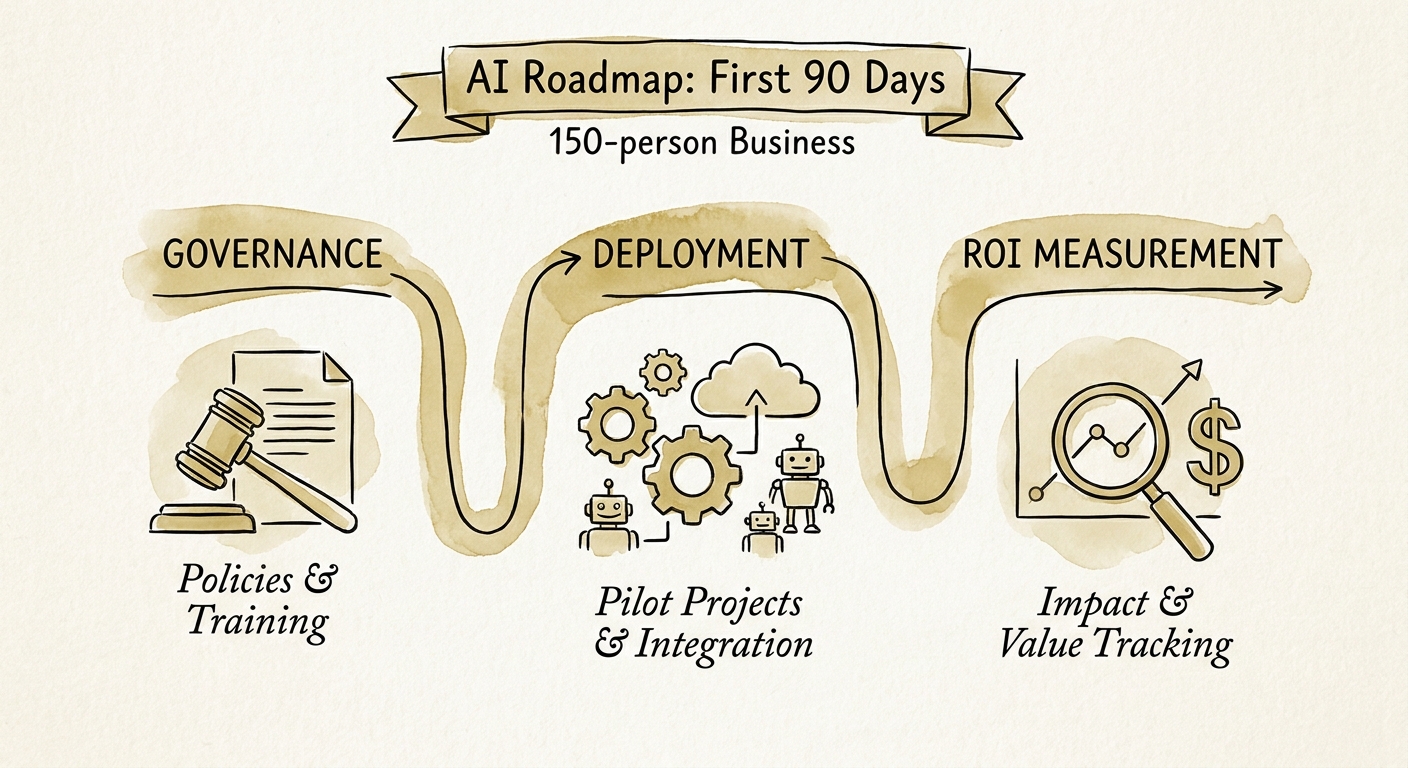

The 90-Day AI Roadmap for a 150-Person Company (Where One Bad Pilot Gets Noticed by Everyone)

A 150-person company has real silos but no slack for a failed rollout. Here is a 90-day AI plan that ships one trusted workflow instead of 12 stalled pilots.

90 days to move from assessment to first production workflow

BRIEF · AI TRANSFORMATION STRATEGY

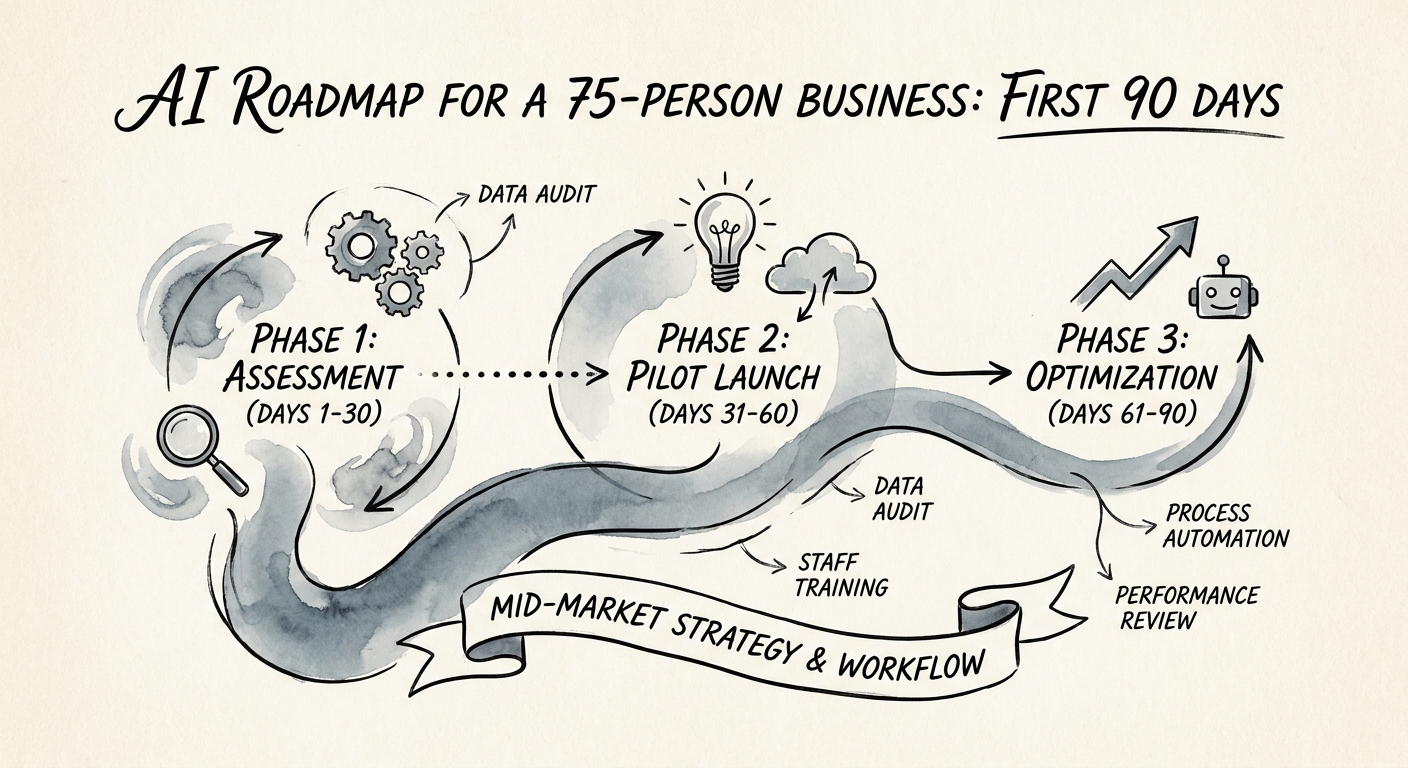

The AI Roadmap That Fits a 75-Person Company (No CIO Required)

At 75 people you have no AI budget for theater and no slack for chaos. A roadmap that names one workflow, one owner, and one metric before any vendor.

90 days to validate the first roadmap workflow

BRIEF · AI INDUSTRY USE CASES

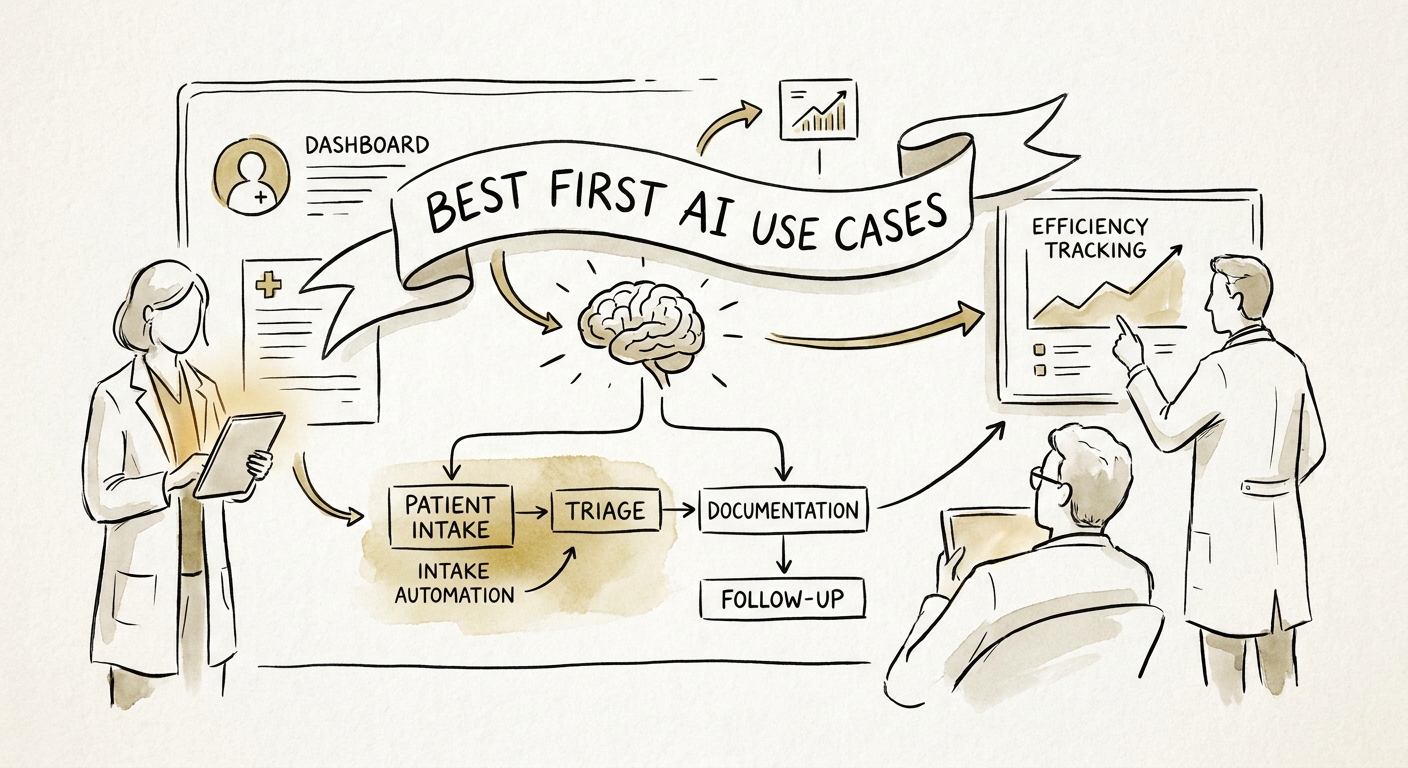

Where Specialty Practices Should Point AI First (Hint: Not the Exam Room)

A specialty practice's safest first AI wins live in prior auth, referral packets, and intake — not clinical judgment. Here's how to pick the first one.

4 administrative workflows to assess before clinical AI

BRIEF · AI INDUSTRY USE CASES

The First AI Win in a Factory Is a Better Corrective Action Report

Skip the lights-out factory pitch. The fastest AI wins for manufacturers live in CAPAs, work-order notes, and quote prep. Here's where to start and why.

90 days to prove one governed manufacturing AI workflow

BRIEF · AI GOVERNANCE AND TRAINING

When Not to Automate Customer Feedback Analysis (B2B SaaS Edition)

A B2B SaaS playbook for when AI should tag feedback themes and when an NPS comment, churn signal, or renewal blocker has to land on a human's desk.

5 feedback categories that should stay human-reviewed

BRIEF · AI MEASUREMENT AND ROI

Document Intake AI: Why "Hours Saved" Is the Wrong Number

Document intake AI pays off in fewer exceptions and faster handoffs, not hours saved. Here's the five-number scorecard that survives a CFO's review.

5 measures needed for document intake ROI

BRIEF · AI GOVERNANCE AND TRAINING

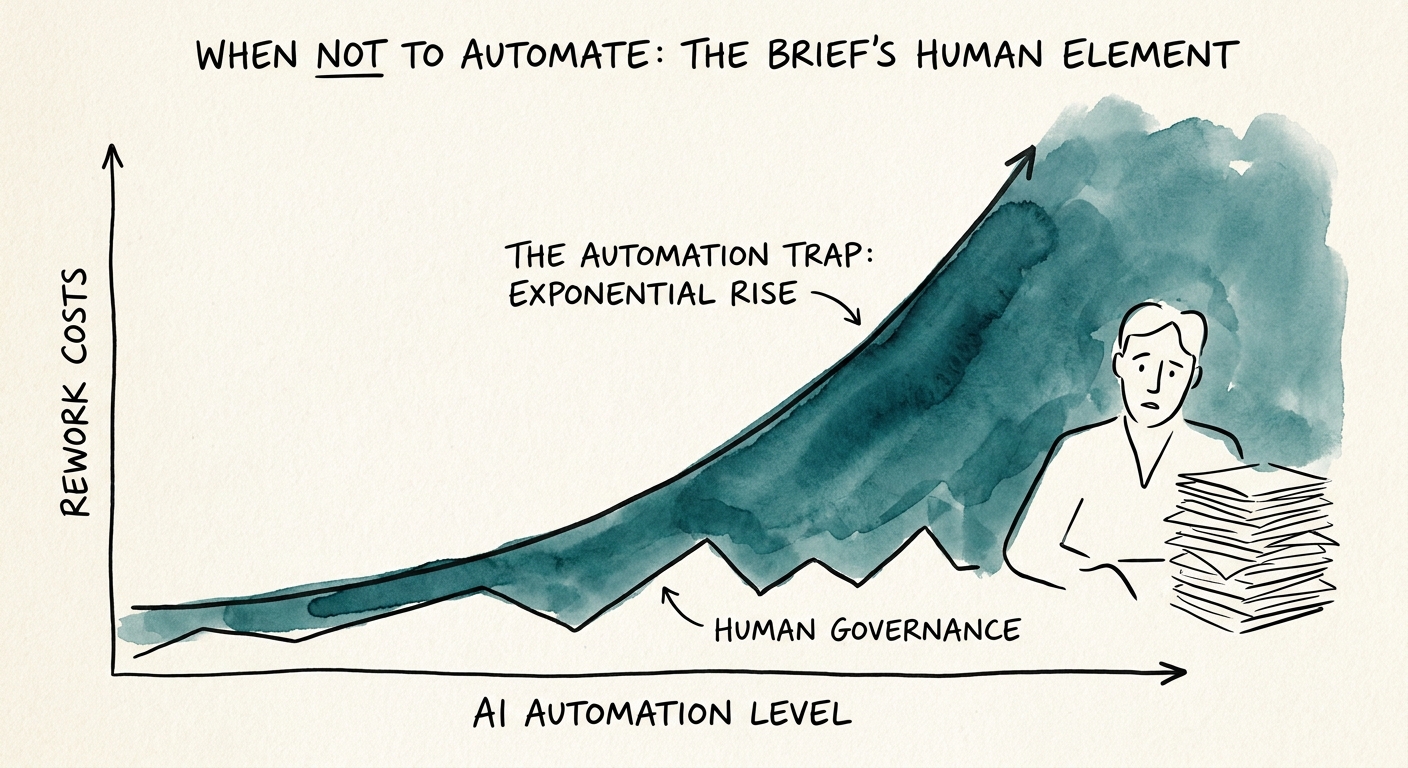

When Not to Automate Marketing Brief Generation With AI

An AI that writes marketing briefs in 90 seconds is worthless if the brief is wrong. Five signals your briefing process is too fuzzy to automate yet.

5 blockers before marketing brief automation

BRIEF · AI GOVERNANCE AND TRAINING

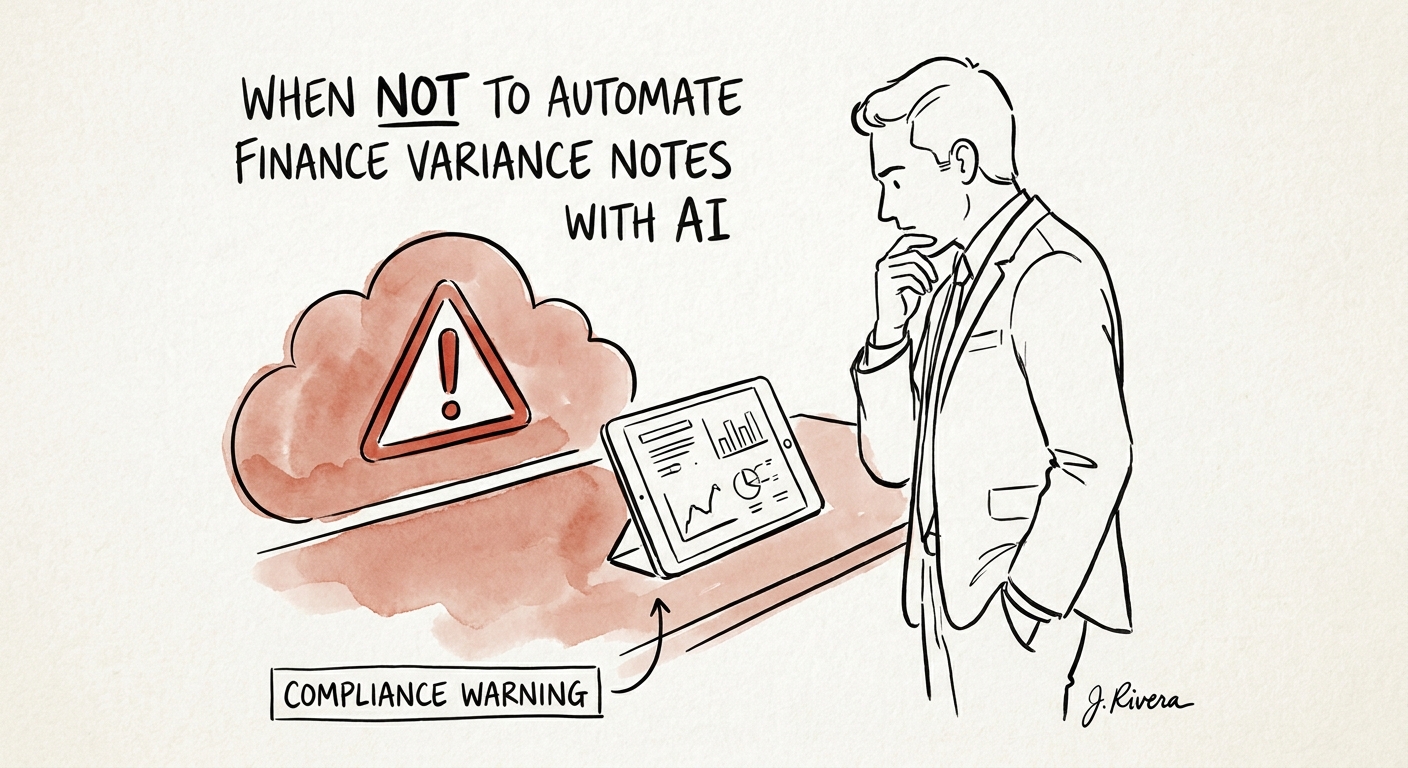

The Variance Note AI Should Never Sign: Where to Stop Automating FP&A

A variance note is a management claim about what changed and why. Here's the line where AI drafting ends and your controller's judgment has to start.

4 finance controls before automation

BRIEF · AI GOVERNANCE AND TRAINING

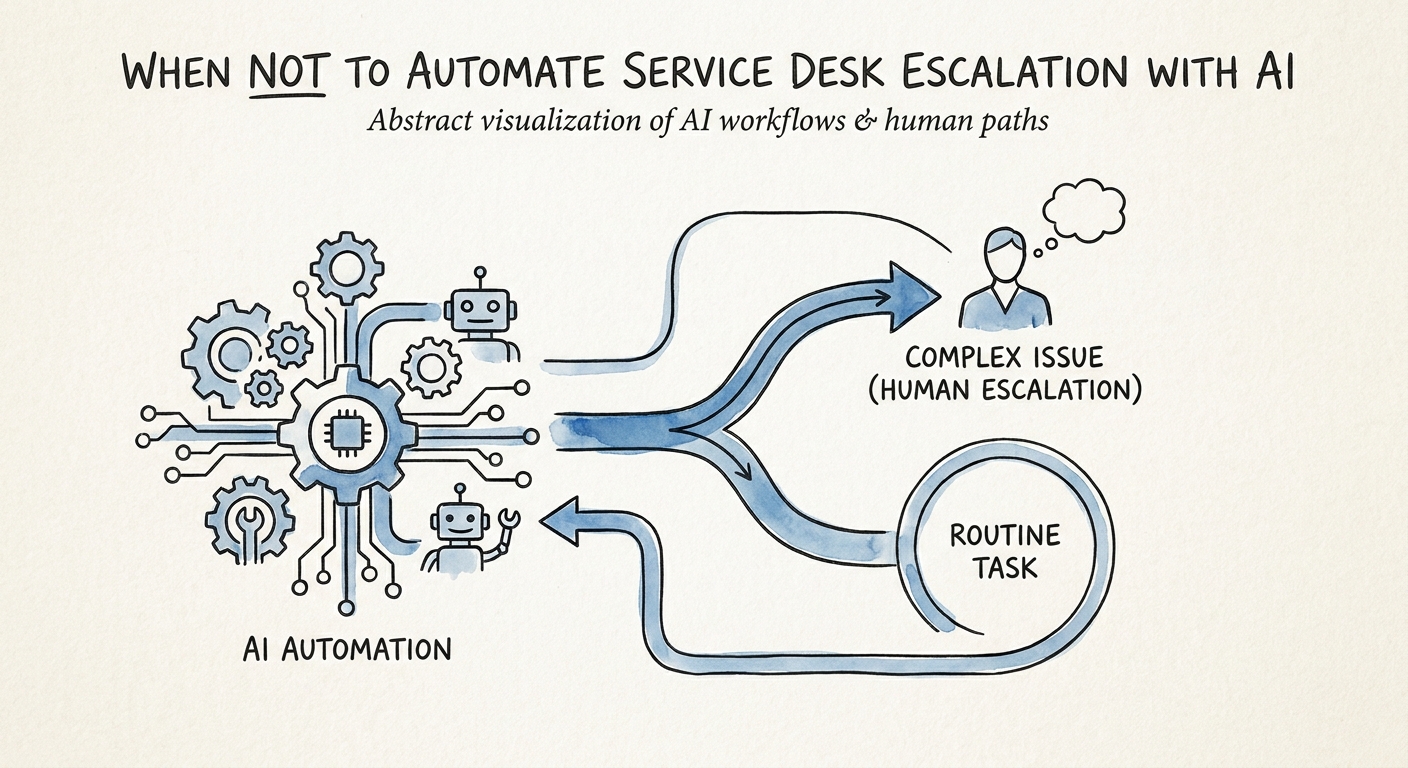

Don't Let AI Decide When a Ticket Becomes a Sev-1

Escalation is where a ticket changes severity, owner, and permissions at once. Four things have to be true before AI gets to make that call. Here they are.

4 service desk controls before automation

BRIEF · AI WORKFLOW AUTOMATION

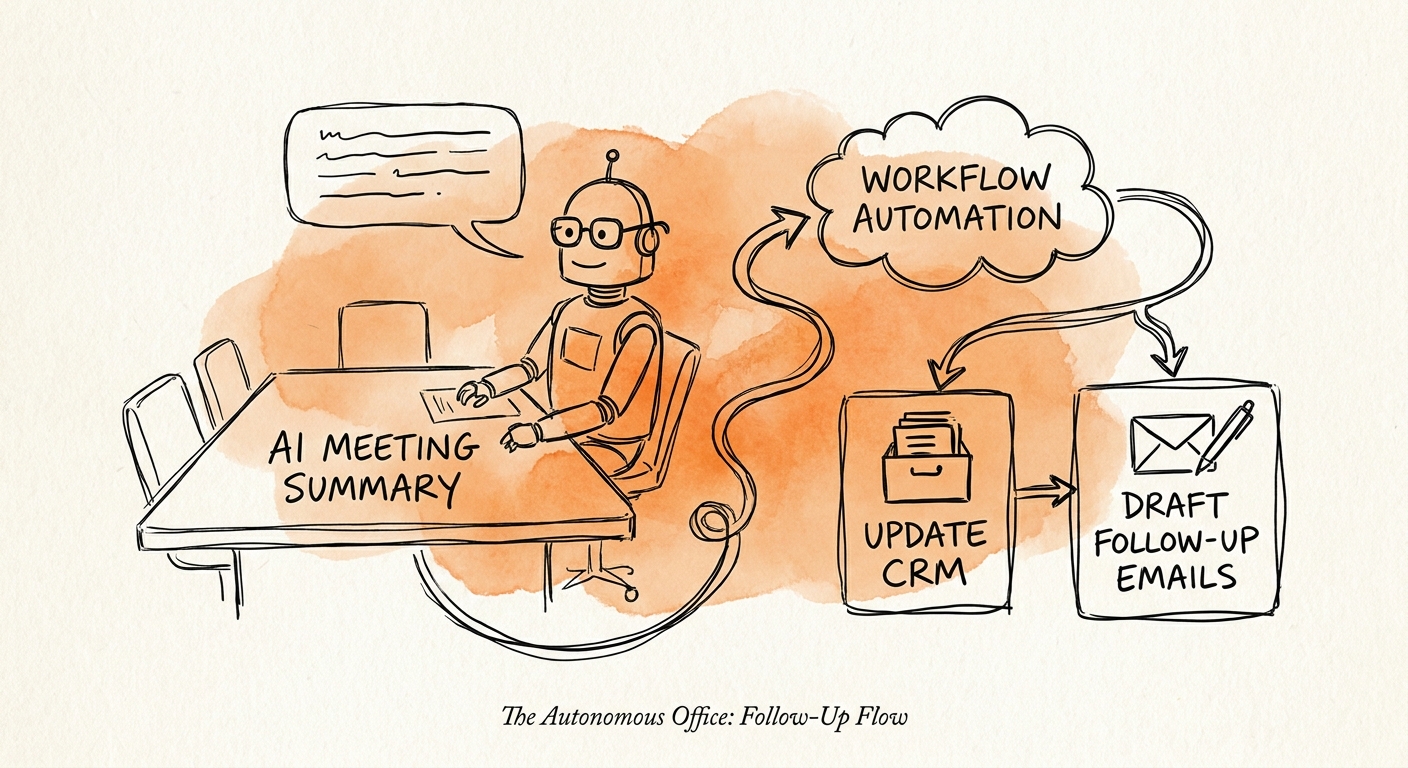

The Meeting Ended Friday. The CRM Found Out Tuesday. AI Can Close That Gap.

Most meeting AI just makes prettier notes. Here's how to turn a transcript into owner-approved decisions, tasks, and CRM updates that actually get done.

4 outputs to review after each meeting

BRIEF · AI INDUSTRY USE CASES

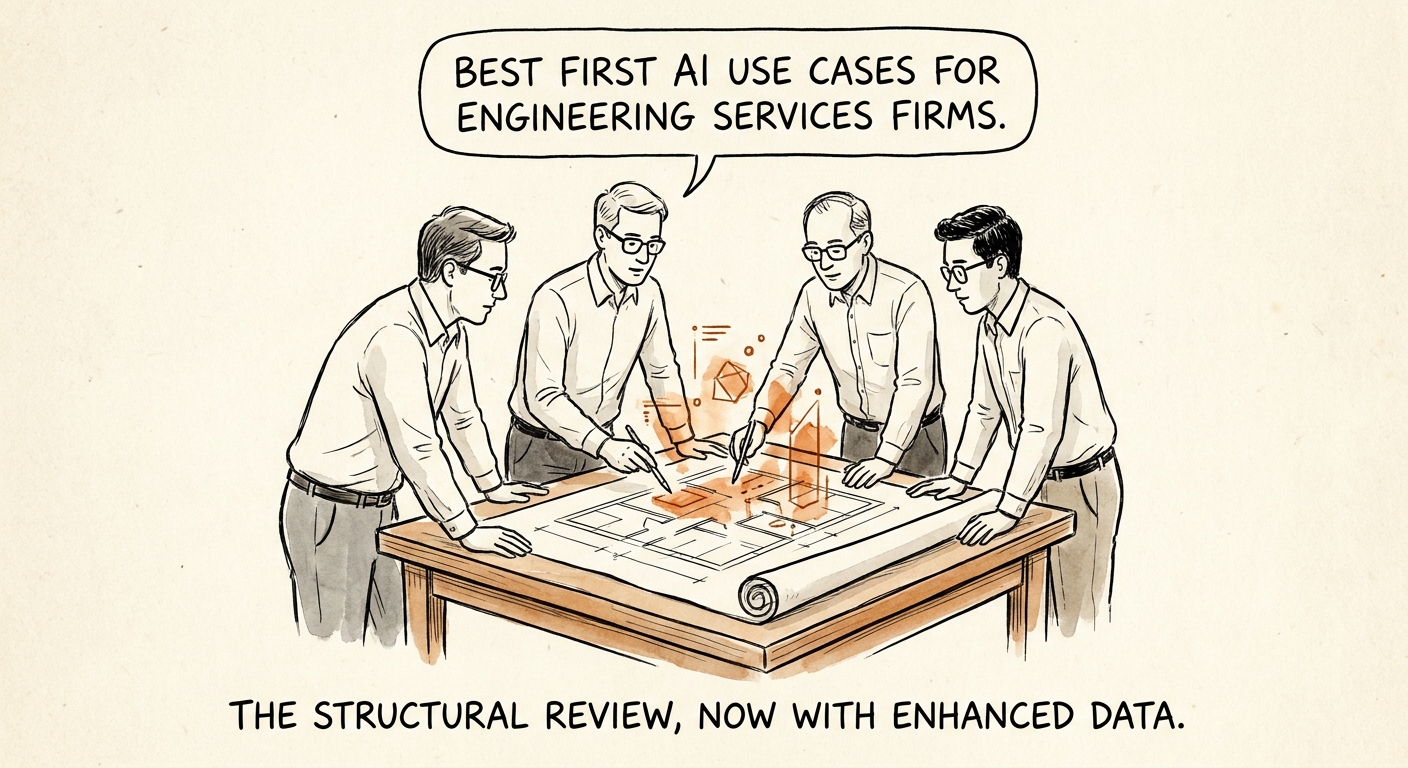

Your Best Engineers Are Stamping PDFs and Hunting for Last Year's Calc Sheet. Start AI There.

The four AI workflows engineering services firms should run first: prior-project retrieval, status reporting, proposal drafting, and QA review prep — judgment stays human.

4 safe first-use-case lanes

BRIEF · AI WORKFLOW AUTOMATION

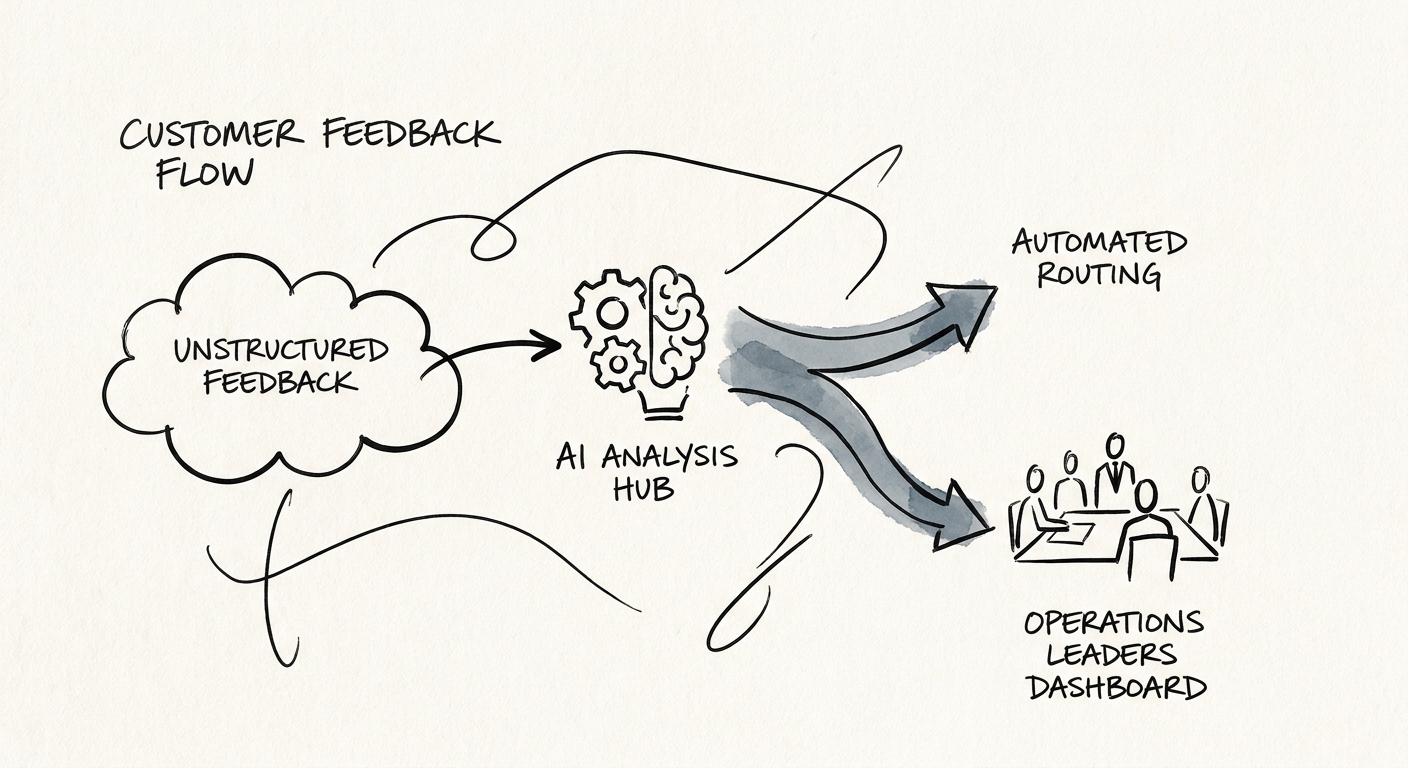

Turn 4,000 Customer Comments Into Three Decisions: AI for Feedback Analysis

Most feedback data dies in a spreadsheet. Here's how a B2B services or software team uses AI to turn tickets, NPS, and churn calls into owned actions.

30 days to pilot a governed feedback-analysis workflow

BRIEF · AI WORKFLOW AUTOMATION

Automating Variance Notes: Let AI Draft the "Why," Not Decide It

Variance commentary eats your controller's last day of close. Here's how to draft it with AI while keeping the explanation traceable, owned, and auditable.

4 finance controls before AI-generated notes

BRIEF · AI WORKFLOW AUTOMATION

The Tier-1 to Tier-2 Handoff Is Where Your Service Desk Bleeds Time. Fix That First.

The slow part of a service desk isn't the fix — it's the tier-1 to tier-2 handoff. How to use AI to build the escalation note, not close the ticket.

30 days to pilot a governed service-desk escalation workflow

BRIEF · AI MEASUREMENT AND ROI

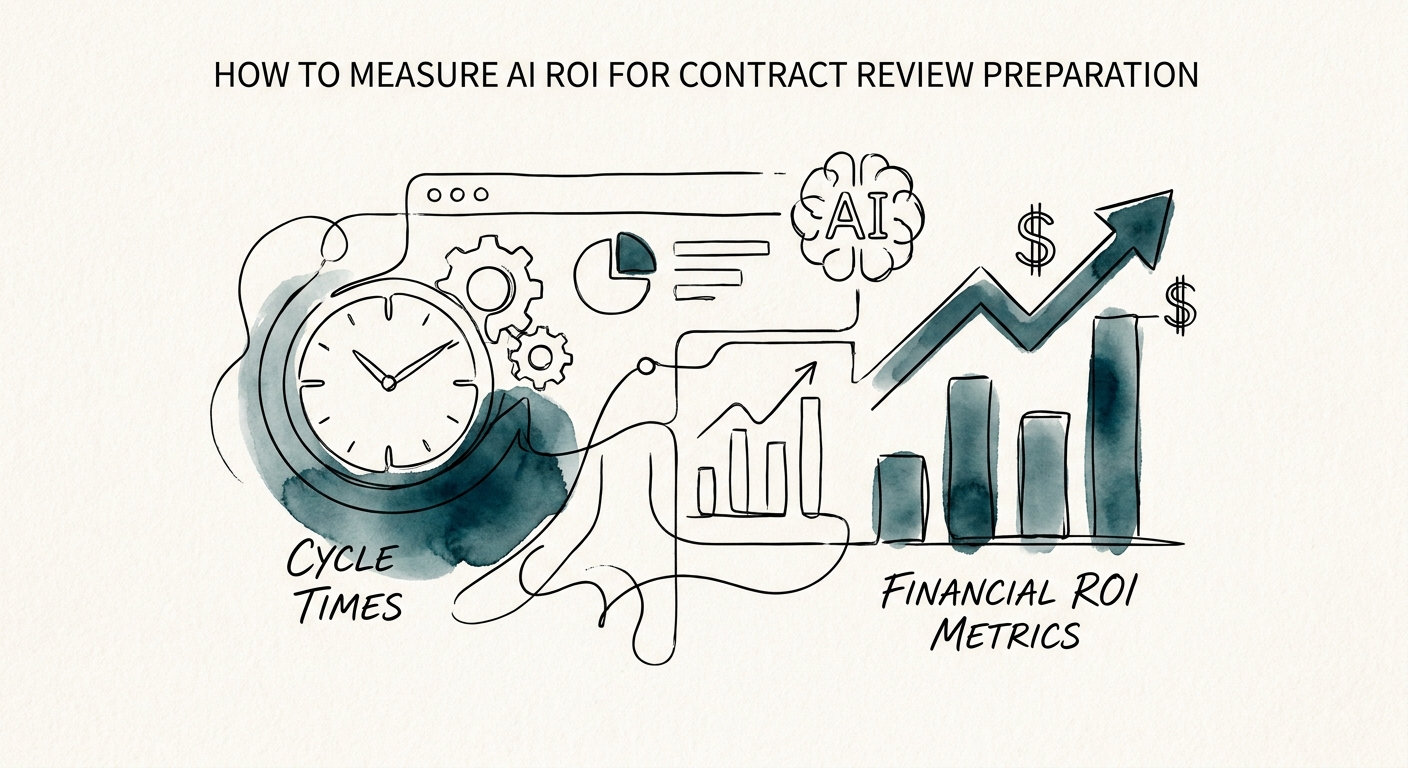

AI ROI for Contract Review Prep: Stop Counting Hours, Count Redline Loops

The real ROI of AI in contract review prep isn't faster reading—it's fewer redline loops and cleaner intake. Here's the scoreboard that proves it.

5 measures needed for contract review preparation ROI

BRIEF · AI MEASUREMENT AND ROI

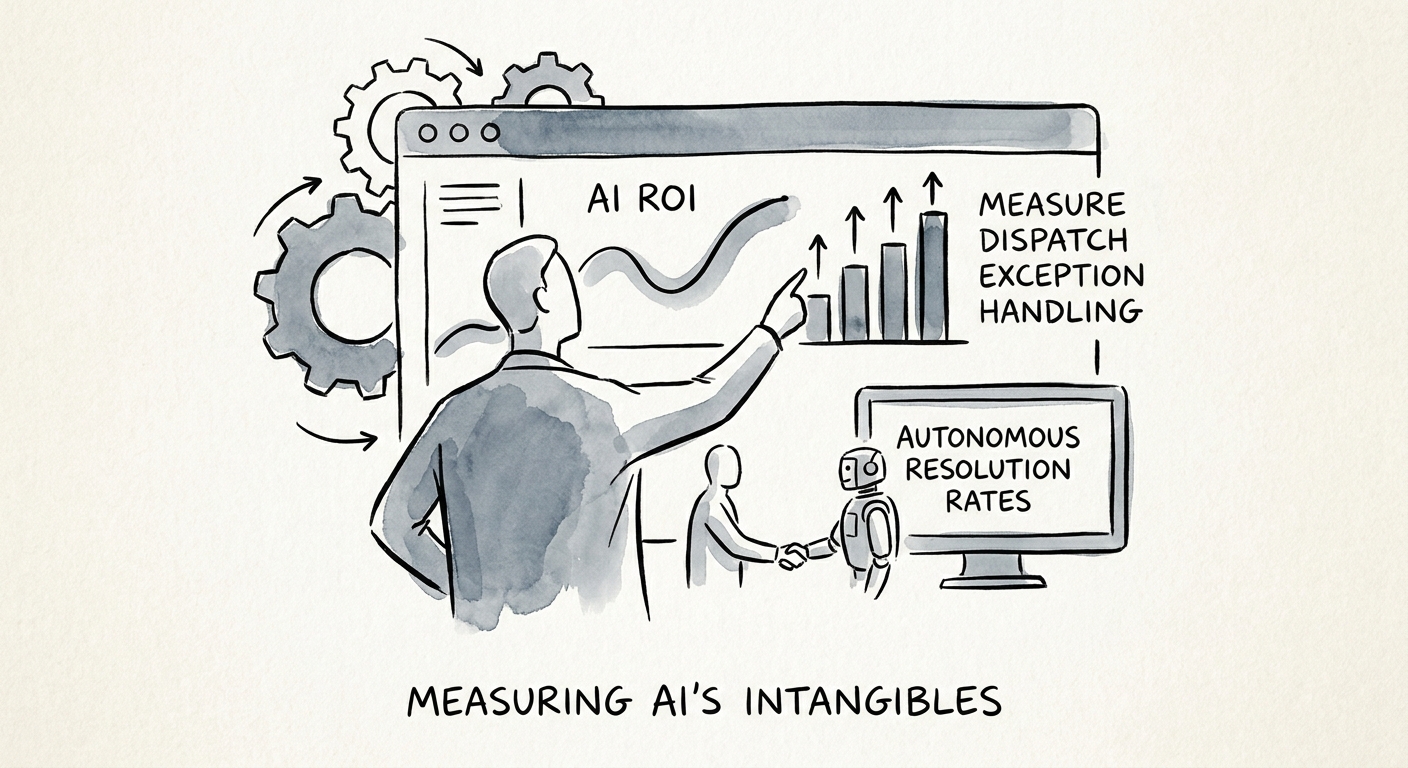

AI ROI for Dispatch Exception Handling: Count Truck Rolls, Not Summaries

A dispatch AI earns its keep when it catches the broken appointment window early enough to reroute. Here is how to baseline truck rolls, overrides, and missed windows.

5 measures needed for dispatch exception handling ROI

BRIEF · AI STRATEGY AND ROADMAP

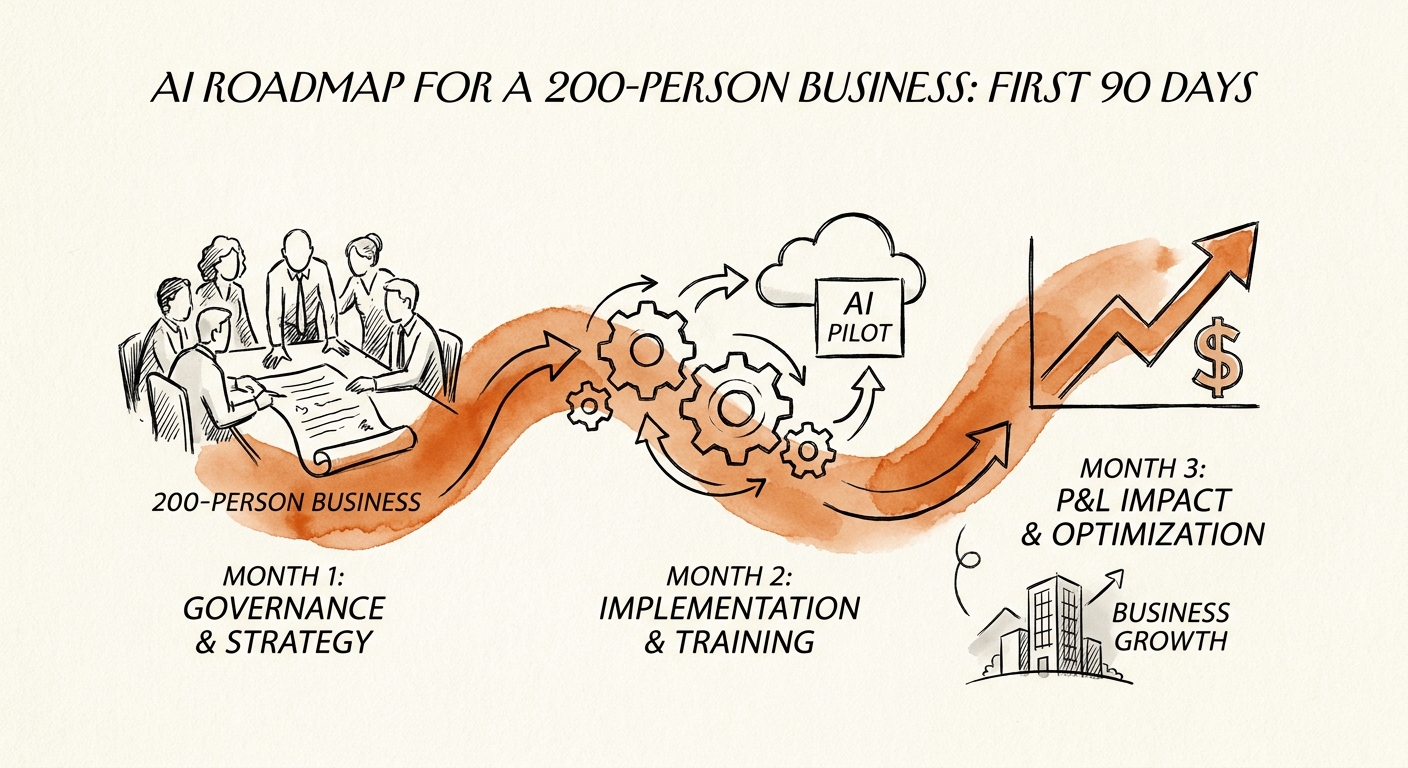

The 200-Person AI Roadmap: What to Actually Do in the First 90 Days

At 200 people you have real silos but no AI team. Here is a 90-day roadmap that ends with one governed workflow in production, not a tool wishlist.

90 days to move from AI ideas to one governed workflow

BRIEF · AI INDUSTRY USE CASES

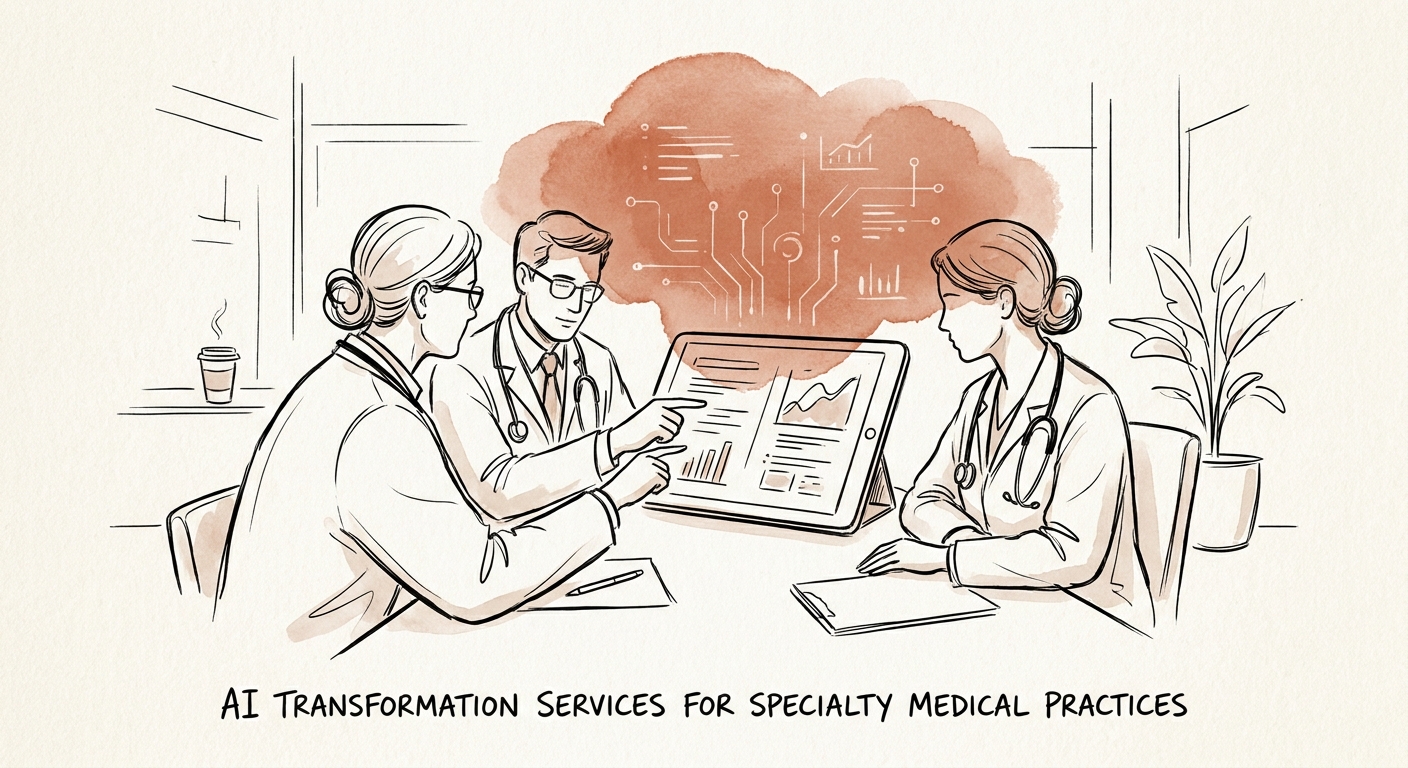

AI for Specialty Practices: Start Where the Paperwork Hurts, Not the Patient

Where a specialty practice should actually put AI first: prior-auth packets, referral intake, message drafts — with a reviewer on every output and PHI handled right.

90 days to validate a governed practice workflow

BRIEF · AI MEASUREMENT AND ROI

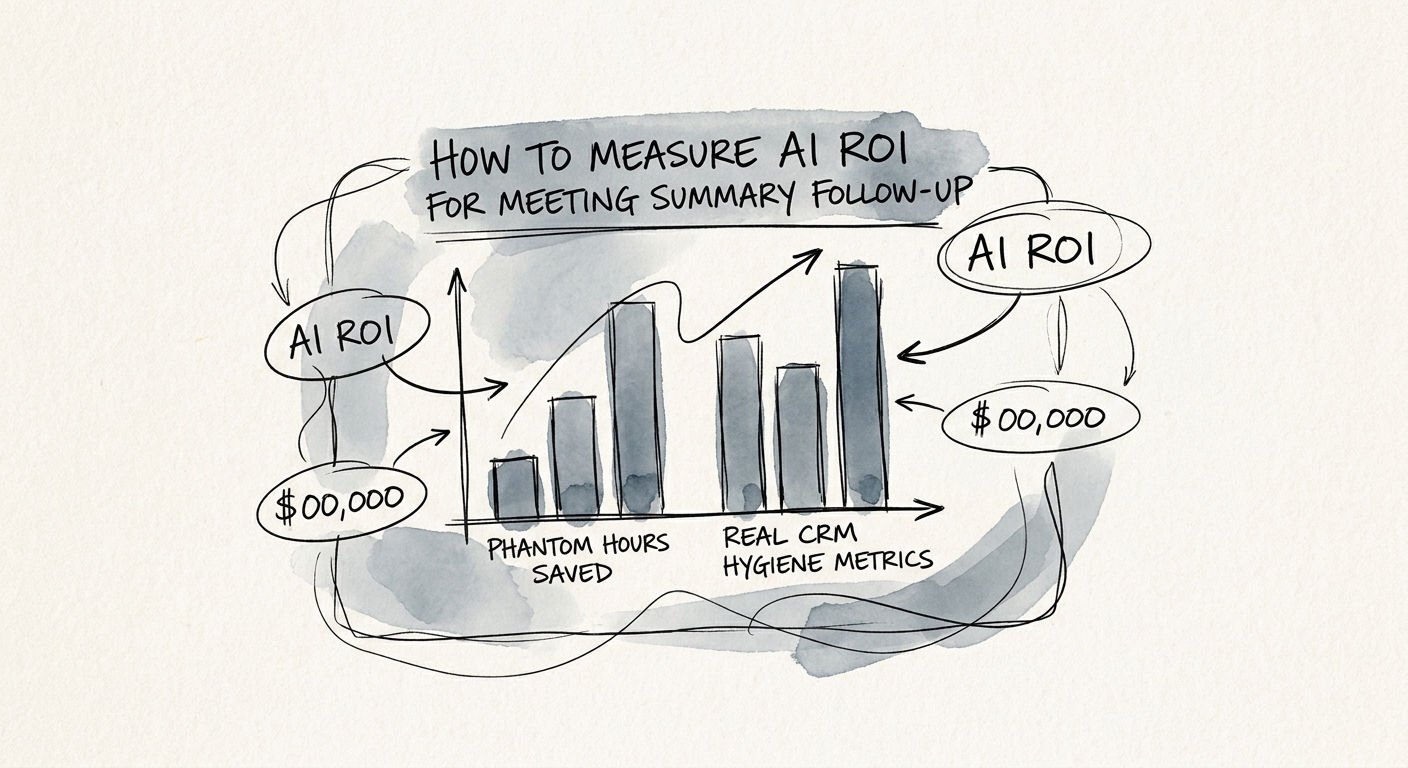

AI Took the Notes. Did Anyone Do the Work?

Your AI notetaker writes perfect recaps nobody acts on. Here's the follow-up scorecard a B2B services CFO can actually defend in a budget review.

Follow-up rate primary ROI measure for meeting-summary automation